02 Mar, 2026

AES shares fall after long-awaited $10.7B take-private acquisition is announced

By Allison Good

AES Corp. shares tumbled March 2 after the company announced a consortium led by BlackRock Inc. subsidiary Global Infrastructure Management LLC and EQT AB agreed to take it private for $10.7 billion.

The all-cash deal, which includes the California Public Employees' Retirement System and the Qatar Investment Authority as co-underwriters, values AES shares at $15 each and carries an enterprise value of approximately $33.4 billion, including assumed debt.

The Arlington, Virginia-headquartered utility and renewables company's stock price, meanwhile, was down 17% at about 3:30 p.m. ET in heavy trading on March 2, to $14.30 per unit, after surging to $17.28 on Feb. 27 on reports that a deal with the private equity giants was imminent.

Though the transaction represents a 40.3% premium to AES' 30-day volume-weighted average share price before July 8, 2025, the last full trading day before the first media report of a potential acquisition, analysts at Jefferies called the deal value "disappointing" for shareholders in a March 2 note to clients.

In a presentation to investors accompanying the deal announcement, AES said that without the merger, which is expected to close in late 2026 or early 2027, the company would have had to "materially reduce or eliminate [the] dividend and or issue significant equity at potentially unfavorable terms, possibly as soon as 2026."

"Substantial" capital needs for funding the infrastructure buildout to serve data centers, combined with rising equipment prices and the "future expiration of tax credits" after federal legislation eliminated incentives for wind and solar projects, drove AES to pursue the deal, according to the presentation.

AES remains an attractive target given "the acceleration of AI-driven power demand growth, while the company has also provided a clear line of sight for incremental earnings growth in the near-term underpinned by its large contracted renewables backlog," analysts at CreditSights wrote in a March 2 report.

The company announced Feb. 24 that it will provide colocated power for a data center under development by Google LLC, a subsidiary of Alphabet Inc., in Wilbarger County, Texas.

AES acknowledged in the presentation that "cash generation in the US is modest in the early years" for renewable energy projects, prompting potential concerns about the sector more generally.

"Others in the space such as [NextEra Energy] are in a much better financing position with a higher quality balance sheet, but we can't help but see this as a clear negative read-through to returns for the business model which all management teams in the space have argued are higher on the back of data center demand and higher power prices generally," Barclays analysts said March 2.

Jefferies, meanwhile, anticipates more similar transactions "as part of the ongoing 'swap' where private equity has brought to public market legacy fossil assets and taken private clean energy assets" like Atlantica Sustainable Infrastructure Ltd.

AES shares began struggling following a series of aggressive Federal Reserve rate hikes in 2022 that dampened the company's stock price, prompting it to pursue billions of dollars of asset sales in both the US and Latin America and initiate a restructuring plan in 2025 aimed at cutting costs and focusing on fewer but larger renewable projects.

AES noted in the March 2 presentation that "the potential pool of remaining sale candidates is limited."

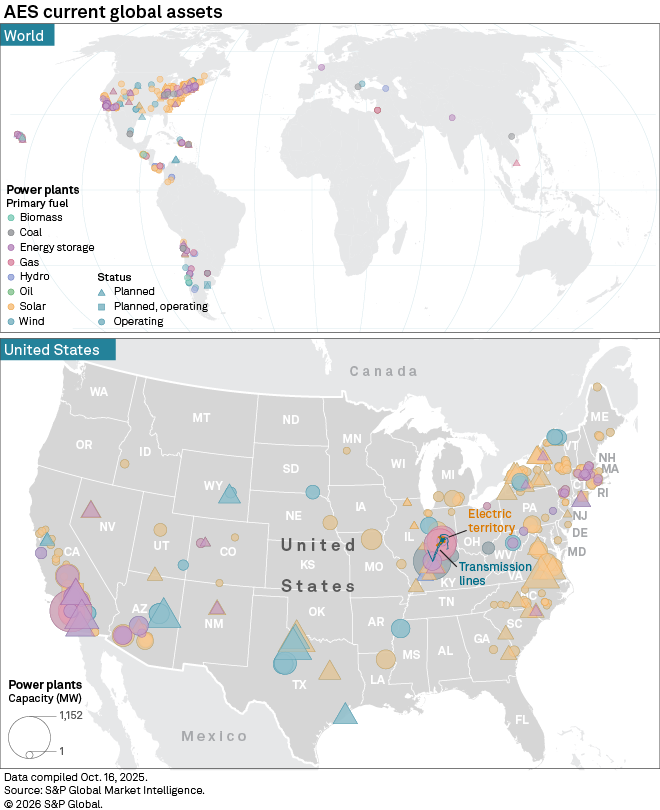

The take-private deal's completion is subject to approvals by the Federal Energy Regulatory Commission and a number of state utility regulators. Its holdings include two regulated electric utilities, AES Indiana, in and around Indianapolis, and The Dayton Power and Light Co., also known as AES Ohio.

If the merger still lacks regulatory approvals by June 1, 2027, either party can terminate the transaction after two successive three-month extension periods, according to a March 2 SEC filing. The consortium would be required to pay AES a termination fee of $100 million or approximately $588 million, depending on specific circumstances, while AES would have to pay the consortium approximately $321 million.