10 Nov, 2025

Shifting risks push major central banks in different directions

By Nick Lazzaro

European Central Bank President Christine Lagarde speaks during a press conference on eurozone monetary policy in Florence on Oct. 30, 2025. The ECB's interest rate easing cycle has likely come to an end this year while the US Federal Reserve and the Bank of England navigate a more uncertain policy path in the coming months. Source: Tiziana Fabi/AFP via Getty Images. |

Economic growth and labor market trends are increasingly driving divergent monetary policy paths for major central banks as inflation moderates in many economies.

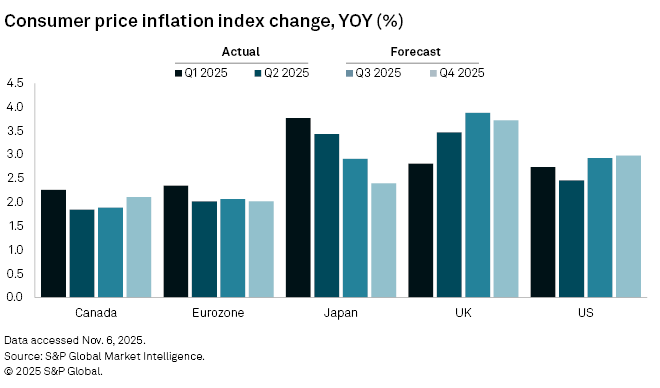

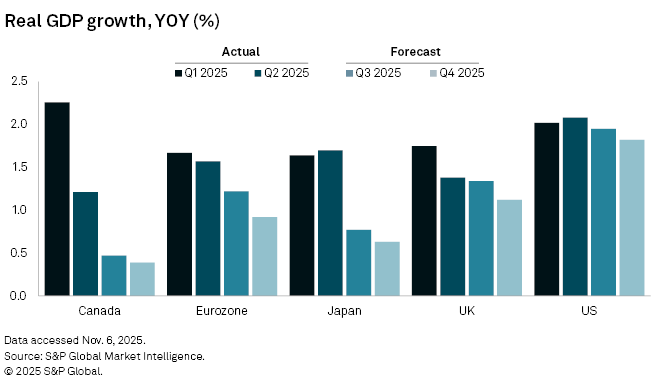

Year-over-year consumer price inflation in the fourth quarter is forecast to cool in the eurozone, Japan and the UK while rising moderately in the US and Canada, according to economic projection data from S&P Global Market Intelligence. Meanwhile, fourth-quarter unemployment rates are expected to creep up in the US and the UK but remain stable in the other G7 economies, and economic growth is projected to slow across the cohort.

The evolving economic landscape has shifted the monetary policy pathways of the G7 central banks, with the European Central Bank and Bank of Canada signaling likely ends to their rate-cutting cycles after their October meetings. However, with December meetings nearing, the outlook remains cloudier for the US Federal Reserve and the Bank of England as they consider the timing of their next interest rate cut, while the Bank of Japan monitors conditions for a potential rate hike.

"The ECB has strongly signaled a steady hold at its 2% rate for the foreseeable future, and after the [Bank of Canada's] latest cut to 2.25%, many analysts expect it to pause there for an extended period," Kevin Philip, partner at Bel Air Investment Advisors, told Market Intelligence. "In contrast, the Bank of Japan's trajectory is highly uncertain as it could surprise markets with a rate hike or policy tweak by year-end, given persistent inflation pressures and past sudden moves, or remain on hold if conditions aren't deemed ripe."

Bank of England, US Fed both still lean toward cuts

The Bank of England (BoE) and the Fed remain in monetary policy easing cycles, though market expectations continue to fluctuate regarding the timing of their next moves.

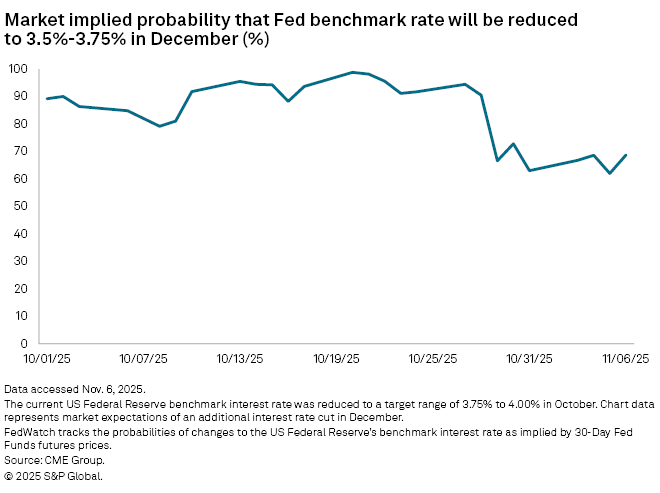

The Fed reduced its benchmark rate Oct. 29 by 25 basis points to a range of 3.75% to 4%. Fed Chair Jerome Powell said during a press conference that an additional cut in December was "not a forgone conclusion" amid differing views among the bank's policy-setting committee.

