22 May, 2026

Aon and UnitedHealth matched peers in Q1 2026 despite Berkshire's exit

By Tyler Hammel

Shares in both Aon PLC and UnitedHealth Group Inc. matched or bettered those of their peers during the first quarter, even as Berkshire Hathaway Inc. dropped the two companies from its investment portfolio.

The insurance broker and managed care giant saw declines that largely matched trends within their broader sectors, as various issues complicated investor confidence in both insurance brokers and managed care insurers.

While both companies reported solid first-quarter earnings and maintained or raised full-year earnings estimates, Berkshire Hathaway sold off its remaining stakes during the quarter, but before first-quarter earnings were reported and full-year estimates adjusted.

The UnitedHealth stake had been comprised of about 5 million shares worth roughly $1.66 billion at 2025-end, representing approximately 0.6% of the company. Berkshire's holdings in Aon had totaled about $1.27 billion, representing approximately 1.7% of the company.

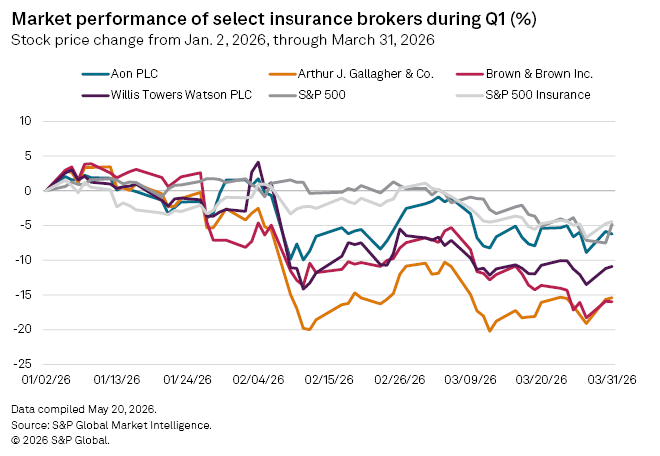

Despite its stock price declining 6.2% from Jan. 2 to March 31, Aon outperformed similar insurance brokers during the same period: Willis Towers Watson PLC fell 10.9%, Arthur J. Gallagher & Co. dropped 15.4%, and Brown & Brown Inc. was down 16%.

Even though Berkshire Hathaway exited Aon, various analysts remained positive on the broker's financials following the release of first-quarter earnings in May.

Piper Sandler analyst Paul Newsome rated the company as "overweight" in a May 4 research note, writing that Aon's revenue was better than expected and organic growth was "essentially in line with consensus but slightly lower than we expected."

"Aon is one of the largest global insurance brokers and targets mid-single-digit or greater organic revenue growth, continued adjusted operating margin expansion, 'strong' adjusted EPS growth, and double-digit free cash flow growth through 2026," Newsome wrote.

Aon's long-term track record of expense management and its solid, recruitment-bolstered organic growth prospects will drive outperformance over the next year, wrote Keefe Bruyette & Woods analysts in a similar post-earnings research note. The analysts also highlighted comments by CFO Edmund Reese during the call, indicating the company's continued investment in data centers.

"On Aon's call, Mr. Reese reported that Aon's data center revenue pipeline is on pace to be [3x higher year over year]; we think a relatively small group of brokers — obviously including Aon — will share in the revenue growth, including near-term data center construction and long-term data center operations," the analysts wrote.

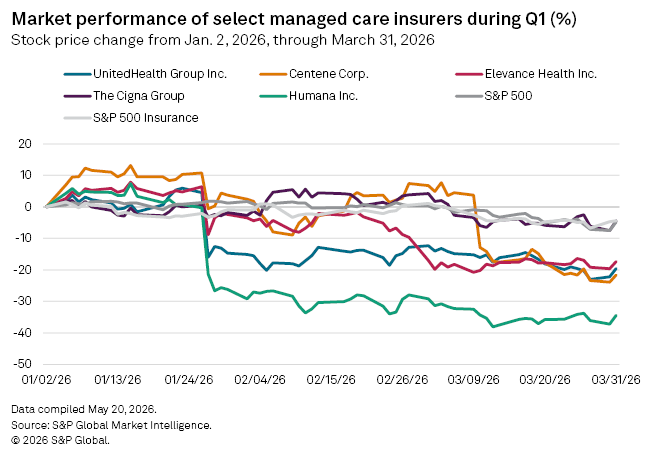

UnitedHealth had a similar experience in the first quarter, with its stock dropping 19.6%.

In earnings results, UnitedHealth similarly met or exceeded first-quarter analyst expectations, raising its full-year earnings to $18.25 from $17.75. The company attributed some of its first-quarter improvements to higher-than-anticipated Medicare Advantage rates for 2027, which are expected to help offset rising costs in the senior-aimed, government-subsidized health plans.

The managed care insurer received an "overweight" rating from J.P. Morgan analyst Lisa Gill in a research note following the company's April first-quarter earnings call. The tone of the call was positive, with all segments outperforming, and the company is on track for a turnaround, Gill wrote.

"Between this and the improvement to the final 2027 [Medicare Advantage] rate notice, we think that sentiment may be shifting to a more constructive position, although we expect [second-quarter] earnings commentary on trend will be a key catalyst for further investor positivity," Gill wrote.

Neither company responded to a request for comment before publication.