1 Jul, 2021

Most big European banks expected to hold on to loan loss provisions in Q2

By Vanya Damyanova and Cheska Lozano

After a notable first-quarter drop, loan loss provision levels at Europe's largest banks are expected to continue declining in the second quarter of 2021 and beyond, but lenders will likely hold on to some of their pandemic-related reserves for longer, analysts said.

An uneven economic recovery across European countries, remaining uncertainty about the full impact of COVID-19 after government aid schemes end and worries about regulatory pushback may discourage many banks from releasing provisions.

As bank profitability remains under pressure, the "bright spot" in the second quarter, and 2021 as a whole, will be provisioning, Giles Edwards, senior financial services ratings director at S&P Global Ratings, said in an interview. Lower credit impairment charges and some improvement in fee and commission income, coming from a rebound in economic activity, will be the main drivers for 2021 bank profits, while net interest income remains a drag, the rating agency said in a June 24 review of roughly 60 European banks.

Profitability will remain a weak point for European banks given that COVID-19 will prolong the low interest rate environment, Alain Laurin, associate managing director in the financial institutions group of credit rating agency Moody's, said in an interview. Fee and commission income still accounts for just a small part of the total income of many European banks and this is not something they can change "with the stroke of a pen," Laurin said. Banks will also face increased costs as the need for investments in IT and efficiency improvements has grown amid the pandemic, according to Laurin. "Banks that are serious about their future, have to spend money to invest in digitalization," he said.

Q1 recovery

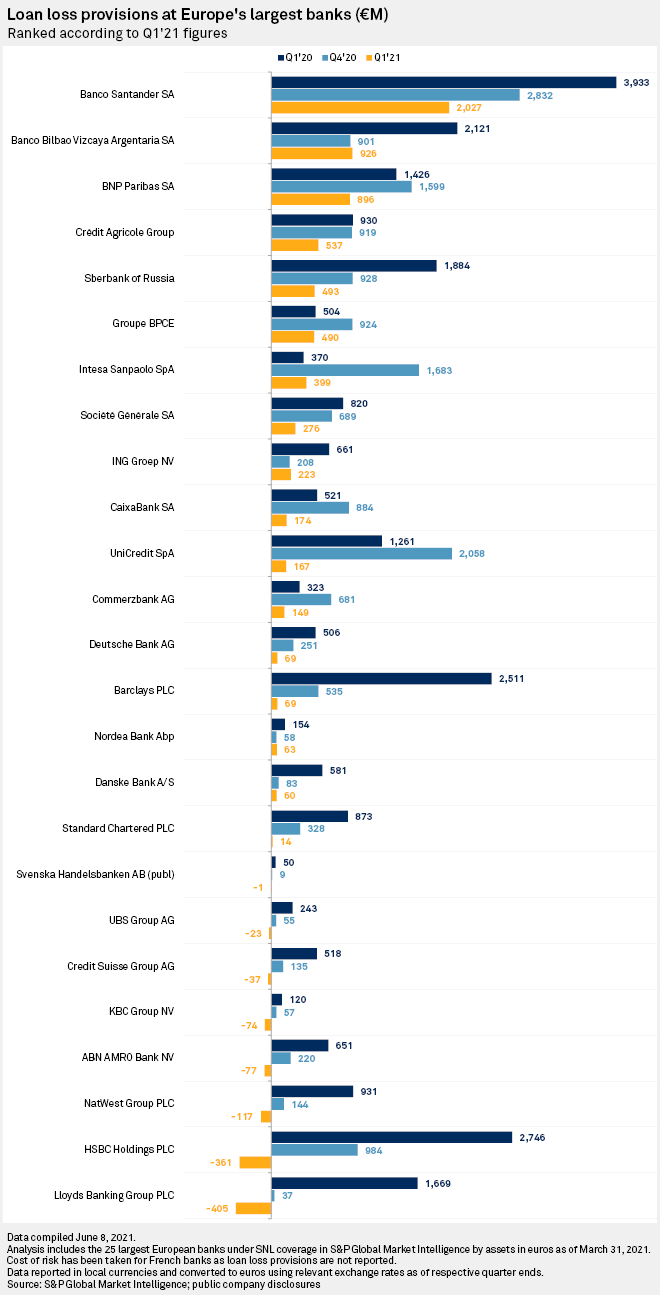

Many European banks provisioned heavily amid the pandemic in 2020 and have seen cost of risk levels decline in the first quarter of 2021, with some even releasing the reserves they had set aside to cushion potential COVID-19-related loan losses. Eight out of the 25 largest banks in Europe released provisions in the first quarter, with U.K.-based Lloyds Banking Group PLC booking the highest release amount of €405 million. All remaining banks in the sample posted loan loss provisions well below the prior-year level.

