24 Nov, 2025

US solar developers add 6 GW in Q3; 271 GW planned through 2030

By Kirsten Errick and Gaurang Dholakia

US solar power plant development remained robust in the third quarter of 2025, marked by rising capacity additions and an expanding pipeline of near- to medium-term projects.

Developers added roughly 6 GW in the third quarter, bringing cumulative installed large-scale solar capacity to 148.8 GW, according to S&P Global Market Intelligence data. Third-quarter capacity additions were up 6.8% from the second quarter and were 13.9% higher year over year.

The acceleration came as clarity emerged over shortened federal tax credit timelines. President Donald Trump's sweeping budget bill, enacted in July, accelerated a phaseout of tax credits for solar and wind by several years, while adding new restrictions on equipment linked to foreign entities of concern (FEOC).

"These were not wise policy changes," Pivot Energy Inc. CEO Tom Hunt told Platts, part of S&P Global Energy. "We need more electricity, not less."

Earlier incentive sunsets, however, are quickening the pace of some development, according to market participants.

"The irony of what's happening from a federal policy level is that the next two years, in 2026 and 2027, you'll see more solar come online in each year than ever has come online for any previous years," REC Solar CEO Robb Jetty told Platts. "That train has kind of already left the station."

Under safe harbor rules issued in August, solar projects that start construction by July 4, 2026, have until the end of 2030 to qualify for tax credits. If projects are not under construction by that time, developers must have them online by Dec. 31, 2027.

As of Nov. 13, developers had completed 20.6 GW so far in 2025, with another 38.3 GW under construction and 9.2 GW in advanced development, Market Intelligence data shows. Over 13 GW of the photovoltaic power plant capacity under construction is scheduled for completion this year.

Through 2030, developers plan to add more than 271 GW of new PV capacity, the majority of which remains in early-stage development. That volume would keep the US solar industry on pace to remain the leading source of new capacity for years to come.

But projects in the pipeline must overcome challenges beyond expiring tax credits and the new FEOC rules, which take effect in 2026.

"The two biggest hurdles are the interconnection and the local permitting, which I would call zoning," Doral Renewables LLC President and CEO Nick Cohen told Platts.

Interconnection is a challenge because "you might get a bad result, which it's just a matter of fact and science," Cohen said, pointing to grid limitations.

Permitting delays, meanwhile, can derail projects.

"Time kills deals," Cohen said. "The longer you wait, the more time opposition has and a lot of times it's out-of-town opposition ... and because you're waiting for the interconnection, you can't move forward."

However, Cohen added that 12 states have passed preemption laws whereby the state takes over the local permitting.

"That's the single most profound thing that can happen to increase the supply of projects," Cohen said.

Another challenge is around labor shortages.

"There's massive shortages in electricians and skilled labor to actually erect steel and do all of the work that we need to build these kinds of projects," said REC Solar's Jetty.

Construction costs and power purchase agreement prices are rising with data center-driven demand, according to developers.

"The market is seeing dramatic increases in prices in both capacity and energy in certain areas across the country," added Hunt of Pivot Energy. "And I think that reflects the shortage of supply ... those are a lot of the areas where the first real wave of data centers are being built."

Despite such challenges, the development of large solar farms is flourishing, as reflected in projects completed in the third quarter.

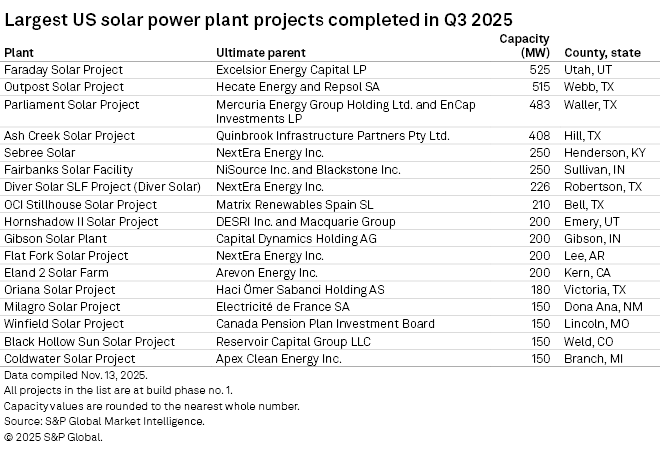

The 525-MW Faraday Solar Project in Utah, owned by Excelsior Energy Capital LP, was the biggest PV project completed in the third quarter, according to Market Intelligence data. It is backed by a 20-year power purchase agreement with PacifiCorp. under a Rocky Mountain Power green energy tariff. Meta Platforms Inc. is purchasing all of the energy and environmental attributes of the project.

Five of the largest 10 projects completed in the third quarter are in Texas.

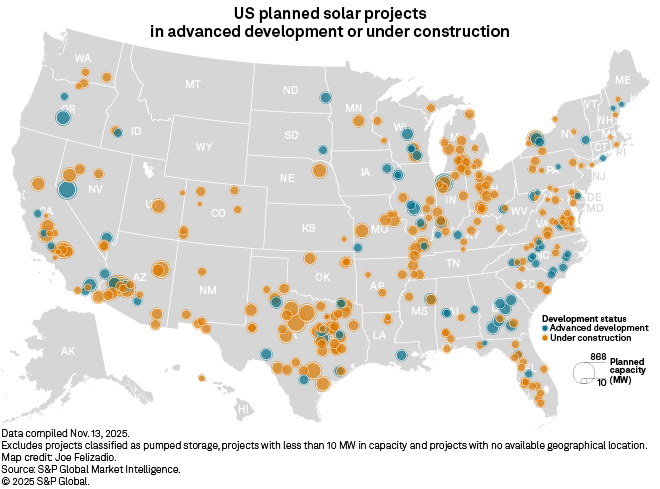

Texas also has the largest pipeline of near-term projects, with nearly 12 GW under construction or in advanced development at 59 projects. Arizona has the second-largest pipeline of projects under construction or in advanced development, with more than 5.4 GW at 17 projects, followed by California with 3.7 GW over 22 projects.

Other states with large near-term pipelines include Indiana, with 2.2 GW across 11 projects, and Michigan, with just under 2.2 GW at 15 projects.

"The demand is everywhere," Cohen said.

Market Intelligence considers a project as announced when it has a listing in an interconnection queue with an accompanying public announcement or permitting action. A project is considered in early development after permitting begins. For a project to be considered advanced development, it must meet two out of five criteria: financing is in place, power purchase agreements are signed, equipment is secured, required permits are approved or a contractor has signed on to the project. A project is under construction when building activity begins; site preparation does not qualify a project for this status.