08 Apr, 2026

US equities largely resilient against Iran war impacts as ceasefire sparks rally

By Brian Scheid

US equities are proving largely resilient against the effects of economic uncertainty and geopolitical instability surrounding the war in the Middle East.

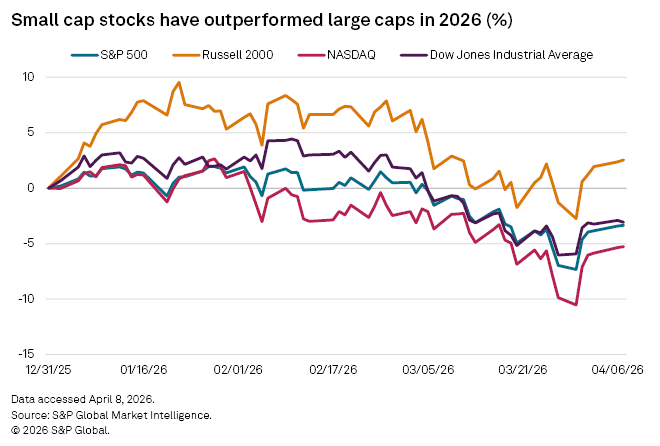

Stocks rallied on April 8 in the wake of a two-week ceasefire between Iran and US following a relatively modest slip since the war began. From the end of 2025 to April 7, 2026, the S&P 500 was down just over 3.3%, while the small-cap Russell 2000 was up more than 2.5%.

The S&P 500 fell more than 7.8% in the month that followed the start of war at the end of February, but was down less than 3.9% on April 7, just before Trump announced a two-week ceasefire on the condition that Iran reopen the Strait of Hormuz. The large-cap index was up more than 2.5% in early trading April 8 and was up more than 36% from a year ago.

"Investors rightfully believe that President Trump fears a stock market decline more than he fears Iran," said Michael O'Rourke, chief market strategist at JonesTrading. "Therefore, the expectation is that President Trump will seek an outcome that minimizes damage to the stock market."

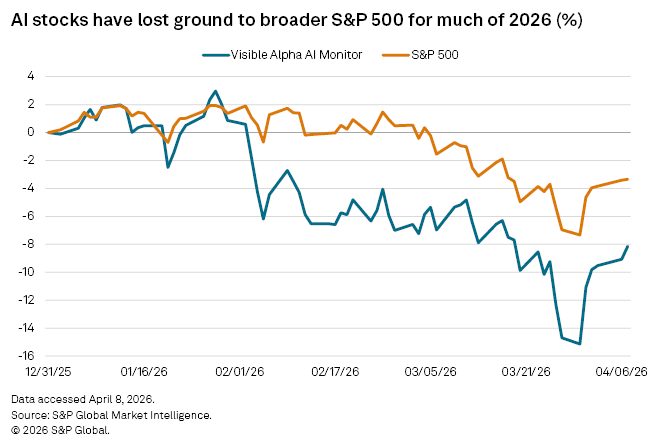

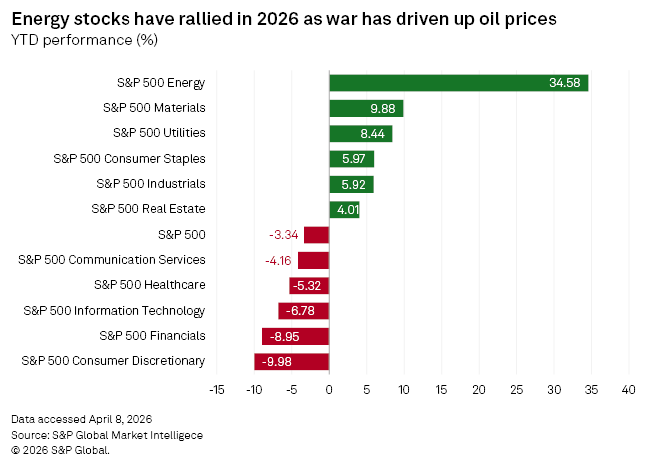

Even amid volatility through the first quarter of 2026, market strategists said that stocks have shown considerable strength as the war escalated and oil prices surged. Stocks also declined little even as AI stocks declined as concerns of a bubble grew, rising inflation expectations largely erased hopes of interest rate cuts this year, and financial stocks stumbled amid private credit fears.

"Despite geopolitical worries and soaring energy prices, the S&P 500 has been relatively resilient, even after falling for five straight weeks," said Bret Kenwell, an investment and options analyst at eToro. "Part of that likely reflects the view that any conflict in the Middle East will not be prolonged. At the same time, earnings estimates have continued to move higher this year, giving some investors reason to stay focused on the fundamentals rather than the headlines."

The ceasefire is unlikely the end of the war and market confidence will wane the longer the conflict goes on, but the market's foundation remains strong, as does the larger economy, said Paul Schatz, president of Heritage Capital.

"When geopolitical events hit, strong markets go back to the highs when the event ends," Schatz said. "Weak markets roll over and bounce and roll over again and again. The data still remain solid."

The relative resilience in equities since the start of the war may have been initially surprising, but the ceasefire recovery signals that any sell-off may have been a temporary repricing on geopolitical risk rather than deterioration in earnings or growth, said Daniela Hathorn, a senior market analyst with Capital.com.

"The S&P 500 isn't just a macro barometer as it's heavily weighted toward large-cap US companies with strong balance sheets, pricing power and global diversification," Hathorn said. "That gives it a degree of insulation from external shocks."

The domestic economy has remained "relatively solid" this year, despite some weakness in the labor market, and earnings expectations have not been meaningfully revised lower, Hathorn said.

"Equity markets tend to react more to changes in earnings than to headlines, and so far, analysts are still assuming that the impact of higher energy prices and geopolitical disruption will be manageable," Hathorn said. "With the ceasefire deal in place for now, the risk of prolonged impact on growth has reduced at the margins. However, there is no guarantee of a lasting resolution, so things could still get worse from here."

A lasting spike in oil prices, a steeper move up in inflation expectations, further delays in interest rate cuts, significant downgrades in earnings guidance, or a breakdown in credit market could also trigger a deeper decline in stocks as economic uncertainty shifts to tangible damage, Hathorn said.

Even major geopolitical shocks can have little impact on equities performance, but the war with Iran is unique due to the uncertainty that surrounds it, said Jeffrey O'Connor, US head of equity market structure at Liquidnet.

The messaging, goals, and timing of this war have been increasingly uncertain, and a Trump comment can generate tremendous market variance in short order, O'Connor said. Investors may be expecting a "violent snapback rally," on White House policy shifts, similar to the rally that followed Trump's easing of his tariff regime in 2025.

"The rebound trade burned a lot of institutional investors in 2025," O'Connor said. "Now in 2026; burn me once, shame on you, burn me twice, shame on me."