12 Sep, 2025

Lithium price spike may return as experts warn about supply pipeline fragility

| The Rugao lithium hydroxide facility in China, which Rio Tinto acquired with its takeover of Arcadium Lithium in March. |

Another lithium price spike could occur in the coming decade as supply will be challenged to meet future demand due to quality and technology issues, experts have warned.

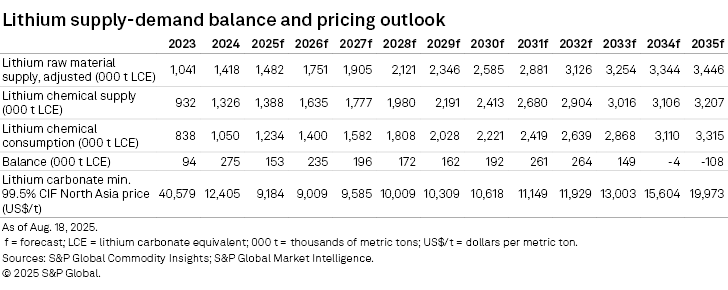

After last year's oversupply of 275,000 metric tons of lithium carbonate equivalent, the next peak is expected in 2032 with a balance of 264,000 metric tons, before flipping to a deficit of 4,000 metric tons in 2034, according to an Aug. 20 note from S&P Global Commodity Insights' Metals and Mining Research team. For 2035, the shortage is forecast at 108,000 metric tons.

Accordingly, the Metals and Mining Research team forecasts the lithium carbonate CIF North Asia price to rise from US$12,405 per metric ton last year to US$15,604/t in 2034 and US$19,973/t in 2035. Lithium chemical demand is expected to rise from 1.1 million metric tons in 2024 to 3.3 MMt in 2035.

Platts, part of S&P Global Commodity Insights, assessed the lithium hydroxide CIF North Asia price at above US$84,000/t in 2022, soaring amid supply deficits due to growing electric vehicle demand. There are signs that supply could again struggle to keep up.

"Brines, hard rock and soft rock projects are anticipated to encounter significant challenges in meeting upcoming demand," Mary Nyah Alcantara and Shunyu Yao, analysts at Commodity Insights, said in a Sept. 11 joint email interview.

Unless both brine and hard rock lithium projects overcome these issues to be developed in a timely manner, "we'll get that spike again because demand will grow rapidly, soak through the surplus capacity fairly quickly and then all of a sudden you end up in a world of undersupply," Ryan Hair, COO of Australia's newest lithium producer Liontown Resources Ltd., told a Sept. 3 panel at the Australasian Institute of Mining and Metallurgy conference in Perth, Australia.

Most of the recently discovered hard rock or spodumene deposits are much smaller with lower quality "relative to what's in production today," Hair said. The highly concentrated nature of existing lithium production means the next phase of growth will inevitably have to come from these lower-quality deposits, or from jurisdictions that are challenged in various ways, according to Hair.

Economic challenges

"Hard rock projects, particularly those in Canada and the US, have higher costs, making them vulnerable to the current low market prices, which could potentially lead to delays," Alcantara and Yao said in the email.

An example is the Nemaska hard rock project in Quebec, which Rio Tinto Group obtained in its US$6.7 billion acquisition of Arcadium Lithium PLC that closed in March.

"According to the Mine Economics cost curve, [Nemaska] is expected to have one of the highest all-in sustaining costs by 2029, a year after our projected start of it," the Commodity Insights analysts said. "Additionally, hard rock projects are grappling with the challenge of securing sufficient refining capacity that offers competitive conversion costs from concentrate to chemical."

The analysts also noted that IGO Ltd.'s second-quarter activities report revealed a conversion cost of A$17,215/t for its Kwinana lithium hydroxide refinery in Western Australia, excluding the purchase of spodumene raw materials, while the Sept. 10 Platts-assessed lithium hydroxide CIF North Asia price was only US$9,800/t.

Spodumene versus brine for lithium production

On a 100% basis, lithium supply from spodumene has grown from 40% of the global total to 60% over the past decade. Though brine output expanded over that period, hard rock has expanded "that much quicker," Leigh Slomp, general manager of technical services at Rio Tinto, told the panel at the Australasian Institute of Mining and Metallurgy conference.

Some saw Rio Tinto's Arcadium acquisition as "an indication of the future dominance of brines in the lithium supply chain," but others wondered if it was "sounding a death for the spodumene producers," Slomp said.

Up to 25 different direct lithium extraction (DLE) technologies based on adsorption, ion exchange, solvent exchange and electrochemical extraction promise to "make the ability to produce [lithium] cheaper and faster" for brine projects, Charlie McGill, CEO of ElectraLith Pty Ltd., told the panel.

However, McGill warned that "there's a lot of work that needs to be done across the board," as most DLE technologies are only in their first five to 10 years of development.

On Sept. 11, McGill confirmed to Platts that ElectraLith's electrochemical technology will be trialed in Argentina in 2026 by shareholder Rio Tinto.

Though brine has historically been cheaper than hard rock in producing lithium carbonate, not every brine resource is cheaper than every spodumene resource to develop, Seth Goldstein, senior equity analyst for resources and chair of the electric vehicle committee at Morningstar Research Services LLC, said in an email interview.

"In general, brine from high-quality resources in Chile or Argentina has been lower cost than many spodumene operations and more profitable. This is why these projects will likely be among the first to be developed once prices rise and will likely see faster growth over the next several years," Goldstein said.

Australia is also disadvantaged in developing a downstream sector due to gas, electricity and labor costs and the fact that China develops lithium processing plants up to three times quicker, Hair said.