04 Feb, 2026

Fed rate cuts hinge on possibly hard-to-gauge job market deterioration

By Brian Scheid

An increasingly opaque US labor market is likely to keep the Federal Reserve from cutting benchmark interest rates until the summer, if officials even lower rates at all in 2026.

With inflation moderating and a new neutral rate in sight, the Fed is unlikely to move rates in the near term unless there is a substantial weakening of the jobs market, a growing number of economists and market strategists believe. Just how substantial that weakening would have to be is the source of fierce debate as consumer confidence plunges, Fed Chairman Jerome Powell's tenure as the head of the central bank nears an end, and another government shutdown has threatened the release of new jobs and inflation data.

President Donald Trump, who has launched an unprecedented campaign to pressure the Fed to lower rates, on Jan. 30 named Kevin Warsh, a former Fed governor, to take over as chairman when Powell's term expires in May. While Powell could stay on as a member of the Fed's board until 2028, he may have announced his last rate move in December 2025, when the rate-setting Federal Open Market Committee (FOMC) agreed to cut the benchmark federal funds rate by 25 basis points for the third straight meeting. The FOMC kept rates unchanged at their January meeting.

In the near term, another cut appears to be a long shot and likely depends on the state of American jobs.

"It's going to take clear labor market deterioration," said Oren Klachkin, a financial market economist with Nationwide. "Unless there's a clear change in the balance of risks ... the Fed is on hold until Warsh takes the helm."

For now, the majority of the futures market does not expect the Fed to cut again until June, and the majority expects two cuts or fewer before the end of 2026, according to CME FedWatch.

What could trigger the next cut is unclear, though a rise in layoffs and firings could be a key motivator, said Jim Baird, chief investment officer with Plante Moran Financial Advisors.

"With fewer individuals entering the workforce, a slower pace of hiring could be tolerated as long as the unemployment rate doesn't resume a sustained upward climb and the pace of layoffs doesn't accelerate meaningfully," Baird said. "Any indications that employers are increasingly leaning into trimming their payrolls would be a red flag that would be tough for the Fed to ignore."

During his Jan. 28 press conference after the Fed's latest meeting, Powell said that by bringing the Fed's benchmark rate near neutral, the labor market will be near stable. Still, with multiple warning indicators, such as declining measures of job availability, the rise of Americans working part-time for economic reasons, and the fall in both labor supply and demand "makes it a difficult time to read the labor market," Powell said.

Fed Governor Christopher Waller, one of two FOMC members to vote for another 25-bps cut at the January meeting, said the labor market "remains weak" with "zero" growth in payroll employment in 2025.

"This does not remotely look like a healthy labor market," Waller said in a Jan. 30 statement, pointing to weakness in labor demand and the likelihood of layoffs in 2026. "This indicates to me that there is considerable doubt about future employment growth and suggests that a substantial deterioration in the labor market is a significant risk."

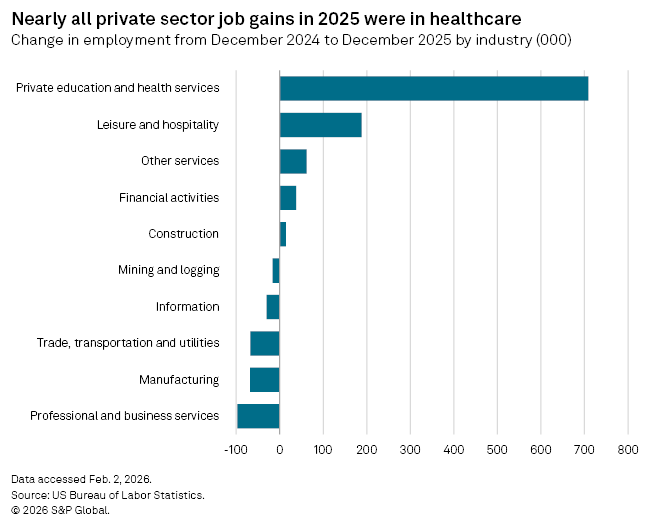

To seriously consider a cut, Fed officials would need to see further declines in private sector payrolls, outside the healthcare and social assistance sector where the majority of job gains have taken place over the past year, said Elias Haddad, global head of markets strategy with Brown Brothers Harriman.

