S&P Global — 5 Apr, 2023

Daily Update: April 5, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Global Economic Resilience, For Now

The much-anticipated first-quarter recession failed to arrive. While the global banking sector has experienced some turbulence related to rising interest rates, the economic impact has been limited thus far. This unexpected resilience of the global economy may be good news with an expiration date, however. Economists continue to warn of downside risks related to persistent inflation, rising rates, lower spending and lower lending. Macroeconomic indicators continue to flash red, but a potential recession is taking its time to arrive.

Paul Gruenwald, global chief economist at S&P Global Ratings, suggests in his latest outlook that the strong policy response to finance sector turbulence in the U.S. and Europe seems to have calmed the markets. But inflation continues to bedevil the U.S., European and U.K. economies, and central banks have not backed away from their inflation targets. While we can anticipate that the major central banks will move cautiously in the hope of a soft landing, the downside risks remain significant, with tepid growth projected for the year.

“While our baseline forecast has not changed much since our previous round, the risks around the baseline have shifted materially to the downside,” Gruenwald wrote. “This shift reflects the emergence of financial fragility over the past few weeks and its potential impact on our baseline.”

The U.S. economic outlook continues to be caught between overheated labor markets and a Federal Reserve committed to bringing inflation back toward a 2.0% target, according to S&P Global Ratings. Despite slightly softer job numbers in recent weeks, February wage gains stood at 4.6% year over year — an indication that job seekers remain very much in demand. The upheaval in the banking sector increases the likelihood of a hard landing, with a mild recession projected for this year.

Still, resilience in the U.S. economy persists alongside its less-desirable twin, inflation. S&P Global Market Intelligence shows U.S. output returning to growth in March. Producers have worked to reduce their backlogs, and supply chain improvements are driving down the inflation that was hitting raw materials. The service sector remains overheated, with wage growth a strong driver of inflation. But the resilience of the economy will encourage an aggressive monetary policy from the Federal Reserve.

In Europe, economic resilience has surprised as well. Positive data on real GDP and survey data in the eurozone and EU indicate unexpected strength in the economy. However, S&P Global Ratings revised down projected eurozone GDP growth for 2024 to 1.0% from 1.4% in their previous outlook.

China, as in previous outlooks, appears to be on track for its relatively modest GDP growth target of about 5%. Strength in China will have some positive impacts on Asia-Pacific economies, while other emerging markets will suffer from slower growth this year due to conditions in the U.S. and eurozone.

Overall, unexpected resilience is the order of the day for the global economy. When, and if, recession finally hits, it will be arriving much later than expected.

Today is Wednesday, April 5, 2023, and here is today’s essential intelligence.

Written by Nathan Hunt.

