18 May, 2026

European banks defend private credit links, pledge to limit exposure

By Deza Mones

| HSBC and Barclays both booked charges for a one-off private credit exposure, widely reported to be related to the now-collapsed Market Financial Solutions. Source: Peter Macdiarmid/Getty Images News via Getty Images Europe. |

Europe's biggest banks defended their exposure to the private credit market during their first-quarter 2026 earnings calls, with some outlining plans to review existing portfolios and curb their appetite for further financing in a bid to assuage growing investor jitters about risks tied to the near-$2 trillion industry.

Private credit — which involves directly originated loans that are not broadly syndicated and are typically provided by nonbank lenders — faces heightened regulatory scrutiny, given its complex lending structures, opaque valuations and concentration in specific sectors such as software, where valuations have come under pressure from AI advancements. Rising redemption requests, liquidity constraints and recent high-profile corporate blow-ups have added to the concerns.

Seven major European banks — Deutsche Bank AG, BNP Paribas SA, Barclays PLC, HSBC Holdings PLC, Société Générale SA, Banco Santander SA

British banks ensnared in Market Financial Solutions

HSBC and Barclays took losses related to a fraud case widely reported to be the collapse of nonbank mortgage lender Market Financial Solutions.

The HSBC charge came as a surprise as it did not lend directly to Market Financial Solutions but rather to intermediary credit providers. The bank's shares fell nearly 6% on May 5 after it reported a $400 million expected credit loss charge for what it said was a "fraud-related, secondary, securitization exposure with a financial sponsor in the UK."

Despite this, HSBC remains "comfortable overall" with its current private markets portfolio and views the fraud-related charge as "idiosyncratic and not representative of the portfolio," CFO Pam Kaur said during a May 5 earnings call.

"We reviewed all our highest risk exposures across our portfolio," Kaur said, adding that HSBC continues to assess its risk appetite and tighten due diligence.

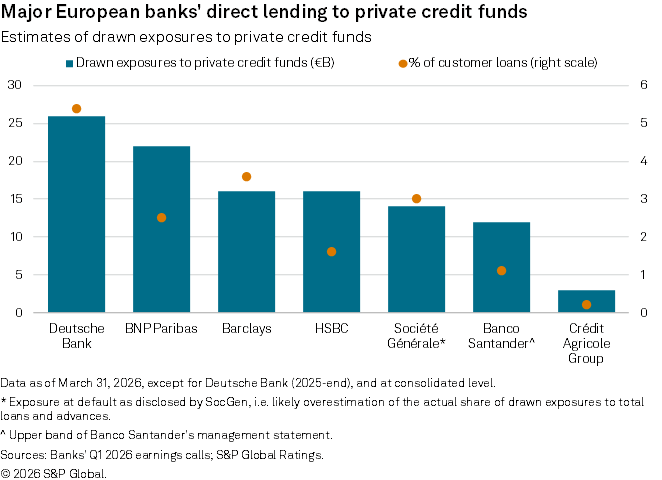

HSBC held $22 billion in private credit-related exposure at amortized cost, accounting for about 2% of its loan book. It includes €16 billion in drawn exposures corresponding to subscription and other securitization financings.

In June 2025, HSBC announced plans to inject $4 billion into its asset management unit's alternative credit funds, aiming to attract capital from other investors to create a $50 billion credit fund over the next five years. However, the bank is yet to deliver on that investment and has no current plans to do so, the Financial Times reported May 15.

Meanwhile, Barclays booked a £228 million charge in its securitized products business linked to a "well-publicized sophisticated fraud," prompting the bank to scale back lending to some structured finance counterparties, CEO CS Venkatakrishnan said. It is also cutting exposure to more highly leveraged, non-investment-grade corporates due to "increased macroeconomic and business uncertainties."

As of March-end, Barclays had £66 billion in structured financing exposure to nonbank financial institutions, of which £15 billion is to private credit, £1 billion to business development companies and £4 billion to private equity.

– Search across multiple earnings call transcripts using Document Intelligence.

– Use our ChatIQ AI tool to interrogate various S&P data sets.

– Set up alerts for European Data Dispatches.

Exposure downplayed

Deutsche Bank's previously disclosed private credit exposure of €25.9 billion as of 2025-end represents 5% of its overall loan portfolio, CFO Raja Akram said April 29. "Within private credit, performance is stable with no losses, and the portfolio is broadly unchanged."

Roughly 75% of the loan book is to multi-asset lender facilities collateralized by highly diversified midmarket corporate loans in the US and the EU, up from about 73% previously, Akram said. That included about €500 million of exposure to large business development companies — listed private credit vehicles that typically have retail investor participation.

France's BNP Paribas put its exposure at €22 billion, or about 3% of its loan book, of which 90% represents "senior portfolio financing" exposure. "We have no [nonperforming loans] on this segment, which is built through moderate loan-to-values, high diversification and exposure to the strongest private credit players," CFO Lars Machenil said.

French bank SocGen reported roughly €14 billion in total private credit exposures at default, representing about 1.4% of its group exposure, while peer Crédit Agricole's stood at around €2.9 billion, or 0.2% of its commercial lending.

Spain's Banco Santander has less than 1% of its total portfolio exposed to private credit, CEO Héctor Grisi said. "This is not a core business for us ... 70% of what we have outstanding there is subscription lines to the best names in the industry. So we don't foresee any problems at that," the executive told analysts. Ratings estimates Santander's exposure at up to €11 billion based on its customer loans as of March-end.

Other banks also described their private credit ties as marginal.

Italy-based Intesa Sanpaolo SpA has a "well-diversified loan portfolio with no material exposure to private credit," CFO Luca Bocca said, while domestic peer UniCredit SpA has "very limited" exposure, largely within the EU, according to CEO Andrea Orcel.

Dutch bank ING Groep NV's lending to private credit funds is "limited" to roughly €2 billion, or some 0.2% of its total exposure, and consisted mainly of collateralized fund financing for diversified portfolios, according to its earnings presentation.

Regulatory warnings, looming risks

The disclosures come as regulators ramp up their warnings about the potential risks posed by the private credit market to the wider financial system.

"Private credit at its current size and scope has not been tested during a severe economic downturn, which could expose leverage and borrower credit quality vulnerabilities," the Financial Stability Board (FSB), a global finance watchdog, said in a report published May 6. The FSB also raised concerns about the influx of retail investors into the market, noting that the share of assets under management accounted for by retail investors had risen "from virtually zero to around 13% in the past decade."

Top officials at the Bank for International Settlements, the European Central Bank and the Bank of England also sounded the alarm on private credit recently.

The FSB estimates euro area and UK banks' aggregate private credit exposures at $130 billion.

While European banks' direct exposures to the private credit market appear contained overall, Ratings said the banks' concentrated lending to the software sector "could lead to a gradual deterioration of private credit funds' credit portfolios, prompting banks to curtail further fund financing and potentially increase credit provisioning."

"We don't see these private credit fund exposures as a material source of systemic risk for European banks. However, following a period of rapid growth and amid a worsening macro environment, more nonbank lenders could report deteriorating credit portfolios," Ratings wrote in its report.

"As secured lenders, banks are not first to in line to absorb resulting losses; but neither are they immune," Ratings said.