10 Sep, 2025

US bank charter applications surge, dominated by nonbanks

By Claire Lawson and Xylex Mangulabnan

Financial technology companies and nonbanks, emboldened by a more permissible regulatory environment, have lined up for bank charters in 2025.

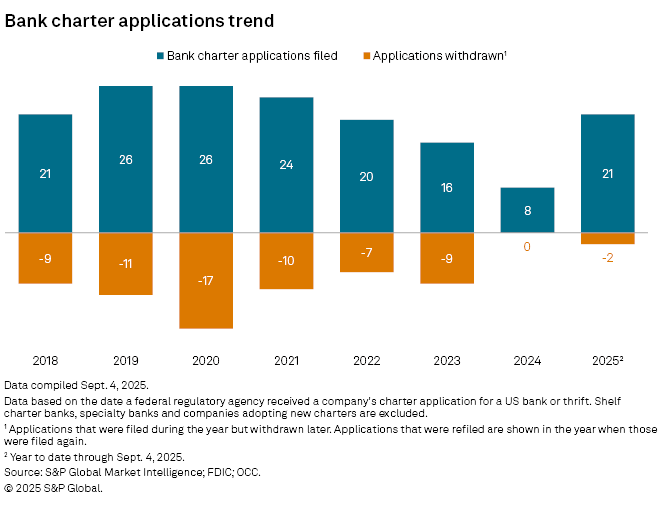

US bank charter applications have surged this year with 21 applications filed through Sept. 4, over double the number of applications in full year 2024 and setting up 2025 to have the most applications since 2020. The majority of those have come from either financial technology companies seeking national trust bank charters with the Office of the Comptroller of the Currency (OCC) or nonbanks seeking industrial loan company (ILC) charters from the Federal Deposit Insurance Corp.

"You have a major chess match playing out here that is broader than stablecoins that some companies believe is a once-in-a-blue moon opportunity," Richard Rosenthal, Deloitte & Touche LLP principal, said in an interview. "People are looking at this and saying, 'If I wanted to do this business, if I wanted to accept deposits, if I wanted to have access to the payment systems, let me try now. This is may be my best shot.'"

In the three-month span between April 18 and July 21, six

Less regulatory scrutiny after years of crackdowns on fintechs' involvement in the bank space is one of the major forces driving the upswing in applications, said Mayer Brown partner Matt Bisanz in an interview with S&P Global Market Intelligence.

"People now know that they will get a fair hearing before the regulators on their application, whereas before there was just years of delay and a lot of skepticism from regulators towards fintech involvement in the banking system," he said.

The Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, which passed July 18, is also emboldening these companies, as it clarified that an uninsured nonbank entity must be under the supervision of a regulatory agency to issue or hold customers' stablecoins, such as through the OCC's national trust bank charter.

The GENIUS Act seemed to be "setting [the national trust bank charter] up as a path" for companies interested in stablecoins, Bisanz said. There is an "idea that national trust banks are going to become a participant in the stablecoin ecosystem," he added.

Community banks are worried as nonbanks increasingly seek bank charters, and as both nonbanks and large bank competitors look to get involved in cryptocurrency custody and stablecoin payments.

A recent survey by IntraFi conducted in early July revealed that 48% of the 455 bank executives respondents believed their bank would need to explore new products or services, including stablecoins, as a result of the GENIUS Act and recent large bank announcements, and 35% are "very concerned" about nonbank companies such as Walmart or Amazon muscling into the space.

"If there was a traditional bank that wanted to offer cryptocurrency custody, then that consumer or other end user may not choose the bank because now one of these nonbank entities that gets a national bank [charter] can do it itself," said James Stevens, partner and co-leader of Troutman Pepper Locke's Financial Services Industry Group, in an interview.

In addition to losing out on customers, banks could experience deposit cannibalization when customers move cash into stablecoins, and there could be increased competition for banks with large payments businesses, the Deloitte advisers said.

"Sitting on the sideline and just waiting for things to transpire is most likely a wrong strategic move ... if you are a bank," said Roy Ben-Hur, managing director in Deloitte's Risk and Financial Advisory practice. "Sitting around and doing nothing is going to create fundamental risk and threat for those banks."

