11 Feb, 2026

Credit card lenders' interest rates not at risk, for now

By Claire Lawson and Zain Tariq

US credit card lenders'

A 10% cap on credit card interest rates would be a dramatic step down for certain lenders, with some rates stretching up toward 30%, an analysis by S&P Global Market Intelligence found. However, lenders will likely be able to keep rates where they are at as the probability of a credit card rate cap is very low, according to policy analysts.

Among the available rates for the top 20 banks by credit card balances, the mean average rate was 18.32%, while the median average rate was 17.62%.

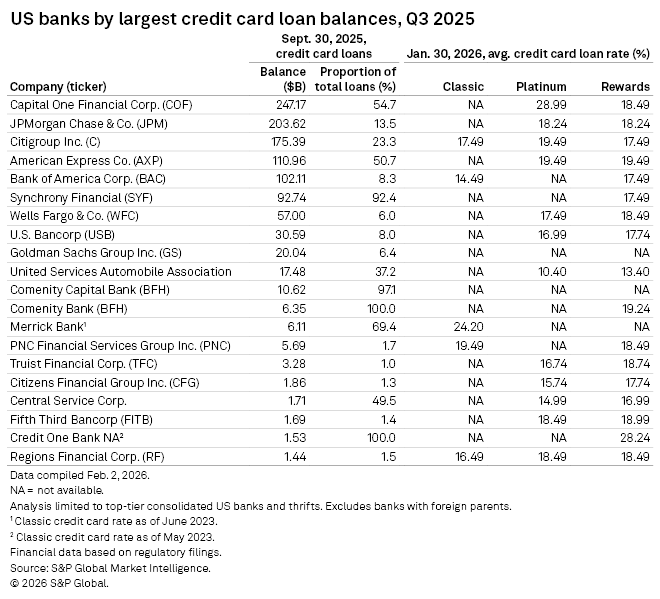

Available top-20 platinum-level cards carried a median rate of 17.87%, with a highest average rate of 28.99% from Capital One Financial Corp. The company is also fairly exposed to credit card lending, with 54.7% of its total loans in that space at Sept. 30, 2025.

Capital One also had the largest credit card balance total among US banks, at $247.17 billion.

For most US banks, credit cards do not hold too much sway over their loan portfolios, but for a select few, a rate cap could do heavy damage to their operations. Credit card loans accounted for over 10% of loans for 10 banks and over 25% of loans for six among the top 20 top-tier consolidated US banks and thrifts by credit card loan concentration, excluding those with foreign parents or without available rates data for 2026.

Comenity Bank, a subsidiary of Bread Financial Holdings Inc., had a loan portfolio entirely comprising credit card loans, with a $6.35 billion balance. The next-highest credit card lender by proportion of its loan portfolio was Synchrony Financial with its $92.74 billion in loans making up 92.4% of its loan portfolio.

Low likelihood of progress

The possibility of a credit card rate cap remains low because it would require congressional approval, and right now, the agenda item lacks support from key lawmakers, according to policy analysts.

"The Republican leadership doesn't seem to think it's a good idea," Capital Alpha Managing Partner Ian Katz

For now, Trump might concede the possibility, but he could push for it again if inflation picks up, Aaron Klein, a Brookings Institution senior fellow in economics studies, said during a Jefferies fireside chat, published in a Jan. 27 research note.

"So, if inflation were to decline in other sectors, Trump would be less concerned about this. If inflation picks up in other sectors, he's going to be throwing more spaghetti at the wall to try to reduce pricing, reduce costs, for his base," Klein said.

While legislation is likely out of reach, Trump's support of the idea could drive the industry to act, Katz said.

"What you're going to see is the industry, the banking industry, the credit card issuers making some sort of conciliatory gestures toward the White House on this. ... It allows everybody to declare victory to some extent," Katz said. "Some of the banks will offer credit card products or certain cards with a lower rate, perhaps as low as 10% with conditions, maybe for certain clients; there'll be a lot of stipulations."

Industry opposition

Banking industry executives have come out strong against the possibility. During fourth-quarter 2025 earnings, JPMorgan Chase & Co.'s CFO called the move "very bad," while U.S. Bancorp's CEO called it "crushing" and detrimental."

At Sept. 30, 2025, JPMorgan had the second-most credit card loans at $203.62 billion, or 13.5% of total loans, for an average rate of 18.24% for both platinum and rewards cards. U.S. Bancorp had $30.59 billion in credit card loans, or 8% of total loans, with an average rate of 16.99% for premium cards and 17.74% for rewards cards.

If the rate cap went through, it would "upend the economics of credit card issuance today," Morgan Stanley analysts wrote in a Jan. 21 note. Any rate cap would slash credit availability for nonprime customers, reduce credit card rewards and potentially lead to higher fees, especially if the cap was permanent or long-lasting, the analysts said.

Transactors — customers that pay credit cards off in full — would see minimal effect. Revolvers, who carry a monthly balance, would experience major reductions in access, lower limits, tighter underwriting and higher fees, driving consumers toward buy-now, pay-later alternatives, reducing consumption and disrupting credit scores and bank profitability, Brookings' Klein said.