18 Mar, 2026

Basel III endgame unlikely to revive banks' mortgage appetite

By Zoe Sagalow

Mortgage capital relief is unlikely to bring banks back into the home lending business as other factors discouraging them from participating persist.

The federal banking regulators are hoping to reignite banks' mortgage lending and servicing activity with the upcoming Basel III endgame rule by relaxing capital requirements. While the industry will welcome the change, it is unlikely enough to lure banks back to the mortgage market, advisers told S&P Global Market Intelligence. Steep hurdles that remain, such as ever-increasing competition from nonbanks, the high capital needed to operate the low-margin business line and persisting regulatory hurdles, will keep banks on the sidelines, they said.

"When you beat up a product line in a highly regulated institution, people's memories last, and just changing one capital provision, positive though it is, won't make all that go away, won't make the higher level of scrutiny and compliance reviews go away, won't make the more stringent examination procedures go away," Brian Graham, partner at Klaros Group LLC, said in an interview. "There's a bunch of stuff that came together to push an entire sector largely out of the US banking system, and it's going to take more than one or two steps to bring it back in."

In the upcoming Basel III endgame proposal expected to be unveiled March 19, the federal regulators plan to allow banks to include mortgage servicing assets in regulatory capital ratios at the current 250% risk weight and tailor current mortgage risk weights to each loan, such as through loan-to-value ratios, rather than uniform risk weights, according to a Feb. 16 speech from Federal Reserve Vice Chair for Supervision Michelle Bowman.

"Even if both of those things happen and happen in a way that's positive for banks' participation in the mortgage market, I don't think that's changed a lot of the other dynamics that have caused banks to view this as more challenging," Graham said.

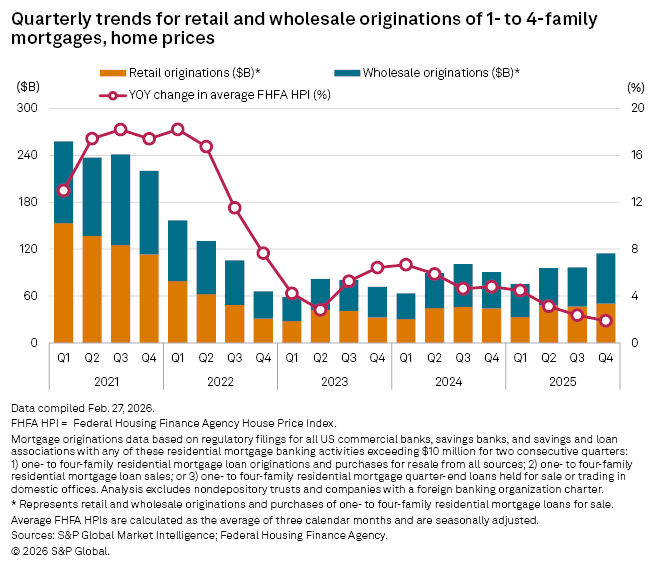

US banks' mortgage originations surged to a three-year high in the fourth quarter of 2025, but still lags previous years' levels, according to Market Intelligence data.

Nonbank competition is one major factor causing banks to leave the mortgage lending segment. In a recent example, Oregon-based Willamette Valley Bank announced in February that it was exiting home lending in part due to the growth of online and nonbank lenders.

Nonbanks have been able to gain market share in the wake of more stringent regulations around mortgage lending and servicing after the 2008 financial crisis. Those changes also made it more challenging for banks to profit from mortgage servicing businesses.

"It was overkill on regulation. So I think [Bowman is] on the right track," Chip MacDonald, managing director of MacDonald Partners LLC, said in an interview. However, "I'm not sure that it's a capital issue as much as it's other regulation, and the fact that now the banks moved away from it. Mortgage servicing is a low-margin business."

In addition to it being low-margin, it is also labor intensive and costly.

"The paperwork is enormous. The diligence is enormous — the financial checking and the back and forth. It's a people-intensive business, which means in today's world, it's expensive," MacDonald said. "It's going to take investments by the banks to get back into the business in a big way."

A recent executive order from President Donald Trump is seeking to solve some of those hurdles by encouraging federal regulators to reduce banks' mortgage lending burdens by digitalizing the mortgage origination process, streamlining documentation requirements, and focusing exams on underwriting rather than process and technical compliance.

The order aims to "promote portfolio mortgage servicing as a core community banking function and otherwise take other actions that lower barriers to entry and costs of operation for community banks in the mortgage lending business," according to a fact sheet.

Community banks that maintained their mortgage servicing and lending arms would benefit from the capital changes, though large banks that have pulled back in recent years would find it hard to shift gears and reenter the space.

"There are certainly banks out there that are more agile themselves ... but not the biggest ones that we think of that have classically had all this," said Eric Edwardson, partner at law firm Mayer Brown who advises on residential mortgage banking and more. "Trying to transition themselves, their culture and all that to something that is more like these independent mortgage banks would be real tough, a tough road for them to go down."