Economy

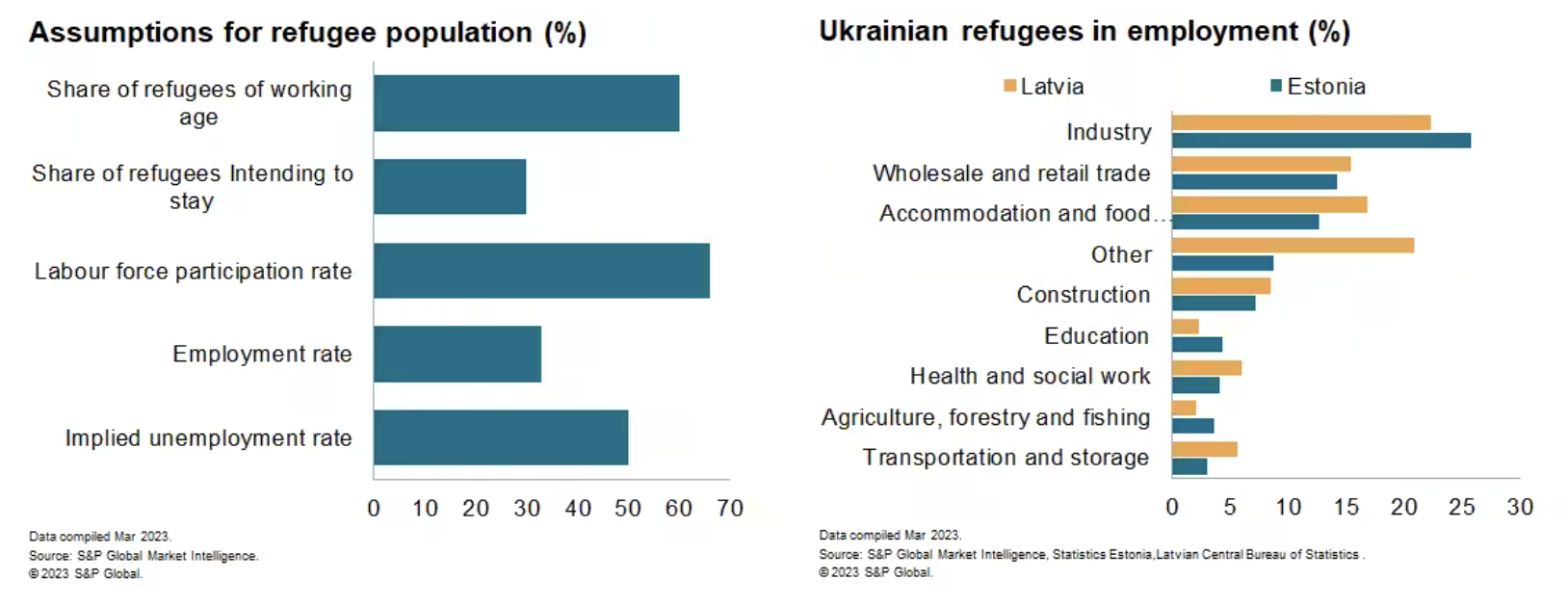

Baltic States Grapple With High Unemployment Rates For Ukrainian Refugees

The number of refugees being hosted by the Baltics has added almost 3% to the local population and, accounting for reported intentions to stay, nearly 1% to the working-age cohort. Addressing high refugee unemployment will be the main challenge in 2023, with no low-hanging fruit. The number of Ukrainian refugees across Europe, excluding Russia and Belarus, had stood at 5.2 million as of March 14, 2023, of which around 4.9 million are currently registered for the European Union's temporary protection scheme or similar national arrangements, according to figures from UN High Commissioner for Refugees (UNHCR). Some refugees could be double counted if they registered in one country before moving onwards to another.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

European Banks' Loan-To-Deposit Ratios Held Steady Ahead Of Credit Suisse Demise

Credit Suisse Group AG was the sole outlier in otherwise stable loan-to-deposit ratios at European banks as of the end of 2022. The Swiss bank's loan-to-deposit ratio jumped to 113.26% as of Dec. 31, 2022, from 74.25% a year prior, S&P Global Market Intelligence data shows. The bank experienced major deposit outflows in the fourth quarter of 2022, which continued into early 2023 and ultimately led to its forced merger with UBS Group AG.

