21 May, 2026

European banks add more than €1.5B of loan loss provisions for Middle East war

Many of Europe's largest banks raised loan loss provisions for risks related to the war in the Middle East during the first quarter, citing uncertainty over the impact and duration of the conflict.

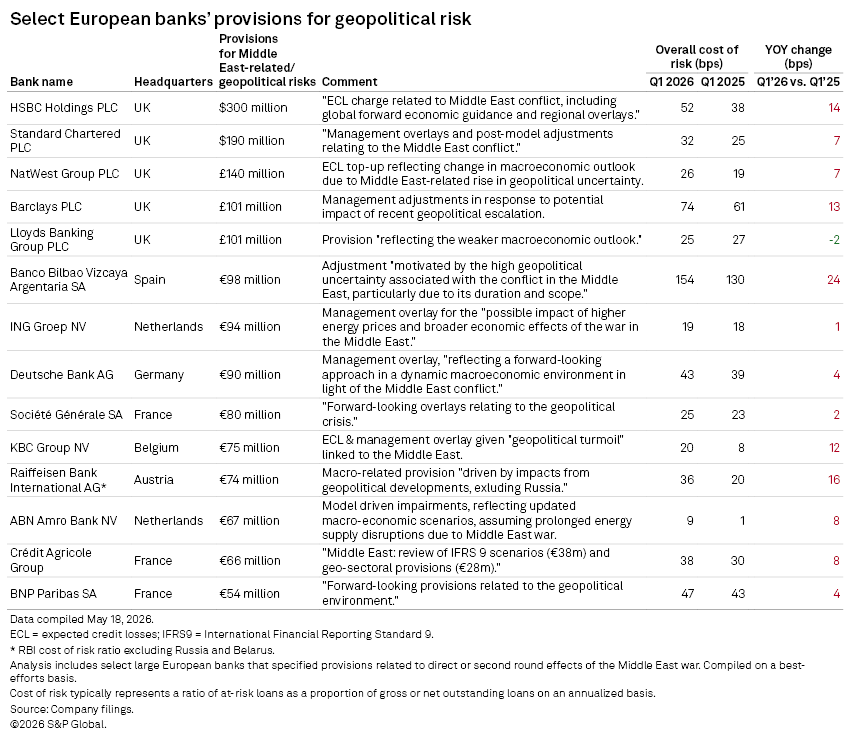

European lenders attributed more than €1.5 billion of fresh provisions to the war and geopolitical risk, an S&P Global Market Intelligence analysis of the latest round of bank earnings shows. UK banks set aside the largest sums, led by Asia-focused groups HSBC Holdings PLC and Standard Chartered PLC (StanChart).

While the direct impact of the war on European banks has been limited so far, lenders set aside additional reserves mainly due to updated macroeconomic scenarios and weightings, reflecting potential negative second round effects such as slower GDP growth and higher inflation.

Banks stressed that a longer duration of the war would have a more pronounced macroeconomic impact in Europe and globally. Many still expect resolution within the next couple of months, but the ongoing uncertainty prevented some from updating financial targets for the year.

HSBC's $300 million ECL charge was precautionary and meant to cover the negative effects of the war everywhere, not just the Middle East, CFO Pam Kaur said during a May 5 earnings call. The bank "has not experienced significant financial impacts from recent events in the Middle East to date, and we are well positioned to manage the current uncertainties," the group said in its earnings presentation.

StanChart executives made similar comments during an April 30 earnings call, with interim CFO Peter Burrill saying the $190 million in additional management overlays was precautionary for effects that have not been experienced yet. StanChart's overall annualized cost of risk in the quarter of 32 basis points was within the group's through-the-cycle guidance of 30-35 basis points, Burrill said.

So far, markets and trade have been "quite resilient," as has StanChart's credit quality, CEO Bill Winters said during the call. "We remain hopeful that this conflict will resolve before there's acute damage to the economy, but you can't preclude that possibility [and] our stress scenarios try to capture as much of that as possible," Winters said.

