4 Jan, 2022

3 sustainability trends for European bankers to watch in 2022

By Sanne Wass

Considerations about climate and the environment are becoming increasingly important in every banker's day-to-day work, and this focus will only intensify in 2022 as lenders, regulators and stakeholders step up their sustainability efforts and seek to bring long-term pledges to fruition.

As Kelly Fisher, HSBC Holdings PLC's head of corporate sustainability, recently put it, financial institutions need to teach bankers and relationship managers "to speak climate" if the sector is to be successful in its journey toward carbon neutrality.

Here are three key sustainability trends that will impact European bankers in 2022.

Climate stress tests

European lenders are already familiar with climate stress tests, which assess the ability of individual institutions and the financial system to cope with climate change. Regulators in France and the Netherlands have

This year will be another big one for

Though stress tests in general have become a powerful supervisory tool, there are pitfalls in existing climate-focused test frameworks, said Sam Theodore, a bank analyst at Scope, speaking on a webinar Nov. 11, 2021. One is the time frame: The ECB's 2021 climate stress test, for example, sought to project banks' loan losses 30 years from now, which is "practically impossible and really not very credible," according to Theodore.

Issues around balance sheet developments are another challenge, he said. Stress tests have typically taken a static balance-sheet approach, assuming management takes no action to address the worsening asset quality, which Theodore deemed as unrealistic and lends a stress test less practical value. While a dynamic balance sheet approach may be adopted in future tests, this carries its own uncertainties, as it is hard to predict how banks would react to climate-related disruptions, he added.

It should be noted, however, that climate stress tests today are "largely pilot schemes" and that their main purpose is to "broaden senior management and the board's understanding of these risks and to make sure that those conversations happen," said Monsur Hussain, head of financial institutions research at Fitch Ratings.

The ECB has said that the output of the climate stress test in 2022 will be integrated into its Supervisory Review and Evaluation Process, or SREP. This may lead to additional pillar 2 capital charges on individual banks, which would be enforced from January 2023 at the earliest, Hussain said. Any charges will most likely be based on the "qualitative elements" of the test, looking at how banks navigate through the stresses, including potential weakness in their decision-making and risk-management frameworks, he added.

Banks establish net-zero plans

In 2021, banks lined up behind promises to achieve carbon neutrality by the middle of the century. This year, those commitments will be put to a test as lenders translate their pledges into interim targets for high-emitting sectors.

Close to 100 banks have now signed up for the Net-Zero Banking Alliance, with European lenders making up the majority. Signatories commit to bringing greenhouse gas emissions linked to their lending and investment portfolios to net-zero by 2050, and to establish interim goals within 18 months of joining.

Those targets will be subject to intense scrutiny by shareholders, who are ready to act through resolutions and campaigns ahead of 2022 annual meetings if banks fail to take convincing steps, said Xavier Lerin, a senior banking analyst at ShareAction, a responsible investment organization that coordinates investor campaigns.

Targets for absolute carbon reduction — as opposed to setting only intensity goals based on emissions relative to total energy financed or other metrics — is one "must-have," Lerin said in an interview. It will ensure that banks focus on reducing production in carbon-intensive sectors rather than just improving carbon efficiency, he added.

Banks will also be expected to back their goals with robust policies and clear expectations spelled out for clients, said Jeanne Martin, a senior campaign manager at ShareAction.

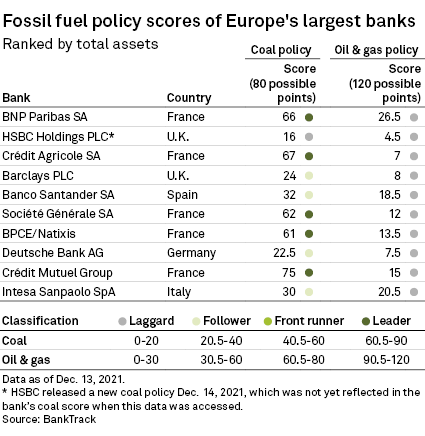

While large European banks are leading the pack when it comes to restricting the financing of coal, they have placed far fewer limitations on oil and gas, according to finance-focused campaigning organization BankTrack's assessment of banks' fossil fuel policies.

