09 Feb, 2026

Geopolitical strains unlikely to spark foreign flight from US Treasurys

By Nick Lazzaro

|

|

Major foreign investors are unlikely to significantly reduce their US Treasury holdings even as geopolitical tensions with the US raise concerns about "sell America" trades.

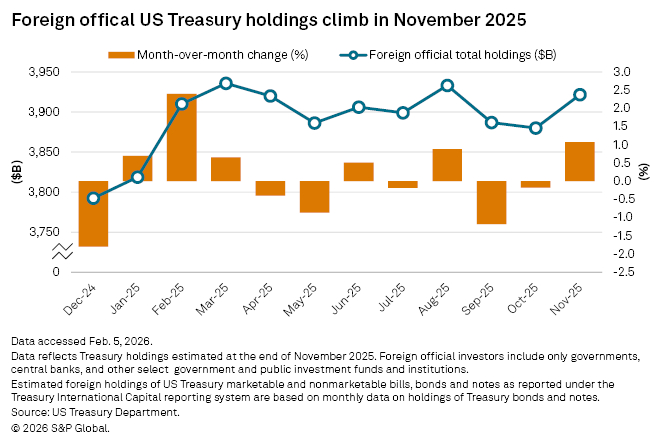

Foreign official investors held $3.922 trillion in US Treasury securities at the end of November 2025, and total foreign holdings reached a record $9.355 trillion, according to the latest US Treasury Department data. Official holdings in November were above a 12-month average of $3.891 trillion and up from $3.886 trillion at the end of May 2025, following a two-month decline that coincided with the announcement of broad US tariffs last April. Foreign official investors include governments, central banks, and other select large investment funds and institutions.

The tariffs on most nations sparked international trade tensions and raised concerns of significant foreign capital outflows from US assets, either in retaliation or to reduce perceived investment risks. These worries resurfaced in January when a US proposal to acquire Greenland faced opposition from European leaders. However, official data and capital flow trends show little evidence of foreign flight from Treasurys, and while such a scenario remains possible, it is unlikely, according to Ed Al-Hussainy, a portfolio manager and global rates strategist for Columbia Threadneedle.

"There are no liquid, high-quality collateral alternatives to US Treasury securities," Al-Hussainy told S&P Global Market Intelligence. Moreover, bond markets in other large economies such as those in Europe and China "are either too fragmented or behind capital controls, which makes them unsuitable as an alternative to Treasurys and the broader US dollar financial system," Al-Hussainy said.

A sudden foreign sell-off of Treasurys could rapidly increase supply. This would lower their prices and increase their yields, as these two factors are inversely related. A spike in Treasury yields would drive up interest rates throughout the US economy. Additional impacts would include volatility for the US dollar and exchange rates, stress in banking systems, higher debt servicing costs for the US government and further geopolitical tensions.

Recent trading data has not shown abnormal foreign outflows from US assets, although diverging trends may be emerging across regions.

"In 2025 there were record inflows overall in the US capital markets, particularly the equity markets, but still generally positive in Treasurys," Grant Johnsey, head of market solutions for the Americas at Northern Trust Asset Servicing, said in an interview. "We are seeing that continue for European investors to start the year but not for Asian investors, where we have seen two months in a row [December 2025 and January 2026] of fairly sized Treasury selling."

Risks of Treasury sell-off for foreign investors

Major foreign investors would likely hesitate to rapidly sell Treasurys, as such a move would also pressure their own economies and financial systems, Al-Hussainy with Columbia Threadneedle said.

These risks could be especially pronounced in major exporting countries such as China.

"It's mutually shared destruction," Gary Pzegeo, managing director and chief investment officer for CIBC Private Wealth, said in an interview. "If China decides to sell holdings, where is it going to go with that capital? Or does it risk losing the US consumer, which has supported its economy?"