—Read the article from S&P Global Market Intelligence

Access more insights on capital markets >

Global Trade

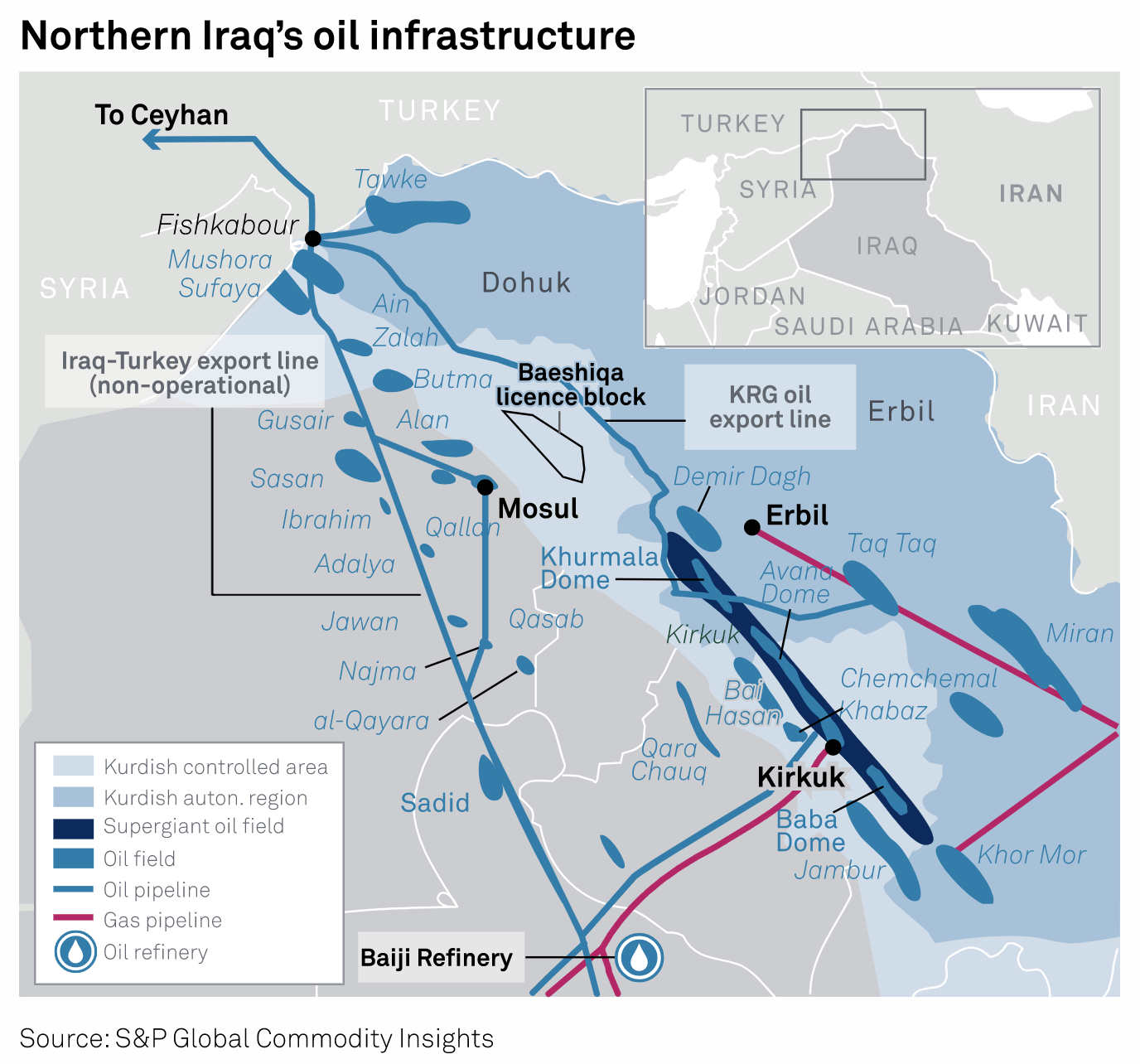

Iraq's Kurdistan Region To Resume Oil Exports April 4 Amid Signing Of Agreement With Baghdad

Iraq's semi-autonomous Kurdistan region will resume crude exports via the Turkish terminal of Ceyhan as soon as April 4 after the prime ministers in Baghdad and Erbil signed a temporary agreement that will allow the flow of over 450,000 b/d back into the Mediterranean basin. The technical sides from Baghdad and Erbil should start "immediately" implementing the temporary agreement, Prime Minister Mohammad al-Sudani said April 4 in a joint press conference with his Kurdish counterpart Masrour Barzani in Baghdad.