Banks, meanwhile, are asking for some leeway as they start a lengthy process of assessing clients and helping carbon-intensive companies build their transition strategies.

"The answer to this is transition, not immediate divestment. That is going to mean taking quite a lot of unpopular noise in the short term," said Tracey McDermott, chair of the Net-Zero Banking Alliance and head of conduct, financial crime and compliance at Standard Chartered PLC, at a London-based event organized by City & Financial Global on Nov. 29, 2021.

Push for more data

A shortage of data is a major challenge for banks in assessing and managing climate risks, and institutions will be expected to step up their efforts to bridge the gaps in 2022.

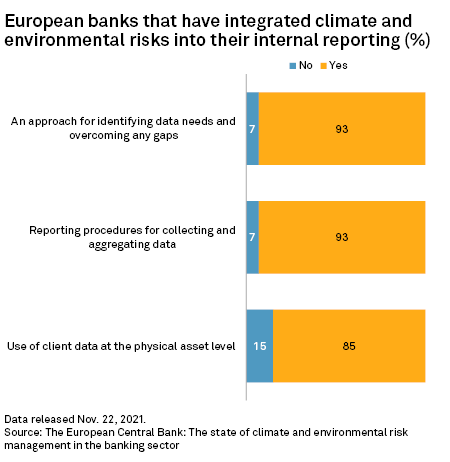

The ECB in November 2021 published an assessment of 112 European banks' climate practices and found that a lack of available data is often given as a reason for insufficient progress by institutions in incorporating climate and environmental risks into their processes. It found that just 7% of institutions have made any effort at all to take stock of the type of data they would need in order to identify and report internally on climate risks.

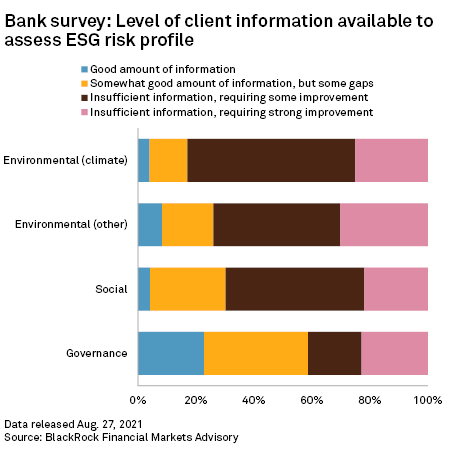

Some 83% of European banks flag environmental data related to climate as "insufficient" when assessing clients' environmental, social and governance risk profile, according to a May study conducted by BlackRock on behalf of the European Commission, which interviewed 28 European banks. In comparison, lenders reported much better coverage when it comes to data around governance.

The ECB has said it expects institutions to assess their data needs in order to inform their strategy-setting and risk management, to identify the gaps compared with current data and to devise a plan to overcome these gaps and tackle any insufficiencies.

The BlackRock study found that banks will need to bolster their own data sets as third-party providers typically lack full coverage of all asset classes, geographies and counterparty types.

Banks need a range of data to effectively measure and assess their exposure to ESG risks, including company-specific metrics on ESG-related practices such as carbon emissions and workforce diversity; transaction-level data such as asset-location; ESG standards such as energy efficiency labels; data related to climate scenario and pathways; as well as ESG scores and ratings, according to BlackRock.

"Data fragmentation is clearly a challenge," said David McNeil, head of climate risk at ESG ratings business Sustainable Fitch, speaking at a webinar Nov. 23. "Increasingly, there will be an onus on banks to be doing a lot of this data collection to supplement the work of third-party data providers and to really help address some of these gaps that we see."