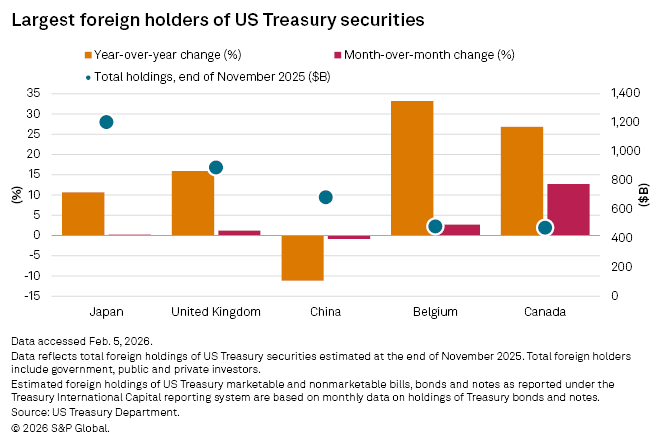

Treasurys held by institutions in China, the third-largest foreign holder of US bonds, declined by more than 11% year over year in November, but this downward trend began years earlier as the country diversified its assets, including a buildup of its gold reserves.

"China has slowly diminished its position, but it is still a stalwart holder of dollars in the global capital markets and the global reserve banking system," Pzegeo said.

Even as China gradually trims its Treasury holdings, this reduction would be limited because it will "get to a point where it just can't replace Treasurys with something else of equal liquidity and equal safety," Pzegeo said.

While countries would risk damage to their own financial systems, the US may be able to protect itself against the fallout.

"The US government will not allow the US dollar-dominated financial system to be undermined by foreign governments," Al-Hussainy said. "The US will proactively use the US Treasury, the Federal Reserve and the broader foreign and economic policy apparatus to arrest any major foreign selling, because that would present a risk to US dollar hegemony and raise domestic financial sector risks in the US."

Other driving factors

Foreign investors could be driven to trim their exposure to US assets by several fundamental factors beyond political influences. For example, caution could increase toward Treasury holdings as issuance rises to fund an expanding US federal deficit.

"There is some element of the 'sell America' trade that might recognize that long-dated US Treasurys in particular are not the haven asset that they once were," Isaac Wheeler, head of balance sheet strategy at Derivative Path, said in an interview. "You see long-term yields sticking where they are, even going a little bit higher, and that could speak to a wariness around the Treasury market."

The 10-year US Treasury yield has mostly traded between 4.0% and 4.3% since August 2025, according to Market Intelligence data as of Feb. 4.

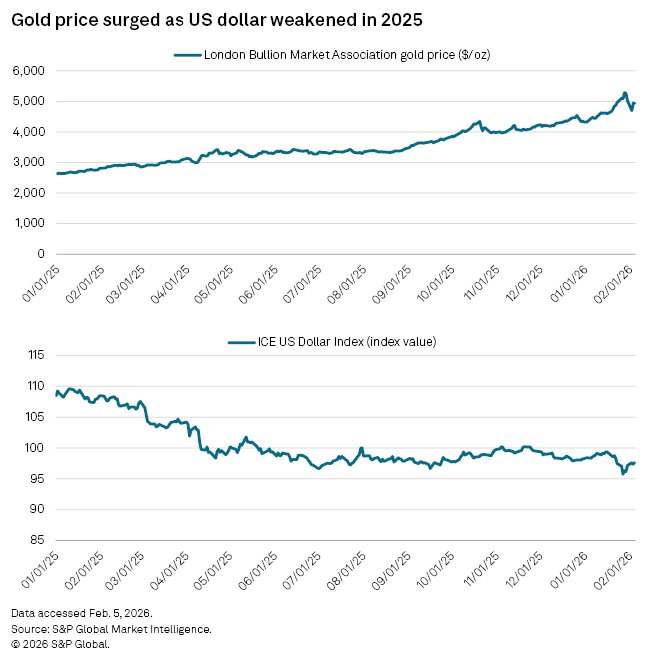

A consistently weaker US dollar since the beginning of 2025 has also driven foreign institutions to hedge against US dollar-denominated assets. This may have partially contributed to the surging price of gold over the past year, with the London Bullion Market Association price of gold reaching a record $5,284.55 per ounce on Jan. 28.

"That driver was more speculative than it was fundamental, but that trend of movement away from the dollar or diversification by reserve banks out of dollars likely has a longer shelf life and supports further appreciation of other assets, whether that be other currencies or stores of value like gold," CIBC Private Wealth's Pzegeo said.