—Read the article from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

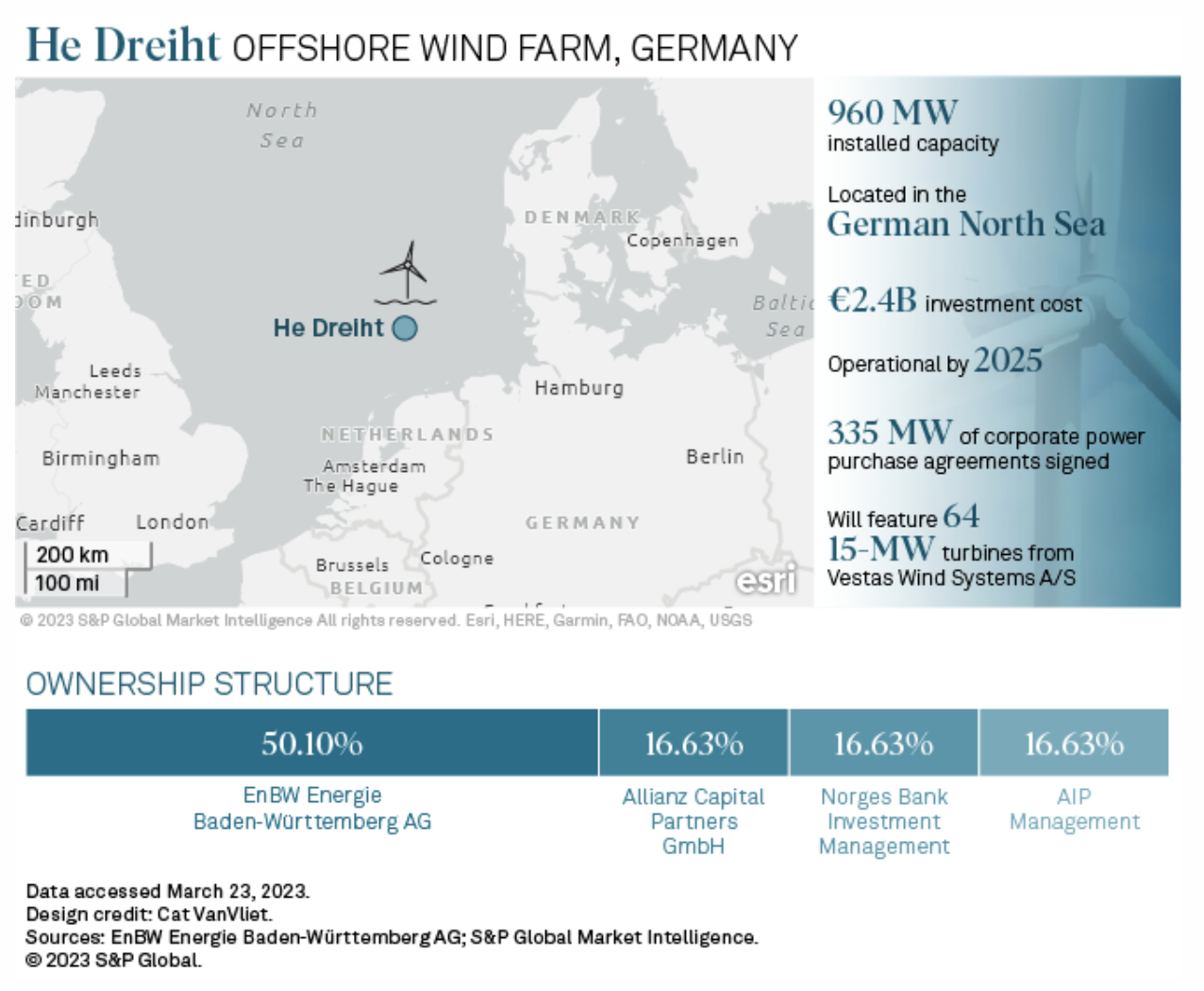

Germany's He Dreiht Forges Blueprint For Subsidy-Free Offshore Wind

With a positive final investment decision in hand, utility EnBW Energie Baden-Württemberg AG's He Dreiht offshore wind farm in Germany illustrates the industry's transformational shift from government support to a complex blend of corporate offtakers and market exposure. Six years have passed since EnBW secured the rights to the 960-MW offshore wind farm in a government auction that defied expectations at the time but has since become the market norm.