NatWest Group PLC's £140 million provision reflects changed macroeconomic assumptions in the wake of the Middle East war and not the group's credit performance, "which remains strong," CEO Paul Thwaite said during a May 1 earnings call. While sentiment amid the heightened geopolitical uncertainty is "more considered, we have yet to see any material impact on our customers," Thwaite said.

The changing economic landscape and shifts in interest rate expectations could have a positive impact on banks. With rates set to stay higher for longer, NatWest expects its revenue to be at the top end of its guidance of £17.2 billion to £17.6 billion in 2026, Thwaite said.

While Barclays PLC took out £101 million in Middle East-related provisions, these were largely offset by the £81 million release of tariff-related adjustments made in the first quarter of 2025.

"At this point, we don't see any significant impact from the situation in the Middle East, other than the revenue impacts, which have been broadly positive, to date," CFO Anna Cross said during Barclays' April 28 earnings call.

Both Barclays and HSBC booked private credit portfolio-related loan loss charges in the first quarter that exceeded Middle East-driven provisions, pushing up the overall cost of risk. The losses related to a fraud case, widely reported to be the collapse of nonbank mortgage lender Market Financial Solutions, amounting to £228 million at Barclays and $400 million at HSBC.

– Use Document Intelligence to interrogate multiple earnings call transcripts.

– Access Visible Alpha estimates for HSBC. (May require additional subscription.)

– Sign up for Earnings IQ alerts to get results as soon as they're released.

"Different story every day"

Some banks highlighted the difficulty of predicting the actual impact of the war, both on the economy and client sentiment, given the ongoing high uncertainty about its duration.

Spanish group Banco Bilbao Vizcaya Argentaria SA took out €98 million in Middle East-linked provisions in the first quarter, noting the continued lack of clarity on the war's "duration and scope."

"We are quite cautious in terms of the impact because we don't know. It's a different story every day," CEO Onur Genc said during an April 30 earnings call.

BBVA's provision was taken mainly for potential negative second round effects of the war on its operations in Türkiye and Spain, while the effects on business in Latin America would be "neutral or positive", Genc said.

Belgium's largest bank KBC Group NV and the Netherlands' third-largest lender ABN AMRO Bank NV, both cited the uncertainty over the duration of the Middle East war as the reason to keep their net interest income (NII) guidance unchanged, despite strong first-quarter results.

"It is extremely difficult to give any sensible comments" on the NII outlook as multiple scenarios are still possible, specifically around the path of interest rates, KBC CEO Johan Thijs said during a May 12 earnings call. The group's 2026 guidance for NII of at least €6.725 billion is "very conservative", but the bank will have "a better view" after the second quarter, Thijs said.

At present, KBC still expects the war to be "short-lived", lasting for two to four more months, Thijs said. The Belgian group took out €75 million in provisions for potential economic effects related to the Middle East war.

Expectations of higher eurozone rates could add €100 million to ABN Amro's NII in 2026, yet there are still variables that could change depending on the duration and outcome of the conflict, CEO Marguerite Bérard said. ABN Amro added €67 million in provisions, mainly related to changes in macroeconomic scenarios and scenario weightings over Middle East risks.

"Depending on the more or less lasting effects, you may have also different competitive and pricing behavior and also expectations from clients," Bérard said during a May 13 earnings call. If the conflict is not resolved by the end of June or early July, ABN Amro expects the negative impact of higher energy prices to intensify, dampening economic growth and driving up inflation, Bérard said.

In contrast, ING Groep NV raised its NII forecast for 2026 despite taking out a €94 million management overlay linked to the war. The Netherlands' largest bank has not seen a big impact from the Middle East war, with the first-quarter cost of risk "still quite benign," CEO Steven van Rijswijk said during an April 30 earnings call.

ING now expects NII of up to €16.7 billion in 2026, compared to the previously targeted up to €16.5 billion. This is based on expectations for expected higher-for-longer interest rates, hedging tailwinds from the group's deposit replicating portfolio and continued volume growth, CFO Ida Lerner said.