18 Feb, 2026

US banks report robust loan growth in Q4 2025

By Robert Clark

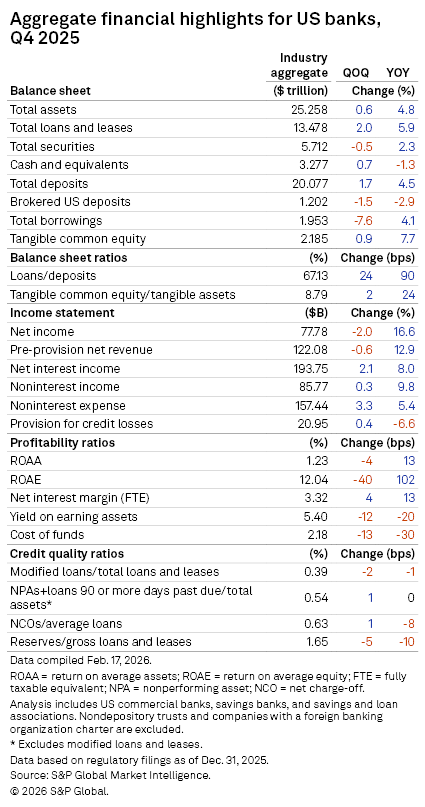

US banks posted the second-highest aggregate loan growth rate in the last three years in the fourth quarter of 2025.

US commercial banks, savings banks, and savings and loan associations, excluding nondepository trusts and companies with a foreign banking organization charter, reported total loans and leases of $13.478 trillion as of Dec. 31, 2025, up $267.80 billion or 2.0% sequentially, according to data from S&P Global Market Intelligence. That growth trumped the 1.2% growth rate in third quarter 2025, and the average quarterly rate for the last three years of 0.8%. It nearly matched the highest loan growth rate in the last three years — 2.1% in the second quarter of 2025.

Much of the loan growth came from the largest institutions. The four biggest banks by total assets at 2025-end — JPMorgan Chase Bank NA, Bank of America NA, Citibank NA and Wells Fargo Bank NA — each grew loans by at least 1.6% and accounted for 43.1% of the total change in loans. And the top 20 banks, all of which reported higher loan balances except for TD Bank NA and Fifth Third Bank NA, represented 70.4% of the total growth.

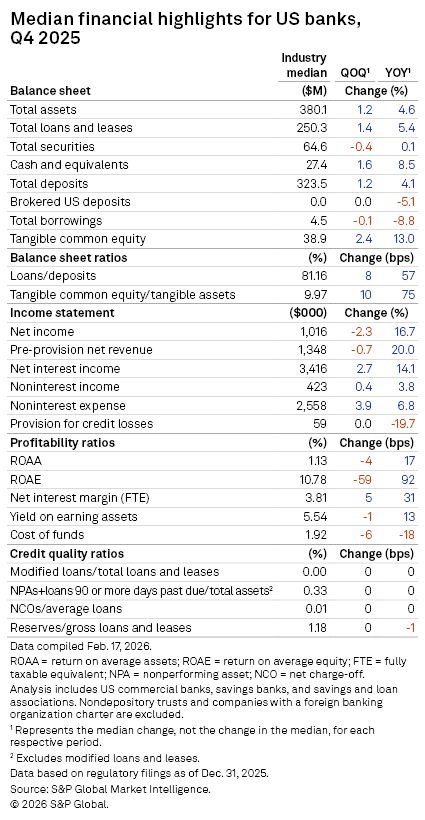

While the loan growth was top-heavy, it was still widely dispersed throughout the industry. The median rate last quarter was 1.4%, up from 1.3% in the third quarter of 2025 and matching the three-year average.

This analysis, which covers US commercial banks, savings banks, and savings and loan associations, examines fourth-quarter 2025 financial performance based on aggregate and median change because the sector remains dominated by larger institutions that can skew the results. For instance, the four largest banks held about 40% of the industry's assets as of Dec. 31, 2025.

NDFIs still driving loan growth

Outstanding loans to nondepository financial institutions (NDFIs) increased by more than $106 billion, or 7.3% quarter over quarter, representing nearly 40% of the aggregate growth in total loans and leases. The private equity category showed the highest increase, up $37.24 billion, or 11.2%. Loans to business credit intermediaries, consumer credit intermediaries and mortgage intermediaries went up 7.5%, 7.2% and 6.0%, respectively.

A small portion of the fourth-quarter NDFI growth was from reclassifications, according to the Federal Reserve's notes on H.8 data. For the week ended Oct. 1, 2025, domestically chartered commercial banks shifted $4.0 billion to loans to NDFIs from commercial and industrial (C&I).

Several banks with more than $1 billion in loans to NDFIs as of Dec. 31, 2025, reported double-digit percentage growth sequentially. The top two banks by percentage growth were Stifel Financial Corp. subsidiaries Stifel Bank and Stifel Bank and Trust. The former expanded NDFI loans to $3.36 billion from $62.8 million, and the latter moved up the outstanding balance to $1.67 billion from $350.8 million.

The nation's largest bank by total assets, JPMorgan, was the top NDFI lender with $237.85 billion of outstanding loans. Still, the bank's 5.2% NDFI loan growth rate lagged the broader industry, but it outperformed the industry in many other segments.

JPMorgan grew credit card loans by 6.0% quarter over quarter, above the industry's 4.6% growth rate. JPMorgan was the second-largest credit card lender by outstanding balance as of Dec. 31, 2025.

For the construction and land development sector, JPMorgan diverged from the aggregate, showing 8.8% sequential growth versus a 1.5% decline for the industry. JPMorgan also exceeded the industry aggregate growth rates for non-owner-occupied commercial real estate, C&I, multifamily and one- to four-family.

Success on the other side of the balance sheet

US banks also grew the other side of their balance sheet in the 2025 fourth quarter, with an aggregate deposit growth rate of 1.7%,

Additionally, the composition of those deposits improved. In aggregate, banks reduced reliance on brokered US deposits by 1.5%. JPMorgan accounted for the majority of the decrease, reporting a 21.0% reduction but still grew total deposits by 1.8%. Other banks that cut brokered US deposits and had a higher growth rate in total deposits relative to the industry aggregate included SoFi Bank NA, Axos Bank, Citibank and PNC Bank NA.

– Download a template to compare a bank's financials to industry aggregate totals.

– Set email alerts for future Data Dispatch articles.

The industry also curtailed dependence on borrowings, which decreased $160.41 billion, or 7.6% sequentially on an aggregate basis. JPMorgan alone shed more than $100 billion of borrowings. Banks that cut borrowings by more than one-third included SouthState Bank NA and Hancock Whitney Bank, as well as SoFi, which eliminated all of its borrowings amid an 18.9% jump in non-brokered US deposits.

SoFi is winning deposits by staying competitive on rates, CEO Anthony Noto said on a Jan. 30 earnings conference call. "I think as rates continue to go down, our advantage will make itself more clear," he said.

A more favorable funding mix, along with Federal Reserve rate cuts, lowered the industry's cost of funds by 13 basis points in aggregate and 6 basis points by median. As funding costs fall faster than yield on earning assets, most banks experienced margin expansion.

Net income and pre-provision net revenue were down quarter over quarter on both an aggregate and median basis as higher margins combined with loan growth to partially offset elevated noninterest expense levels.