27 Apr, 2026

Bawag's €1.62B deal for PTSB undervalues Irish bank – analysts

By Bea Laforga and Beenish Bashir

| Permanent TSB, Ireland's third largest lender, was bailed out by the government during the global financial crisis. Source: NurPhoto via Getty Images Europe. |

The all-cash bid, which works out to a consideration of €2.97 per share of Permanent TSB (PTSB), already has the support of PTSB's board and its majority shareholder, the Irish government. While the price represents a 26% premium to PTSB's undisturbed share price when the formal sale process commenced Oct. 30, 2025, it is lower than the around €3.20 per share, or €1.75 billion, that Deutsche Bank analyst Marlene Eibensteiner had anticipated.

"The price looks favorable for Bawag, in our view. Bawag would be able to finance this transaction with existing resources by year-end 2026," Eibensteiner said in a note published April 14. Bawag expects the transaction to generate a more than 20% EPS accretion in three years, a target Eibensteiner deems achievable.

UBS analysts estimate that the deal would result in €756 million of negative goodwill for Bawag. Negative goodwill means the price paid is below the target company's fair market value and is recorded as a one-time gain for the buyer.

For John Cronin, founder of independent research firm SeaPoint Insights, the price is "disappointing" as PTSB is on a "speedy returns recovery journey," has substantial excess capital and is operating in a highly favorable economy. PTSB's valuation could range from around €2.3 billion to as much as €3.2 billion based on various estimates, Cronin wrote in an April 17 note.

One potential obstacle to achieving PTSB's "fair value" in the offer was a lack of competition among bidders in the banking sector, with the two other contenders being private equity firms, Cronin said.

Private equity firms Centerbridge Partners LP and Lone Star Global Acquisitions Ltd. were among the remaining contenders for PTSB, alongside Bawag.

Despite a lower-than-expected price, Bawag is the "preferable" owner of PTSB from a longer-term perspective on financial system stability, rather than a private equity company that might sell the bank again in the future, Cronin noted.

Bawag intends to self-fund the deal through existing excess capital, withholding its dividend for the first half of 2026, capping payouts for the full year, and taking measures to reduce risk-weighted assets such as significant risk transfers (SRTs).

International expansion

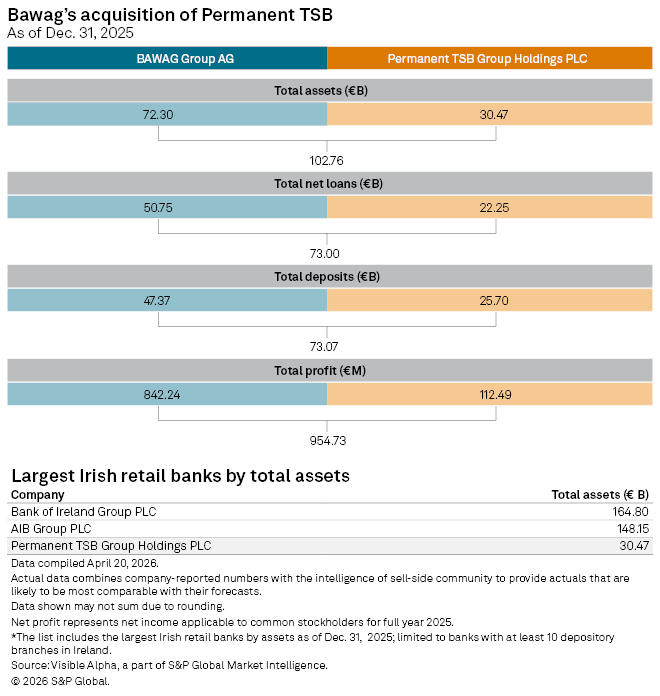

The transaction, set to take effect in the fourth quarter of 2026 or the first quarter of 2027, would increase Bawag's assets by about 40% to €102.76 billion and boost net profit to around €950 million, according to S&P Global Market Intelligence data. PTSB is already the third largest bank in Ireland, while Bawag has been present in the country since 2015 and operates a mortgage and deposit franchise through MoCo.

