23 Mar, 2026

Demand for private credit to persist amid lower US interest rates

|

|

Federal Reserve Chair Jerome Powell speaks Dec. 10, 2025, at a news conference in Washington, DC, after the Fed cut interest rates for the third time that year. Rate declines could make public bond markets more accessible again for some borrowers without necessarily denting demand for private credit.

Federal Reserve Chair Jerome Powell speaks Dec. 10, 2025, at a news conference in Washington, DC, after the Fed cut interest rates for the third time that year. Rate declines could make public bond markets more accessible again for some borrowers without necessarily denting demand for private credit.Lower interest rates are unlikely to soften borrower demand for private credit in 2026.

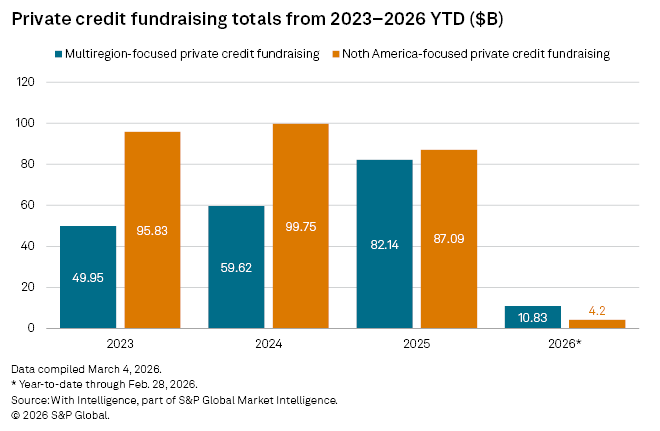

The private credit market has expanded in recent years, with North America-focused funds raising nearly $100 billion in 2024 and more than $87 billion in 2025, according to With Intelligence data. Multiregion private credit funds raised more than $82 billion in 2025, up from nearly $60 billion in 2024.

Higher interest rates push banks and public bond investors to demand higher yields and stricter terms, making it more difficult for middle-market and smaller companies with weaker credit profiles to secure financing from these sources. Those companies often then turn to private credit lenders, which can offer more flexible terms and faster execution.

Even as traditional bank loans and public bond markets have become more accessible of late, many of these borrowers prefer to maintain existing private credit relationships given the economic uncertainty surrounding geopolitical events, tariffs and other factors.

"When you are in a falling interest-rate environment but also experiencing market volatility, like we are now, you would see those types of borrowers continuing to go to the private markets because they offer speed and relationships, and they could be covenant-lite," Nick Tsafos, partner-in-charge at EisnerAmper, said in an interview.

The US Federal Reserve and other central banks raised short-term interest rates throughout 2022 and 2023 to curb inflation after the COVID‑19 pandemic, making it more expensive for companies to borrow. Policymakers then eased rates in 2024 and 2025 as inflation cooled. Thus far in 2026, the Fed has held steady, though a majority of officials on the rate-setting Federal Open Market Committee expect to cut that benchmark rate at least once more before the end of the year despite uncertainty surrounding the effects of the war in the Middle East.

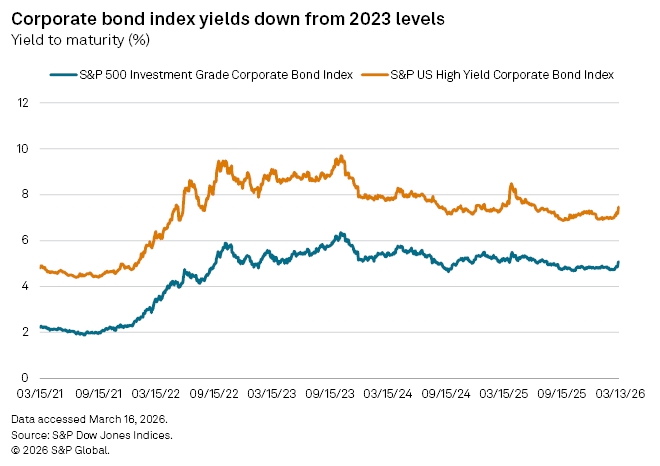

The yield on the five‑year US Treasury note, a key benchmark for medium‑term financing, stood at 4.01% as of March 20, down from its most recent peak of nearly 5% in late 2023, according to S&P Global Market Intelligence data.

Private credit borrowers, often private equity‑sponsored companies, generally still pay higher interest rates than they would in public markets, given their risk premiums, deal complexity and the relative illiquidity of private credit assets compared to public bonds. Lenders have leaned into relationship-building and flexibility to justify these higher costs.

"There is a premium there that these borrowers are willingly acknowledging and buying because they know that they're brokering a relationship for the next several years with parties on the other side who, when times are bad, are going to be able to respond quickly and also have quite a bit of dry powder to help them grow," Derek Ladgenski, a partner at Katten, said in an interview.

Investor demand

Lower interest rates stand to boost institutional investors' relative appetite for private credit assets this year compared to public debt and other fixed-income vehicles. This would follow several years of strong demand for both private credit and higher‑quality, lower‑risk public bonds when higher interest rates pushed up yields in both asset classes.

"It opened up more appetite for the public market bonds during the period of higher rates when investors didn't necessarily have to take the credit risk of going into the sponsor-backed type of companies," Olaolu Aganga, head of portfolio construction at Citi Wealth, said in an interview.

Yields on corporate bonds have declined from 2023 levels, thanks to lower interest rates and tighter spreads. Higher yields available from alternative assets like private credit will serve more strategic roles in institutional portfolios. Pension funds, insurers and endowments searching for higher returns will "need that type of yield," Aganga said.

Institutional investors with longer investment horizons can more readily accept the risks of holding illiquid private credit assets, often to maturity, in pursuit of higher potential returns.

"If borrowers are willing to compensate investors with adequate illiquidity premiums in exchange for certainty of execution and a concentrated stakeholder base, then each market [public and private] will get its fair share," Vinod Chandiramani, head of the capital advisory group at Solomon Partners, told Market Intelligence.

With Intelligence is part of S&P Global Market Intelligence.

Theme

Location

Products & Offerings

Segment