22 May, 2026

Analysts see NextEra-Dominion deal closing, but may not augur more utility M&A

By Allison Good

What is the outlook for the NextEra-Dominion deal and its impact on utility M&A?

Analysts are largely optimistic that NextEra Energy Inc.'s proposed acquisition of Dominion Energy Inc. will close, citing the deal's structure and strategic drivers. However, they are divided on whether this transaction will trigger a broader wave of utility industry consolidation. Some view it as a unique "one-off" driven by NextEra's specific need to rebalance its earnings profile, while others see it as a validation of scale in a new load-growth cycle.

Why is this deal significant for the US energy sector now?

The proposed merger comes as NextEra seeks to dilute its reliance on expiring clean energy tax credits by increasing its regulated business mix. For Dominion, the deal follows a period of investor disappointment and a strategic business review. The transaction's timing also coincides with a broader industry discussion about the need for scale to capitalize on new load growth from artificial intelligence (AI) and electrification, making this a pivotal moment to assess the future of utility consolidation.

Key Insights

- NextEra's acquisition of Dominion is driven by a strategic need to increase its regulated business from 70% to over 80%, reducing overall business risk and diluting its reliance on expiring clean energy tax credits.

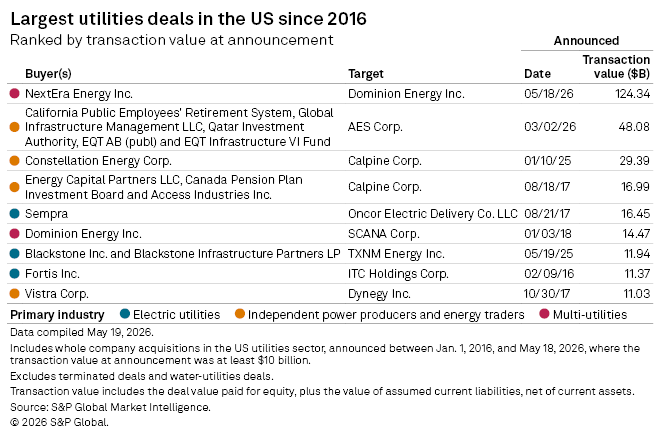

- Analysts express confidence in the deal's closure, pointing to significant termination fees: $2.24 billion payable by Dominion and up to $6.52 billion payable by NextEra under various circumstances.

- The combined company would become the third-largest in the US energy sector by market capitalization, trailing only Exxon Mobil Corp. and Chevron Corp.

- Opinion is split on whether this deal will spur more utility mergers and acquisitions (M&A). Some analysts see it as a "one-off," while others believe it validates the need for scale and could make M&A more common for utilities seeking higher growth rates.

- NextEra has a history of walking away from deals that face regulatory roadblocks, a context that analysts say is important should the Virginia State Corporation Commission initially deny the transaction.

Industry analysts are largely optimistic that NextEra Energy Inc.'s proposed $70 billion acquisition of Dominion Energy Inc. will close, but disagree over whether the deal may usher in a new round of broader utility industry consolidation.

With Dominion, NextEra faces a greater sense of urgency than in previous attempted mergers, Jefferies Equity Analyst Julien Dumoulin-Smith said in an interview with Platts, part of S&P Global Energy.

"This transaction has everything to do with NextEra wanting to rebalance itself, and recognizing there's an abundance of tax credits in their earnings profile that need to be diluted down because those aren't sustainable," he added, referencing clean energy incentives set to expire in the next few years.

"In earlier years they thought they had time, which is why they went after smaller utilities in some respects," Dumoulin-Smith said.

Upon the merger's close, NextEra's regulated segment would increase from 70% of its business mix to over 80%, reducing overall business risk, S&P Global Ratings wrote in a May 18 report.

NextEra has unsuccessfully pursued several US electric utilities over the past decade. It agreed to buy Hawaiian Electric Industries Inc. for $4.3 billion in December 2014, but terminated the deal in July 2016 after the Hawaii Public Utilities Commission rejected it. Days later, NextEra announced an agreement to buy Oncor Electric Delivery Co. LLC for $18.7 billion, which fell apart in July 2017 after the Public Utility Commission of Texas rejected the merger and declined a rehearing request. Oncor was soon after acquired by Sempra.

In both rejected deals, state regulatory bodies cited negative impacts to ratepayers in their decisions.

In 2020, NextEra made unsolicited takeover offers to Evergy Inc. and Duke Energy Corp. that both companies rebuffed.

The Dominion deal also includes $2.25 billion in bill credits spread out over a two-year period for Dominion's customers.

"It's a meaningful starting point," Nicholas Campanella, senior equity research analyst at Barclays, said in an interview, adding, "There's high confidence in the management teams of getting this done based on the break fees."

If Dominion terminates the deal following a change of board recommendation, a decision to enter into an alternative transaction or failure to receive shareholder approval, the company will be required to pay NextEra a $2.24 billion termination fee. Likewise, NextEra will be required to pay Dominion a termination fee of $6.52 billion under similar circumstances. If the merger is terminated as a result of failure to receive regulatory approval, NextEra must pay Dominion a $4.83 billion termination fee.

In previous proposed deals, however, NextEra has been the party to walk away.

