22 Feb, 2021

Deep Dive: US national debt hits 100% of GDP. Should the credit markets care?

By Jack Hersch

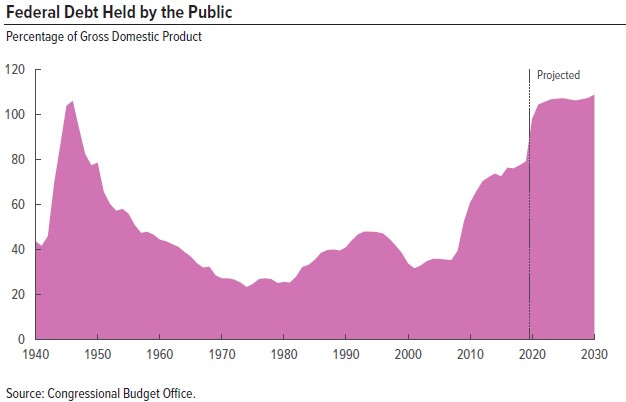

The nonpartisan Congressional Budget Office recently released its publication, The Budget and Economic Outlook: 2021 to 2031, highlighting that during 2020 the U.S. national debt held by the public rose to 100% of GDP for the first time since the end of the Second World War. Will such high levels of U.S. debt, so worrisome in the early 2010s, when markets focused on the greater-than-100%-of-GDP Southern European sovereign borrowings, be a concern to U.S. high grade and high yield bond portfolio managers today?

|

High yield and investment grade market players have not, so far, exhibited any fear of the national debt. In fact, their only fear last year seemed to be that of missing out, as bond issuance in 2020 broke records across the risk spectrum.

|

But 10 years ago financial markets zeroed in on the sovereign debt burdens of Southern European countries. As Greece, in particular, teetered on the edge of default, investors reacted by pushing down equity and debt markets, including sovereign paper, and driving the euro lower against the U.S. dollar.

Then Mario Draghi took over the European Central Bank in November of 2011. He promptly cut interest rates, and the next summer famously said he would do "whatever it takes to preserve the euro. And believe me it will be enough."

Markets believed him, eventually recovering through International Monetary Fund cash, Eurozone financial support vehicles and austerity measures, along with interest rate moves and table-pounding by Draghi.

But nations, to this day, have continued to maintain high debt-to-GDP levels. In the U.S. there is more than $21 trillion of public debt. Note that the $21 trillion figure is the "debt held by the public," which does not include intragovernmental debt held by U.S. government trust funds, such as Social Security, which totals roughly $6 trillion.

Nothing to see here?

Despite the market's clear concern about high sovereign debt-to-GDP levels in 2011, the U.S.'s ascendency to the 100% Club has some observers wondering if investors should now focus their attention on the potential ramifications of such lofty debt levels.

"One hundred percent is not what we thought it was," answers Joe LaVorgna, former white house chief economist and former chief economist Americas, at asset manager Natixis. "Markets don't care, because rates are so low, and even lower in Europe."

To LaVorgna's point, according to the CBO, from 2010 to 2020 the U.S. national public debt more than doubled — from $9 trillion to $21 trillion. Yet over the same period the gross interest cost on that debt grew only 26%, from $414 billion to $523 billion. The CBO attributes the lag in interest cost to "historically low interest rates."

Viewing interest costs through the lens of U.S. GDP confirms the current low-rate environment. Through the 1970s, net interest on the national debt equaled no more than 1.5% of GDP. By 1985 that cost had ballooned to more than 3% of GDP. But in 2020 net interest was back to 1.6%. On a relative basis, the cost of the national debt today is half its cost 10 years ago, and no worse than nearly half a century ago.

According to LaVorgna, part of what is keeping interest costs at 1970s levels is the Federal Reserve's bond buying under Quantitative Easing. Fed purchases, both in Treasury open-market operations as well as through Treasury, mortgage and other non-government bond purchases, are raising the scarcity value of debt instruments, thereby keeping their interest rates down.

Pete Cecchini, founder and chief strategist at AlphaOmega Advisors LLC and former global chief strategist at Cantor Fitzgerald, concurs. Expanding on the explanation, he says that QE is a form of "duration transformation."

Cecchini says that Fed buying under QE creates a reserve liability on its balance sheet, while the purchase of Treasury bonds creates an offsetting Fed balance sheet asset. The reserves, residing at member banks, mean the Fed has effectively replaced a longer-dated bond with the shortest-dated risk-free asset available — cash. This process creates demand for Treasuries and pushes down yields.

Cecchini believes the high U.S. government debt load is not necessarily harmful. The strategist notes that while there are risks to QE, the Fed can continue buying all the bonds the government needs to fund its debt and deficits; reserve creation need not end.