The hiring and quit rates would need to drop as well, while the overall labor force participation rate would need to fall and the unemployment rate would need to move higher, Haddad said.

If there is broad weakening in the labor market, the Fed could seriously consider another rate cut in March, said Thomas Simons, chief US economist at Jefferies.

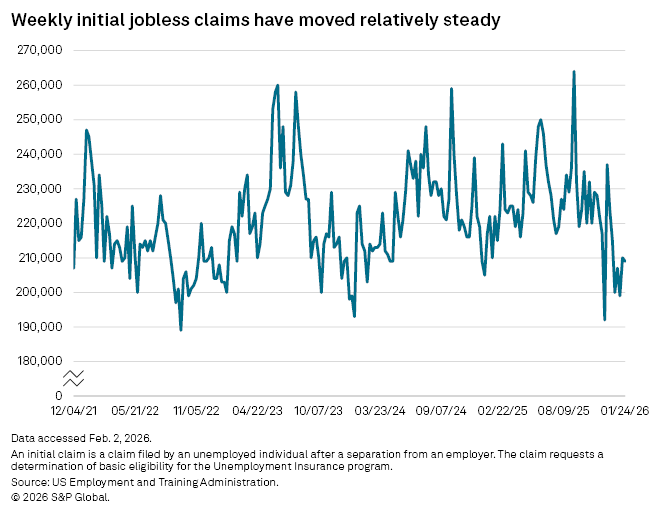

The deterioration in the labor market needed for a cut would be a combination of factors, including downward revisions to payrolls, a slowdown in healthcare hiring, and a jump in layoffs and jobless claims, Simons said.

"A lot of things need to fall into place in the data in order for it to happen," Simons said.

Tracking whether this is taking place is complicated, at least in the near term, by the latest partial government shutdown that began Jan. 31. Congress approved a spending plan on Feb. 3 to end the partial shutdown, though key labor market data, including the monthly job openings and labor turnover survey, scheduled for release Feb. 3, and the January jobs report, scheduled for release Feb. 6, will likely be delayed, according to the US Bureau of Labor Statistics.

Higher unemployment

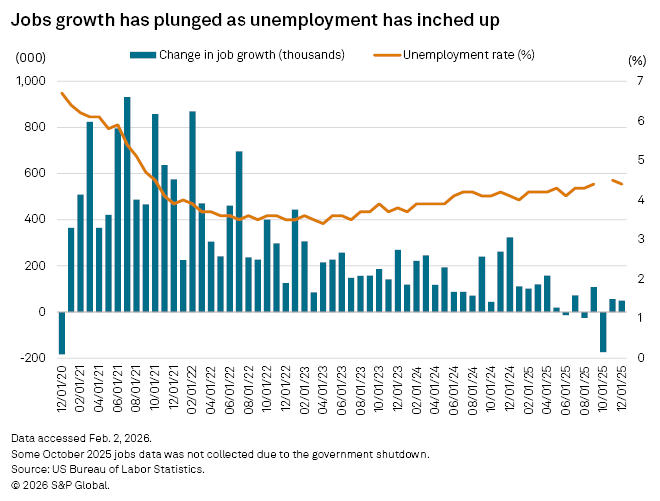

US unemployment was 4.4% in December, up from 4.1% a year earlier, though it is moderating. Joblessness would have to see a much more significant uptick to motivate a near-term cut.

"If you see unemployment breach 5% ... I think this is the most likely catalyst to see the Fed front-load more rate cuts than what is currently expected," said Kevin McCullough, portfolio consultant at Natixis Investment Managers.

With unemployment "little changed" over the past 18 months, rates may not be restrictive and could already be a benefit to the jobs market, said James Egelhof, chief US economist at BNP Paribas.

"A sustained spike in unemployment would probably convince the Fed it needed to do more as it would suggest that monetary policy is actually still tight and is dragging down labor demand," Egelhof said.