—Read the article from S&P Global Market Intelligence

Access more insights on sustainability >

Energy & Commodities

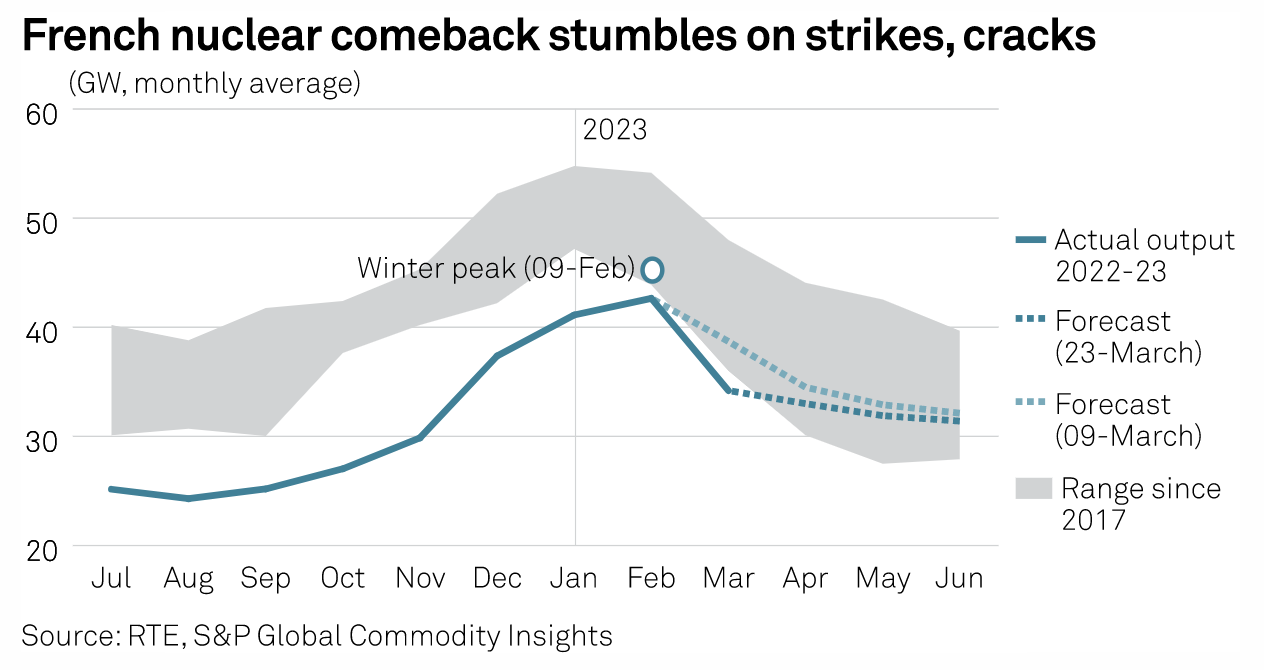

French Nuclear Output Extends Series Of Record-Lows Into March As Strikes Continue

French nuclear registered another long-term low in March as average output fell 4.7% on the year to 34.4 GW, system data showed, due to the effects of strikes in the country. Analysts at S&P Global Commodity Insight had forecast March to average 38.7 GW, already down sharply from an end-2022 forecast as France's nuclear comeback started to stumble in March amid the strikes.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

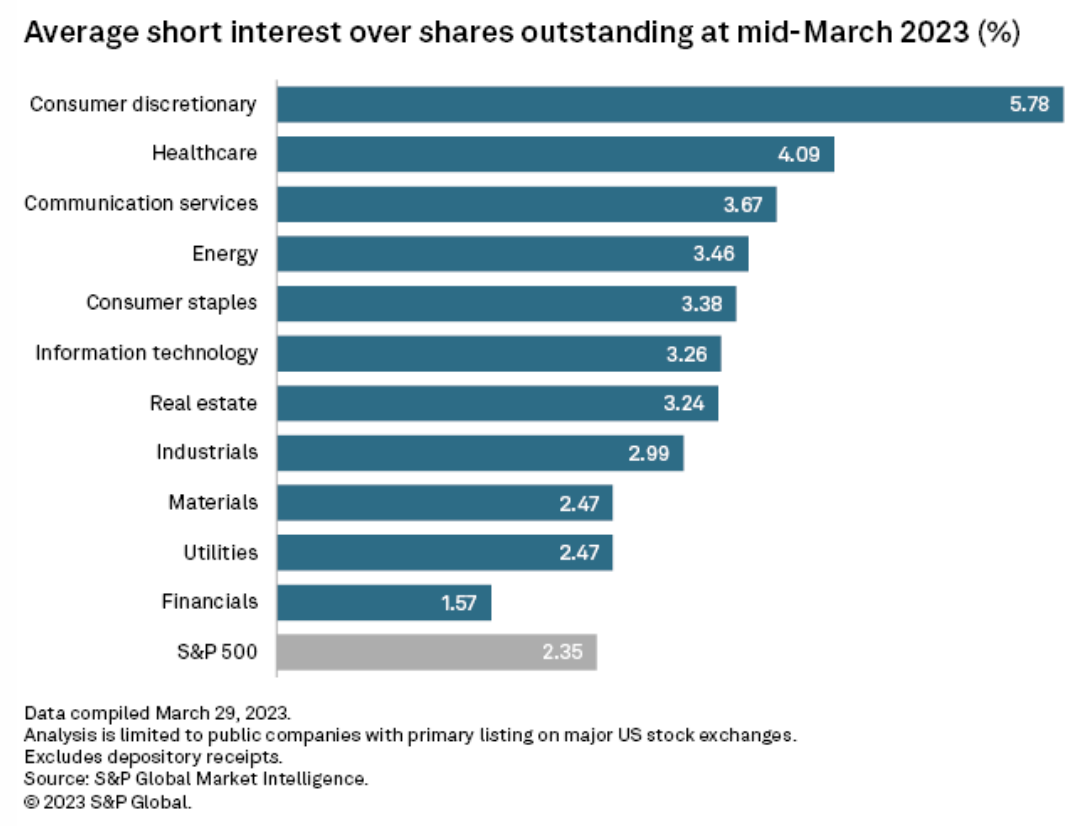

Short Sellers Cut Bets Against Communication Services Stocks

Short sellers further pared back their bets against communication services stocks through the middle of March. Short interest in the communication services sector was at 3.46%, a drop of 17 basis points (bps) from the end of February and down about 214 bps from the most recent peak in July 2022, according to the latest S&P Global Market Intelligence data.

—Read the article from S&P Global Market Intelligence