Nonbank-run stablecoins could increase competition for banks on payment-related fee income and traditional, noninterest-bearing deposits, which could then constrain lending capacity, according to a report by Moody's Ratings published July 7.

"Increased stablecoin issuance is likely to put pressure on bank profitability and intensify competition from non-bank financial services firms and fintechs, which continue to demonstrate agility in adopting digital assets and emerging technologies," the report said.

The American Bankers Association released a similar statement following the GENIUS Act's passage, pointing out disruption-related concerns.

"While the framework established in the GENIUS Act seeks to create that regulatory perimeter and spur innovation, stablecoins continue to risk disintermediating core bank activity like deposit taking and lending, which could undermine the fundamental role banks play in making loans to consumers and businesses," the statement said.

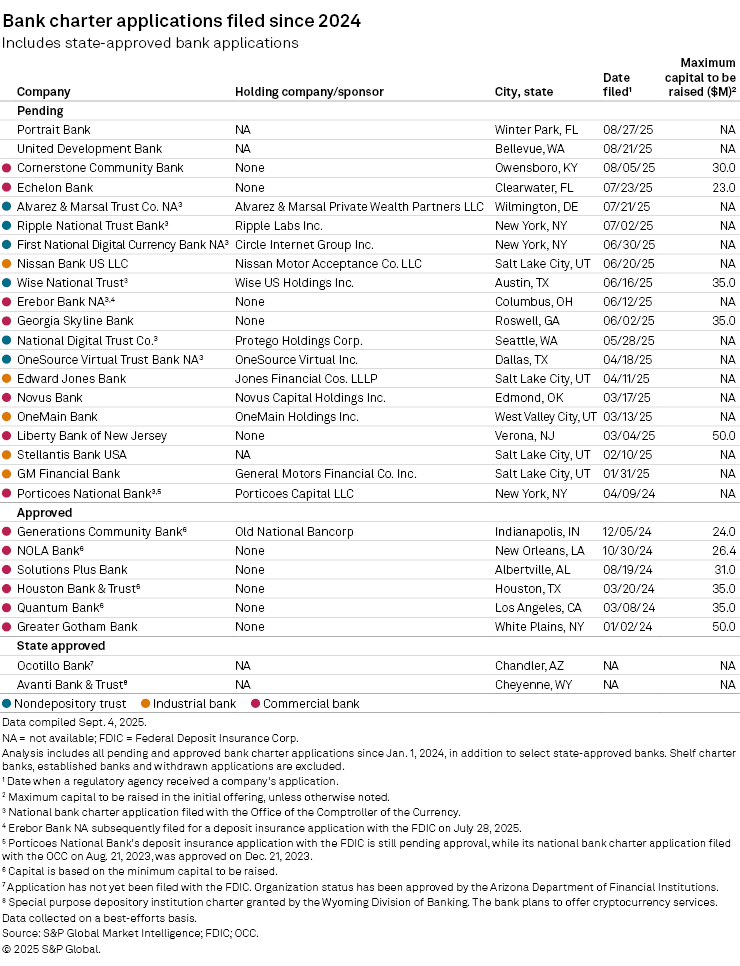

Other charter application activity

The friendlier regulatory environment has also led to increasing applications from ILC hopefuls, with

The uptick comes among public encouragement from FDIC acting Chairman Travis Hill in April and a subsequent request for information from the agency in July seeking to simplify the application process for ILCs.

The road to obtaining an ILC charter has been long and winding since 2006, with only three companies securing approval in nearly two decades while most others withdrew their applications, sometimes several times.

FDIC's Hill also tried to encourage more traditional community bank charter applications during his April speech, as de novo activity has remained subdued since the Great Recession. So far through Sept. 4, there have been nine

The agency is currently exploring "adjusted standards" for traditional community bank applicants, including the up-front capital needed to launch a new bank, Hill said.

Right now, traditional de novo activity remains constrained mostly due to the sheer upfront capital required by regulators, Bisanz said. The cash needed to open a community bank is "a huge overheard cost," he said.