"We believe consolidation among European banks is a catalyst for creating stronger institutions better equipped to compete both domestically and internationally," CEO Anas Abuzaakouk said in a call following the offer announcement. "PTSB will be transformative in advancing our vision."

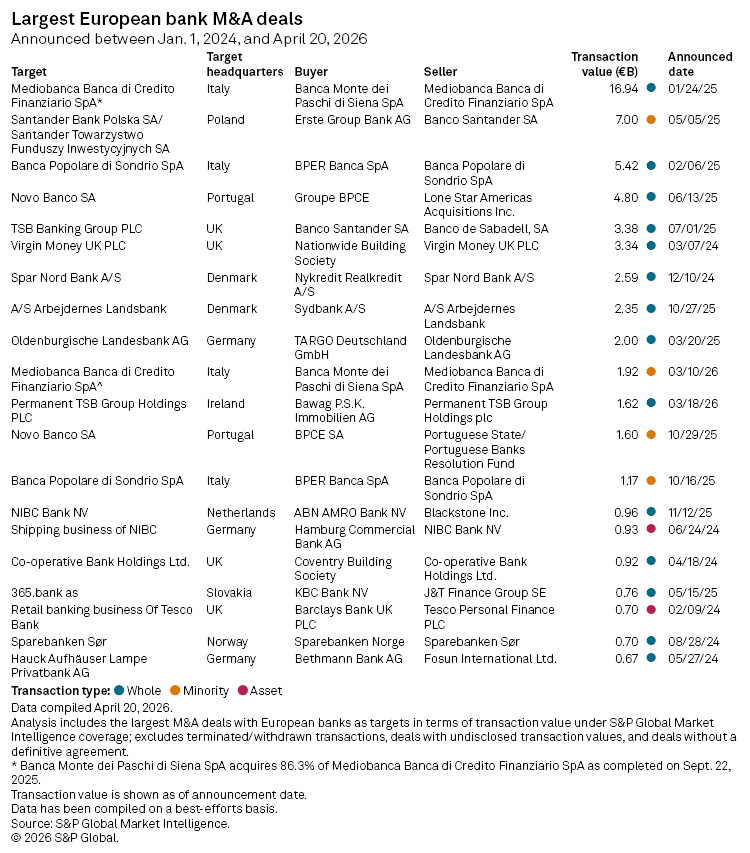

The deal would be the 11th largest among European banks since 2024, according to Market Intelligence data.

Cost challenge

The Irish government will be paid around €931 million for its remaining stake in PTSB, marking its exit 17 years after rescuing the bank in 2011. Including Bawag's offer, the state will have recovered the roughly €4 billion it invested in PTSB through fees, dividend income, bank levies and proceeds from its earlier stake sales.

"The state has and continues to be very supportive of PTSB, and the government believes that it is in the long-term interests of PTSB and citizens in general that the bank be returned to full private ownership and begin the next phase of growth," Tánaiste and Irish Finance Minister Simon Harris said in a statement.

PTSB has grown profitable since the bailout. Its net profit reached €112.5 million in 2025 and is projected to rise to €159.3 million by 2027, Visible Alpha data shows. Asset quality has also improved with the bank's stock of bad loans declining in 2025, although this is estimated to increase slightly in the next two years.

Still, PTSB has fallen behind European peers in improving cost efficiency, making aggressive cost rationalization a key part of Bawag's integration plan, UBS analysts noted. PTSB's cost-to-income ratio was 79.2% in 2025, compared to 37.8% for Bawag. A higher ratio indicates a less efficient business.

"PTSB fits Bawag's M&A blueprint well in terms of clear opportunities for cost optimization, profitability improvement and potentially capital extraction over time," UBS analysts added.

Visible Alpha is a part of S&P Global Market Intelligence.