24 Mar, 2026

Software debt sell-off signals cyclical turn for private equity and credit

By Iuri Struta

| A sell-off in software stocks preceded a decline in software loan bid prices. Source: Torsten Asmus / iStock / Getty Images Plus via Getty Images |

Private equity and private credit helped fuel the post-pandemic software boom, leaving some of these buyers and lenders facing losses amid a cyclical downturn in the sector.

Buttressed by cheap credit from private lenders and syndicated loans, private equity firms embarked on a software company buying spree in 2021 and 2022, paying ever-higher valuations as digital transformation efforts drove software growth rates above 20%. In subsequent years, rising interest rates and declining software growth rates compressed valuations, exposing investors in private credit funds and private equity firms to potential losses.

With the Federal Reserve thus far holding interest rates steady, the outlook for multiple rate cuts in 2026 is increasingly grim. Moreover, investors are realizing that weak software growth rates are being compounded by risks associated with AI. This has triggered a sell-off in public software equities and debt and prompted markdowns on private loans to the sector.

"This is how the cycle turns," Greg Obenshain, head of private credit at asset manager Verdad, told S&P Global Market Intelligence. "Private credit has seen incredible inflows, which allowed them to mask a lot of problems, but markdowns will stop the inflows, which can eventually turn into net outflows."

Debt prices decline

Debt related to software has experienced an abrupt sell-off in recent months, as public software equities were impacted by a series of AI productivity-enhancing products released by Anthropic PBC, including some that make it easier and cheaper to write code.

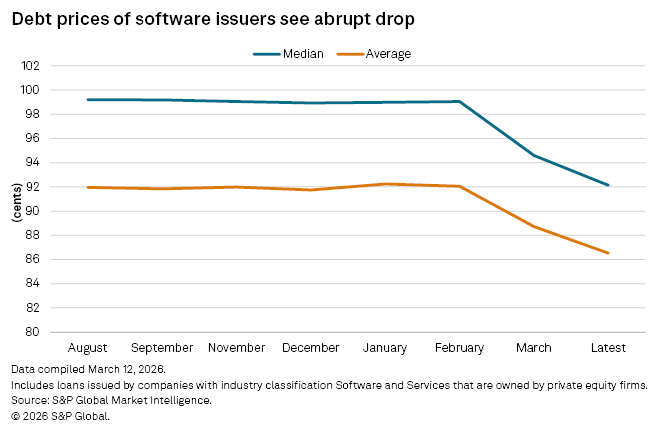

According to S&P Global Market Intelligence data, the median software loan bid price declined to 86 cents in mid-March from 92.2 cents on the dollar in February, approaching depressed territory.

Loans are not typically as volatile as equities and usually move sharply down or up on news regarding a company’s ability to continue paying interest on the loans. The downward move on many loans in software was notable for its scale and speed.

"In software, it is typically not asset-based lending, you are lending on [annual recurring revenue] and growth. Were the underwriting standards too loose? In some cases they were," Gregory Bedrosian, CEO of Drake Star, a tech-focused investment bank, said in an interview with Market Intelligence.

The problems in private credit are "not at crisis levels, but they cannot be ignored," Bedrosian added.

A pandemic era hangover

Unsurprisingly, a large portion of the debt now trading at depressed levels was issued during the COVID-19 pandemic, a time of high software company valuations, cheap debt and laxer underwriting standards. Private equity firms such as Thoma Bravo LP, Vista Equity Partners Management LLC, KKR & Co. Inc. and Francisco Partners Management LP were among the most active acquirers during the pandemic.

At the peak in 2021, private equity firms acquired more than 450 software companies for a total of $101 billion, according to S&P Global Market Intelligence data. Most of these deals were financed with debt, which could run as high as 50% of the total transaction value. Thoma Bravo's latest $12.7 billion acquisition of Dayforce Inc. was nearly half financed with debt.

The total value of deals and deal count fell in subsequent years.

"The worst deals get done in the best of times," S&P Global Ratings analysts said in a recent report. "The year 2021 was characterized by unprecedented monetary and fiscal stimulus, during which loans were underwritten based on high valuations, predicated on the expectation of sustained low rates and readily available capital."

A distant maturity wall

The stress in the software credit industry will make it harder for existing private equity-owned companies to refinance their debt, while new private equity deals in the software sector may be more difficult to finance.

"In general, the noise around private credit has made some lenders more cautious, and ticket sizes are much smaller. Software deals on the smaller size — sub $500 million — are having an easier time to access private credit markets," Scott Twibell, managing director and co-head of technology at investment bank Lincoln International LLC, told Market Intelligence.

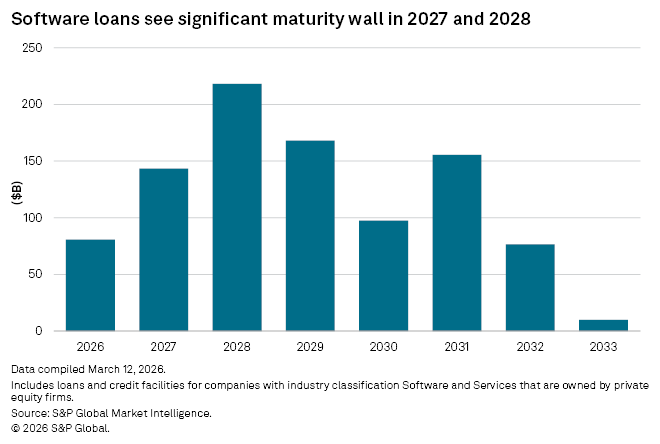

For now, time sides with many of these software companies. A significant portion of loan maturities will not arrive until 2028 and beyond, according to Market Intelligence data. Roughly $386 billion worth of software debt matures in 2028 and 2029, with about $80 billion maturing this year.

