5 May, 2021

Healthcare M&A activity bounces back in Q1'21 from early-2020 doldrums

The size and volume of pharmaceutical and biotechnology M&A transactions began to rebound in the first quarter of 2021 from a deep valley a year earlier, but the sector has stayed fairly quiet on the megadeal front, according to data compiled by S&P Global Market Intelligence.

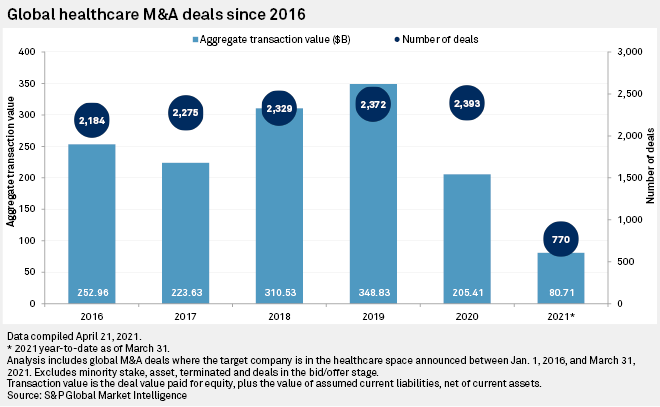

Industry M&A transactions through 2020 swung toward smaller to midsize deals as companies sought to restore product pipelines rather than transform via the larger megadeals that characterized the prior year — a trend that probably reflected the fledgling COVID-19 pandemic at the time.

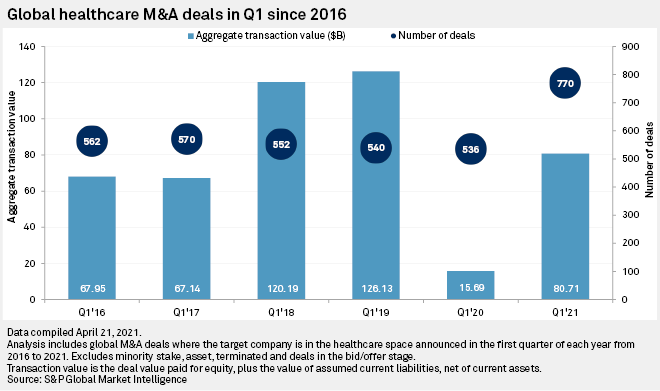

But deal-making rose through the year into the first quarter of 2021 as the light at the end of the COVID-19 tunnel emerged along with vaccine rollouts and a recovering worldwide economy. The aggregate transaction value for healthcare M&A was five times higher in the first quarter of 2021 compared with the year-ago period.

"It looked to us that perhaps due to COVID, there was a delay in new M&A announcements," Moody's Senior Vice President and Pharmaceutical Analyst Michael Levesque said in an interview. "And then towards the end of [2020] or the second half of the year, there really was a flurry of activity."

Levesque said the drawback in early 2020 was more likely due to volatility in the general capital markets than in any weakness to the biopharma industry, which came through the pandemic relatively unscathed.

"It was just more that the capital markets were so in flux as opposed to any company feeling that its own business had some vulnerabilities to get through," Levesque said. "Because pharma was among the least affected sectors."

The capacity for M&A among the sector's top U.S. players remains high from a Moody's credit rating standpoint, Levesque said. Companies with particularly high capacity for deal-making — using a ratio of debt to EBITDA, as well as cash on hand — were Merck & Co. Inc., Regeneron Pharmaceuticals Inc. and Amgen Inc., according to an April quarterly report from Moody's.

Those on the lower end of that credit capacity range were AbbVie Inc. and Gilead Sciences Inc. after having acquired Allergan and Immunomedics, respectively, in the previous year.

A similar trend has emerged among European pharmaceuticals, as noted by Novartis AG CEO Vas Narasimhan on the company's first-quarter 2021 earnings call.

"We have shifted to a more opportunistic approach on M&A," Narasimhan said. "We continue to look at small deals, where we've done a number in the research area over the course of last year, as well as licensing deals, but other than that, we will be opportunistic when we see something but nothing else planned at this point in time."

The appetite for smaller, research-based pipeline acquisitions has remained high and is likely to continue as companies seek to bolster their portfolios, Levesque said.

"It's just for many years been a key part of the strategy to enhance growth prospects and expand into new areas and bring in new pipeline compounds," Levesque said. "So we would say the appetite is rather high across the sector."

In 2021, the expectation is to see a continuation of late-stage pipeline deals for products that have just reached the market and still have expanding uses and potential new indications, Levesque said.

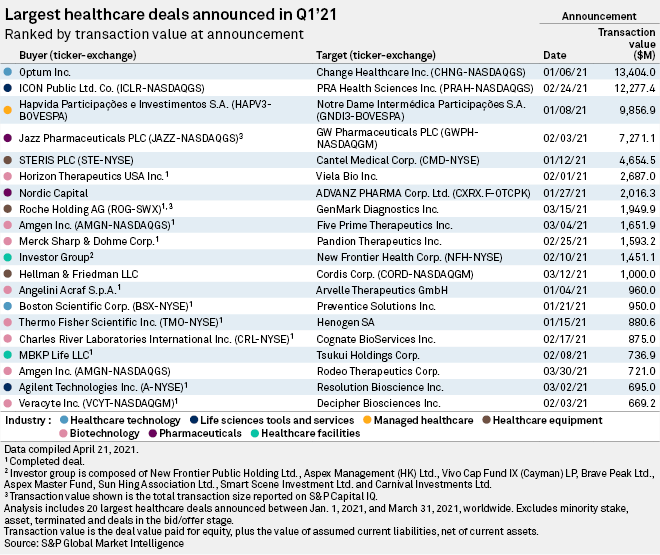

The healthcare technology and life sciences tools and services sectors saw the biggest announced deals of the quarter and the only two that rose above $10 billion in total value: Optum Inc.'s purchase of Change Healthcare Inc. for $13.4 billion and ICON PLC's acquisition of PRA Health Sciences Inc. for $12.28 billion.

Levesque also noted that M&A activity is not limited to just the large-cap space, as indicated by another one of the largest deals of the first quarter, when Jazz Pharmaceuticals PLC announced in February it would acquire GW Pharmaceuticals PLC with a total value of $7.27 billion.

SPAC activity fills a void

Another emerging trend is the special purpose acquisition company, or SPAC, which has become more common as a means to bring companies public and could augment overall M&A activity in 2021.

"You're going to see some M&A — whether you call it M&A or not — coming out of the SPAC phenomena," said Sophie McGrath, technology & life sciences partner at law firm Goodwin Procter. "You've got a huge number of these listed vehicles, a lot of them created by specialist life sciences and healthcare investors, which have a limited period in which to find a target, and so I think you will see some M&A activity driven by that."

Increased scrutiny from regulatory authorities such as the U.S. Federal Trade Commission has some large pharmaceutical companies rethinking their dependence on M&A to drive business forward. Roche Holding AG CEO Severin Schwan said on a first-quarter earnings call that the company's experience acquiring gene therapy specialist Spark Therapeutics resulted in a more hesitant approach down the road.

"There is increased scrutiny, and it's very much coming from the tech industry, but it has spilled over to pharma and biotech now," Schwan said, pointing to regulatory obstacles that made the Spark acquisition more troublesome than expected. "We watch that very closely; so does the whole industry, and that will also have an impact, depending on what the outcome is, on how we look at potential acquisitions in the future."