07 Apr, 2026

UK bank profits set to rise on stronger revenue, efficiency gains

By Vanya Damyanova and Uneeb Asim

| The UK's largest banks say they are well-positioned to weather any impact from the war in the Middle East and meet their key targets. |

Profits at the largest UK banks are forecast to increase in the coming years on the back of higher revenue and improving efficiency.

The near-term performance outlook remains positive despite heightened geopolitical risks amid the Middle East war. Analysts say lenders entered the new period of uncertainty in a strong financial position, while the banks themselves have expressed confidence in their ability to navigate the volatile environment.

Return on average equity (ROAE) at the country's four largest lenders by total assets — HSBC Holdings PLC, Barclays PLC, Lloyds Banking Group PLC, NatWest Group PLC — is projected to rise as efficiency ratios tick down in 2026 and 2027, according to consensus estimates compiled by Visible Alpha. Cost of risk, which measures loan loss provisions as a share of gross loans, is expected to remain low, at under 0.6% for all banks, the data shows.

After a bumper 2025 where net interest income (NII) was a key driver for revenue and profits, UK banks are expected to sustain their strong performance, according to S&P Global Ratings analysts. "Refreshed guidance suggests a stronger 2026. Interest income is set to expand, cost discipline remains high, and credit costs [are] under control. Sector profitability should consequently climb," the analysts said in a March 9 commentary.

Revenue at all four banks is expected to increase in 2026 and 2027, with domestic-focused Lloyds and NatWest projected to see the strongest growth, according to Visible Alpha estimates data. NII, which is the difference between the interest banks earn on loans and pay on deposits, should also rise across all lenders, the data shows.

UK banks' revenue is heavily supported by structural hedges — trades that aim to even out the impact of interest rate changes on NII. As a result, UK banks have managed to grow NII even as interest rates have declined.

Assessing the Middle East war

The Middle East war has raised questions about bank performance as inflation and recession fears resurface amid a surge in oil prices and trade disruptions, but UK bank executives remain positive on the short-term performance outlook.

"We don't see [the impact of the conflict] materially slowing us down...We remain very confident in our 2026 guidance and our trajectory looking forward," Lloyds CEO Charlie Nunn said March 17 at the Morgan Stanley European Financials conference.

While the likely prolonged disruption at the Strait of Hormuz could raise inflationary pressure and slow UK economic growth, households and businesses in the country are more financially resilient now than at any time since the global financial crisis, Nunn said. Households have high levels of savings and businesses have robust cash flows, according to Nunn.

– Access Visible Alpha estimates data for Lloyds, NatWest, HSBC and Barclays.

– View aggregate UK banking industry data.

– Set up alerts for more EMEA Data Dispatches.

HSBC, which has the highest exposure to the Middle East among the four banks, expects to increase loan loss provisions in the short term but is still keeping its overall expected credit loss guidance for 2026, CFO Pam Kaur said March 18 at the same conference. HSBC remains committed to the region and believes in the potential of its business there, Kaur said.

Banks are well equipped to withstand and manage volatility, having set up risk barriers such as their structural hedges and built up resilient financial models designed to endure "the most robust of shocks" over the past decade, said Lindsey Naylor, head of the UK financial services practice at Bain & Co.

Bain & Co. expects a low single-digit percentage-point increase in UK-oriented banks' return on equity in 2026, "with potential upside depending on what happens in markets businesses, which are always a bit volatile in times of uncertainty," Naylor said in an interview.

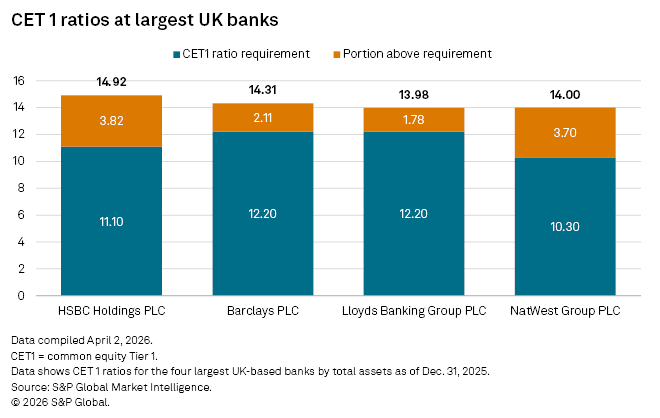

Banks have also built and maintained capital reserves in excess of regulatory minimums, with core capital ratios at the big four lenders near or above 14% in 2025, S&P Global Market Intelligence data shows.

In late 2025, the Bank of England lowered what it deemed the appropriate benchmark capital requirements for UK banks to reflect the reduced risks in the sector. While major UK banks' core capital ratios are anticipated to taper, this is not expected to be detrimental to ratings over the next 12 to 24 months, the S&P Global Ratings analysts said.

A drawn-out Middle East war has both positive and negative implications for banks' performance. Higher rates are generally good for revenue, but not when economic conditions worsen, said John Cronin, founder of financial sector research firm SeaPoint Insights.

Weaker economic growth expectations, higher inflation and the ensuing higher interest rates typically result in softer loan demand and tighter underwriting conditions, Cronin said. Other potential impacts include expected credit loss provisioning, adverse risk-weighted asset migration and markdowns in the valuations of investment portfolios and pension assets, he said.

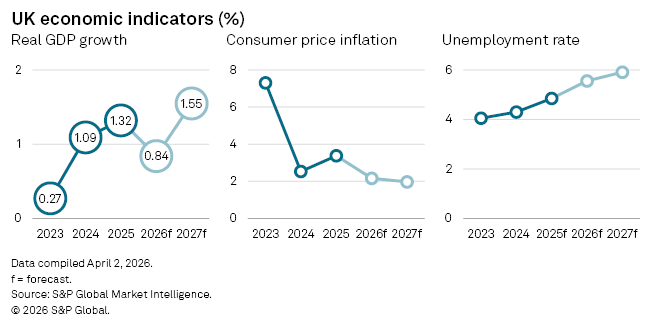

Current economic forecasts point to slower GDP growth and higher unemployment in 2026, yet inflation is still projected to ease this year, according to Market Intelligence data.

Net loan and deposit volumes at the big four banks are projected to increase across the board in 2026 and 2027, Visible Alpha data shows.

Loan volume growth has been more dynamic in recent years, and there are signs of acceleration in areas such as student loans and mortgages, which should support banks' interest income and margins, said Marco Troiano, head of financial institutions ratings at Scope Ratings. Banks' asset quality is something to watch closely as there is some deterioration expected here in 2026 and 2027, Troiano said.

The recent wave of acquisitions could also impact UK bank performance in the next couple of years and beyond, according to Naylor. Most major UK banks have announced a large transaction in the last two years and good execution of those deals, in terms of delivery on short-term synergies and longer-term objectives, will be crucial to medium-term economics, Naylor said.

Visible Alpha is a part of S&P Global Market Intelligence.