In fact, according to Cecchini, it can't end. He says QE's success to date in holding down yields has eliminated the Fed's maneuvering room. "QE is here to stay," he says emphatically, pointing out that the last time the Fed backed away and allowed longer yields to rise led to late-2018's equity market decline. He explains that the Fed needs to continue QE in order to monetize Treasury issuance which is needed to fund deficits. That, in turn, is keeping rates and yields low.

Kryptonite

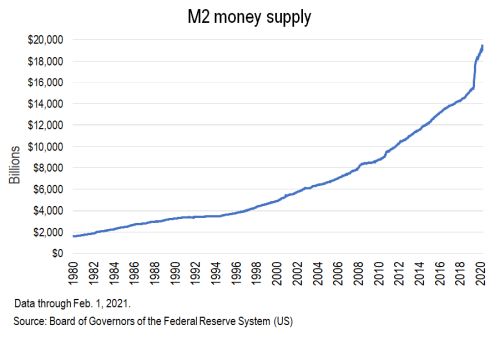

A longstanding expectation of some economists watching the growing national debt level is that its sheer size, funded by significant growth in the money supply, would spark inflation. Yet so far it has not. The following chart, from the Board of Governors of the Federal Reserve System, shows U.S. money supply from 1980 through Feb. 1, 2021.

|

Buy-sider Daniel Zwirn, credit markets specialist and chief investment officer of Arena Investors LP, believes the national debt won't in some way cause rates to rise, though he points out that he is not expressing a portfolio position.

Zwirn says that a result of today's growing national debt and low rates may be that the U.S., as well as Europe, might eventually look a lot like Japan, a reference to Japan's over-200% debt-to-GDP level. He notes that while Japan has low inflation when measured against other developed markets, it has also experienced decades of lost growth as its financial problems were spread over that time frame, instead of being dealt with earlier and more forcefully.

Cecchini echoes those sentiments. "QE is funding Japan and it isnt killing them — yet."

Zwirn expects the Fed to keep interest rates low, rather than allowing them to rise in the face of the growing national debt, which he feels would be the more appropriate action. "I don't see a Volcker 2.0" he said, referring to policies employed by Carter/Reagan-era Fed chief Paul Volcker.

In the late 1970s and early '80s, Volcker jacked up the Fed Funds rate into double-digits and used limits on the money supply to combat inflation. William Poole, former president and CEO of the Federal Reserve Bank of St. Louis, says Volcker's policies led to "not one, but two, recessions before prices finally stabilized."

While Japan looms as a possible down-case scenario, according to the CBO's February report, the U.S. national debt might not reach Japan-style levels any time soon, anyway. The CBO projects that U.S. debt-to-GDP will hold between 101% and 107% through 2031. However, the CBO also projects that, unless things change, the U.S. would reach 195% in 2050.

Marty Fridson, chief investment officer of Lehmann Livian Fridson Advisors LLC, a decades-long observer of the high yield market and a regular contributor to LCD, agrees that, at least for now, the national debt will have no direct impact on markets or interest rates. He notes that inflation-fighting would be a primary reason for the Fed to raise rates. But he currently sees nothing on the near-term horizon that will produce more than a temporary uptick in inflation that could result from pent-up demand as pandemic-related constraints ease.

According to Fridson, inflation needs — among other accelerants — a high velocity of money, a strong labor market, or a booming economy. He sees none of them.

The velocity of the U.S. money supply "has fallen off a cliff," he says (it is, in fact, lower than at any time in the past 60 years, according to the St. Louis Fed). Fridson also notes that wage pressure remains constrained in the globalized economy. He adds that he sees little danger of the U.S. economy overheating, given that the U.S. workforce is not growing, in part because of an aging population.

Fridson cautions, however, that he isn't saying inflation will never return. In fact, he assumes at some point it will — just not in the near term.

Tipping point

Though the level of U.S. national debt to many seems innocuous right now, LaVorgna believes the markets may reach a tipping point, at which U.S. debt-to-GDP is high enough to warrant concern by the markets. He doesn't know specifically what that point is, only that collectively investors may one day believe, as they did regarding European sovereign debt in the early 2010s, that the national debt has risen too high.

Fridson says roughly the same thing, noting that, "We can’t be complacent about [the national debt] — there is probably some limit to it," adding that, "but for now it's not causing inflation or any problems."

Yet the yield curve is steepening. The spread between 2-year and 30-year U.S. Treasuries has advanced from 109 basis points on July 31, 2020, to 152 bps on Jan. 1, to 203 bps at Feb. 19. A steepening Treasury curve, of course, is a classic indication of rising inflation expectations.

Article amended at 6:05 p.m. on March 17, 2021, to add clarity around interest rate costs in the 1970s.