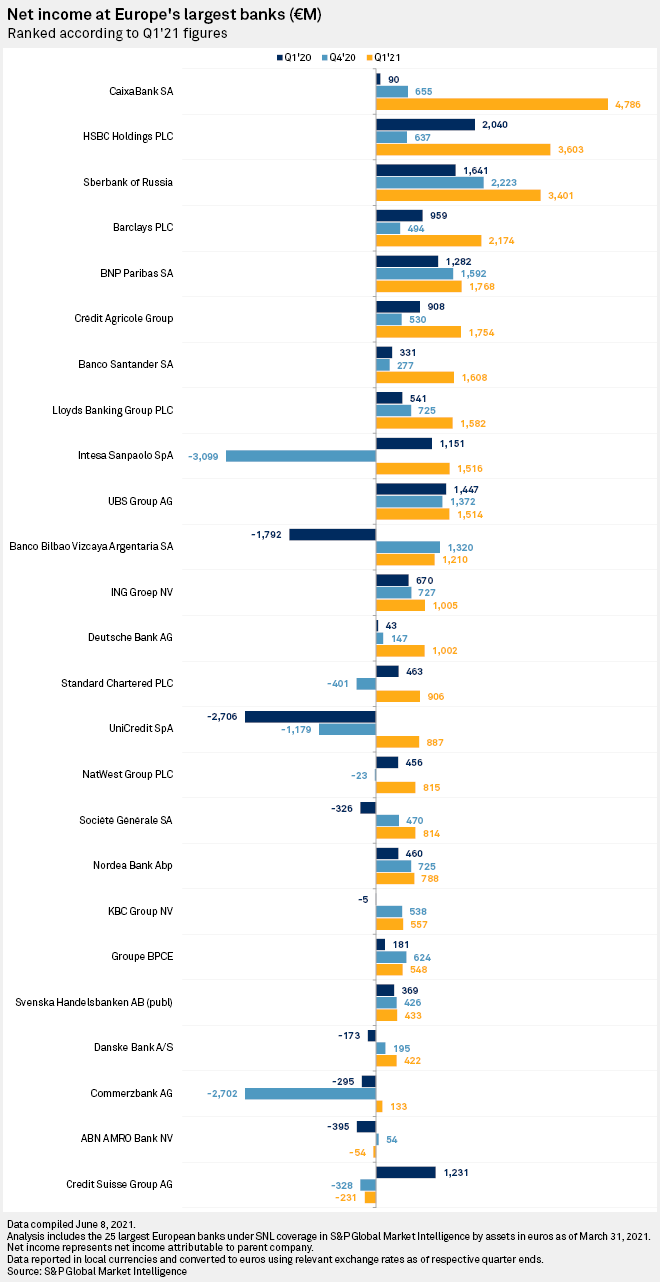

The drop in provisions gave first-quarter net income a boost, with 23 out of the 25 banks in the sample posting year-over-year profit growth. The only two banks to book a loss for the period were Netherlands-based ABN AMRO Bank NV, which had to cover a €480 million anti-money laundering settlement, and Credit Suisse Group AG, which took a CHF4.43 billion hit from the collapse of U.S. hedge fund Archegos.

Sticking with provisions

Although loan loss provision amounts are gradually declining in 2021 and are expected to be lower than in 2020, they will stay elevated compared to pre-pandemic levels, according to Edwards. There will be some releases in the second quarter and later in the year, but S&P Ratings expects most of the top 100 European banks "to still have a meaningful credit loss charge this year," Edwards said. "Management teams will be trying to hang on to their overlays for as long as possible," he said.

Acting out of caution due to the uncertainty about the impact of the pandemic, many banks have applied management overlays, which are extra buffers for expected credit losses, or ECLs, under current international financial reporting standards.

In terms of expected provision releases, banks are likely to remain on the safe side and hold on to their reserves until there is more clarity about the economic recovery, Laurin said. Banks may also be hesitant to release provisions too soon due to expectations that supervisory authorities like the European Central Bank or the Single Supervisory Mechanism, which comprises the ECB and national regulators, would object, Laurin said.

'Transition year'

For now, the forward-looking cost of the pandemic for the banking sector has been factored in and was reflected in the surge of stage 2 provisions in 2020, Laurin said. Under the IFRS 9 accounting standard applied in Europe, assets are classified in three stages of credit risk where stage 1 are performing assets, stage 2 are assets that have experienced a significant increase in credit risk since their initial recognition in the bank's books, and stage 3 are nonperforming assets. Provisioning for stage 2 assets requires banks to set aside ECL reserves for the lifetime of the asset rather than just for the next 12 months, as with stage 1 assets.

This year could be a year of transition in terms of provisioning because the risks have not yet materialized, Laurin said. Depending on the pace of economic recovery and government support withdrawal across regions, these risks could hit banks in 2022 or even later, in 2023, Laurin said.

Additional EU funds that are being made available are bound to support the private sector and eventually the banking system. What this means for provision levels in the second and third quarter of 2021 is that stage 3 provisions will remain rather stable, while stage 2 provisions will decline compared to the prior-year levels, Laurin said.