"The company's merger history is somewhat akin to a runaway bride," Washington Analysis Director of Policy Research Rob Rains wrote in a May 18 report. "It historically does not revise its bids nor does it negotiate against itself."

"Twice the utility has declined to take a second bite at the apple when it has encountered roadblocks, and the merger should be considered within this historical context should the [Virginia State Corporation Commission] initially deny the transaction," Rains added.

The combined company would be the third-largest in the US energy sector by market cap, behind Exxon Mobil Corp. and Chevron Corp.

Dominion, meanwhile, has faced investor disappointment, with lackluster share prices and a focus on ESG after selling its midstream natural gas pipeline business in 2020.

The company initiated a top-to-bottom business review in November 2022, resulting in the sale of three gas distribution utilities, its Cove Point LNG export facility and a stake in its Coastal Virginia Offshore Wind project due to come fully online in the first half of 2027.

"They were on the mend, so in some respects [the merger announcement] was surprising," Jefferies' Dumoulin-Smith said.

Consolidation doubts

Analysts at Mizuho and Evercore told clients they expect more utility-sector M&A activity.

"We believe the transaction could redefine the regulated utility opportunity set, thus validating the notion that scale for both buying and building is a structural competitive advantage in the AI/load-growth cycle," Evercore said.

In August 2025, Black Hills Corp. and NorthWestern Energy Group Inc. announced a $3.6 billion all-stock merger to fulfill what they said had become an immediate need for scale and growth, while AES Corp. agreed to a $10.7 billion take-private transaction earlier this year in part to "maintain a leading position with big tech customers."

Mizuho analyst Anthony Crowdell described in a May 19 report an emerging distinction in the sector between utilities with projected compound annual growth rates (CAGRs) of 8% or greater and those with lower forecasts, writing, "We believe M&A may be more commonplace to push up EPS CAGRs."

Barclays' Campanella agreed that conversations are likely "happening elsewhere about other potential tie-ups," even though utility companies do not necessarily need to consolidate to capitalize on load growth.

"What we hear from executives is that size and scale matter, but utility management teams have a lot of one-time organic rate base growth opportunities in front of them," he said.

Morningstar's Andrew Bischof is also "more cautious" about further transactions, given NextEra's uniquely large balance sheet and Dominion's discounted trading multiples.

"I'm not quite sure I see that dynamic elsewhere in the market right now," he said in an interview.

For Dumoulin-Smith, the transaction is "really a one-off."

"I don't think you're going to have a lot of tolerance for more transactions in a world in which affordability is so front and center and when … utilities are actively walking away from rate cases," Dumoulin-Smith said.

Still, a merger between utilities with overlapping service territories could ultimately benefit ratepayers by reducing operations and maintenance spending and redeploying it as capex "while keeping bills flat," according to Barclays' Campanella.

How S&P Capital IQ Pro Supports Utility M&A Analysis

Navigating the complexities of utility M&A, as highlighted by the NextEra-Dominion deal, requires comprehensive data and analytics. S&P Capital IQ Pro provides essential tools for stakeholders to evaluate such transactions.

- Financial and Market Analysis: Users can access in-depth financial data, including historical share price performance and trading multiples, to understand the valuation dynamics that made Dominion an attractive target. This allows for peer analysis and benchmarking against sector trends.

- Deal Structure and Terms: The platform offers detailed information on M&A transactions, including deal values and specific terms like the termination fees that analysts cite as indicators of commitment in the NextEra-Dominion agreement.

- Regulatory Monitoring: With regulatory approval being a critical hurdle, our tools help track proceedings and decisions from bodies like the Virginia State Corporation Commission, providing context from past cases such as NextEra's pursuits of Oncor and Hawaiian Electric.

- Company Profile and Strategy: Clients can analyze company strategies, such as Dominion's top-to-bottom business review and NextEra's efforts to rebalance its business mix, to understand the fundamental drivers behind major corporate actions.

Frequently Asked Questions About the NextEra-Dominion Merger

Q: Why is NextEra motivated to acquire Dominion? A: According to the analysis, NextEra wants to "rebalance itself" by increasing its regulated business mix from 70% to over 80%. This strategy is aimed at diluting its reliance on expiring clean energy tax credits and reducing its overall business risk profile.

Q: What are the main arguments against this deal sparking more utility M&A? A: Some analysts view this as a "one-off" transaction due to NextEra's uniquely large balance sheet and Dominion's discounted trading multiples, a dynamic not seen elsewhere. They also note that affordability is a major concern for regulators, and many utilities are focused on their own organic rate base growth opportunities rather than consolidation.

Q: What indicates that this deal is likely to close? A: Analysts point to the significant termination fees as a sign of high confidence from the management teams. If the deal is terminated under certain conditions, Dominion would owe NextEra a $2.24 billion fee, while NextEra could owe Dominion a fee as high as $6.52 billion.

Q: What is NextEra's track record with large utility mergers? A: NextEra has a history of unsuccessfully pursuing utilities, including Hawaiian Electric Industries Inc., Oncor Electric Delivery Co. LLC, Evergy Inc., and Duke Energy Corp. The analysis notes the company has been described as a "runaway bride" that historically does not revise its bids and has walked away from deals facing regulatory roadblocks.

Location

Products & Offerings