However, if fears of AI-driven disruption prove true, the financial health of these companies could deteriorate further in the coming years. This would likely push many credit investors toward the exit, fearing the companies will be unable to refinance or repay their debt at maturity.

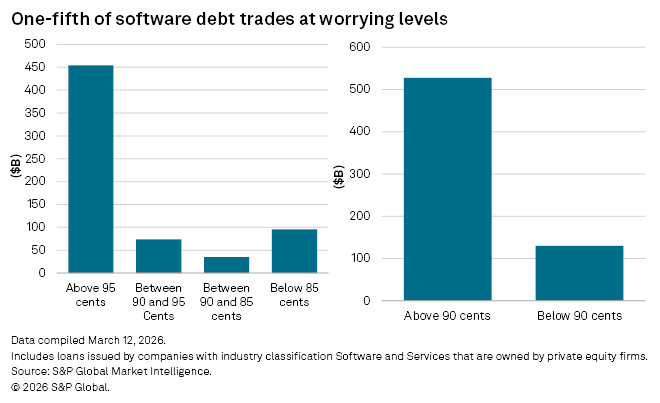

According to a Market Intelligence analysis, about $130 billion of software acquisitions-related loans trade below 90 cents out of a total of $657 billion in loans covered. The loans in the Market Intelligence universe are broadly syndicated loans rather than private credit and are typically rated by ratings agencies.

Loans that trade below 90 cents are often considered to be approaching risky territory, with those trading below 80 cents closer to distress. Around these thresholds, equity also starts to be impaired. Loans are senior to equity, which means that in the event of a liquidation, debt holders get paid first and equity holders last.

According to Twibell, the 2021–2022 software buyouts are "fundamentally good credit" versus the expected return on equity, which is a bigger "unknown."

"The bigger impact on equity has more to do with public software, which takes away an exit opportunity at good value," Twibell said.

Private equity firm Clearlake Capital Group LP has 11 companies with underperforming debt in its portfolio, followed by TA Associates Management LP with 10 and KKR & Co. with five. Clearlake-owned companies that have underperforming debt include Quest Software Inc., whose lowest-graded debt trades at about 25 cents, and Cornerstone OnDemand Inc., which has two term loans issued in 2021 trading below 80 cents.

Clearlake and TA Associates declined to comment.

Pressure mounts on private equity

This environment suggests that returns for private equity firms with heavy exposure to software will likely suffer. Buyout shops have been struggling to exit their investments, as the IPO market has not offered the valuations they require. Consequently, private equity firms have resorted to continuation funds, the practice of transferring holdings from an old fund to a new one to extend the ownership period.

The software sell-off means the IPO window for software is unlikely to open soon. Ashish Patel, a managing director at Houlihan Lokey, said in a recent Market Intelligence webinar that the impact on exit opportunities for private equity and venture capital firms with large software-as-a-service portfolios will likely result in companies staying private longer.

Bedrosian believes that private equity buyers will use more equity to buy tech companies, which could lead to lower valuations.

"Credit is getting tighter and we might be going back to the times when most software deals were funded with equity," Bedrosian said. "That does put pressure on valuations."

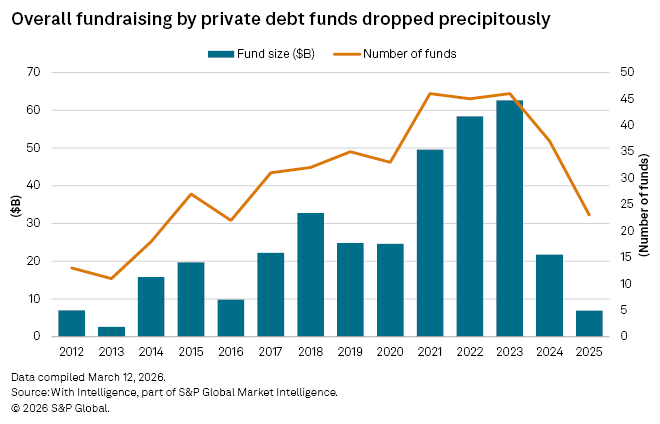

Fundraising fall

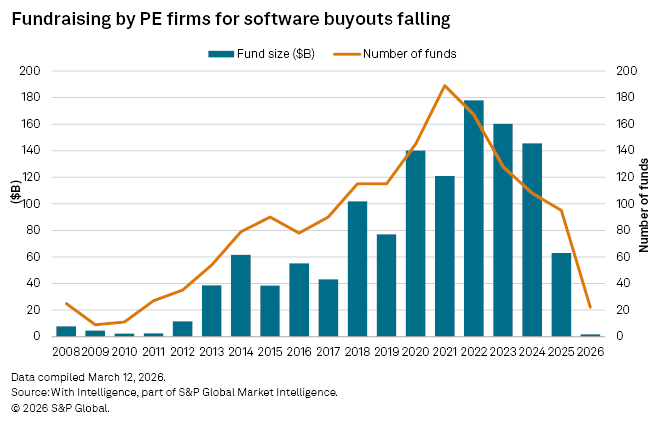

Fundraising by private equity firms has continued to fall since a peak reached in 2021. According to data from With Intelligence, the number of software buyout funds with vintage year 2025 is the lowest since 2017, when growth accelerated.

The picture in private credit fundraising is also bleak, with 2025 seeing the fewest funds launched since 2016, following strong activity between 2021 and 2024.

"The fundamental issue with private credit is that it never made a lot of sense in the way it was marketed, high return with low risk, it was never that," Obenshain said. "Most of the loans will be fine, but a lot won't. What you are seeing now is people understanding this."

Theme

Location

Products & Offerings

Segment