"The biggest surprise to the market was that the Fed guided to a somewhat 50/50 chance for the December meeting whether they are going to cut or not," Robert Timper, chief fixed income strategist at BCA Research, said in an interview. "We had flagged that the market's pricing for a cut in December was getting a bit ahead of itself because even before October's meeting, we knew that the Fed committee was pretty split."

Markets were pricing in a nearly 69% chance as of Nov. 6 that the Fed would issue a 25-basis-point cut to its benchmark rate in December, according to CME Fedwatch data.

In contrast to the Fed, the BoE held its rate steady at 4% during its November meeting in a 5-4 vote. In a statement released after the meeting Nov. 6, the BoE said the decision reflected its view that inflation had peaked, and underlying disinflation trends were being "underpinned by subdued economic growth and building slack in the labor market."

"For the BoE, we do think that there is a good chance they cut in December," Timper said. "In November, if data confirms the recent weakness in the inflation print and the employment print also confirms the labor market weakness, then the BoE is likely to resume cutting in December."

Over the next 12 months, the Fed and the BoE could ultimately cut their respective interest rates by the same amount, according to Timper.

ECB's easing pause may be temporary

After the ECB's decision to hold its key interest rates steady in October, President Christine Lagarde said the eurozone's monetary policy was "in a good place" with modest economic growth and inflation near the medium-term target rate. Market analysts expect the bank to keep rates on hold through 2026, though the eurozone's hazy economic outlook may pressure this expectation.

"We find it somewhat unrealistic to expect the ECB to remain on hold for at least another 12 months," Julien Lafargue, chief market strategist at Barclays Private Bank, told Market Intelligence. "While this may be the outcome ultimately, we suspect market expectations will shift, possibly quite meaningfully, over this period."

Lagarde's view on Europe's economic growth outlook may be viewed as overly optimistic and dependent on expected tailwinds from Germany's ongoing fiscal stimulus, according to Capital Economics Chief Europe Economist Andrew Kenningham.

"We're a bit more pessimistic about prospects for the economy in general, partly because we think there's an overoptimism among policymakers and a lot of people in the markets around how much impact the German fiscal stimulus will have," Kenningham said during an Oct. 30 webinar. "It will be a positive, but it will probably be quite small, and they'll probably be quite slow implementing it."

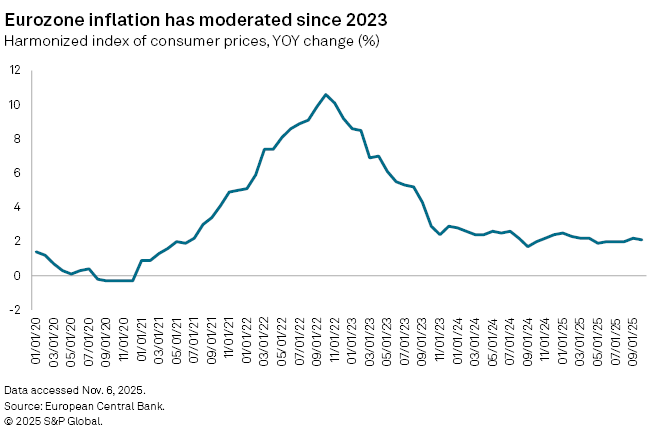

The ECB could also be pushed to revisit rate cuts in 2026 if the eurozone's moderating inflation rate dips to unsustainable levels. The region's annual harmonized index of consumer prices inflation rate has mostly been rangebound between 2% and 3% since 2023.

"The balance of views on the ECB Governing Council is most likely to shift towards cutting rates a bit further to ensure against the risk of getting stuck again in a low inflation world," Kenningham said. "It wouldn't be as serious as we had in the 2010s, but there is a tendency in the eurozone for things to head in that direction, so we think they'd want to move against that."