BLOG — Aug 18, 2021

Weekly Pricing Pulse: Commodity prices down as iron ore market correction continues

By Michael Dall

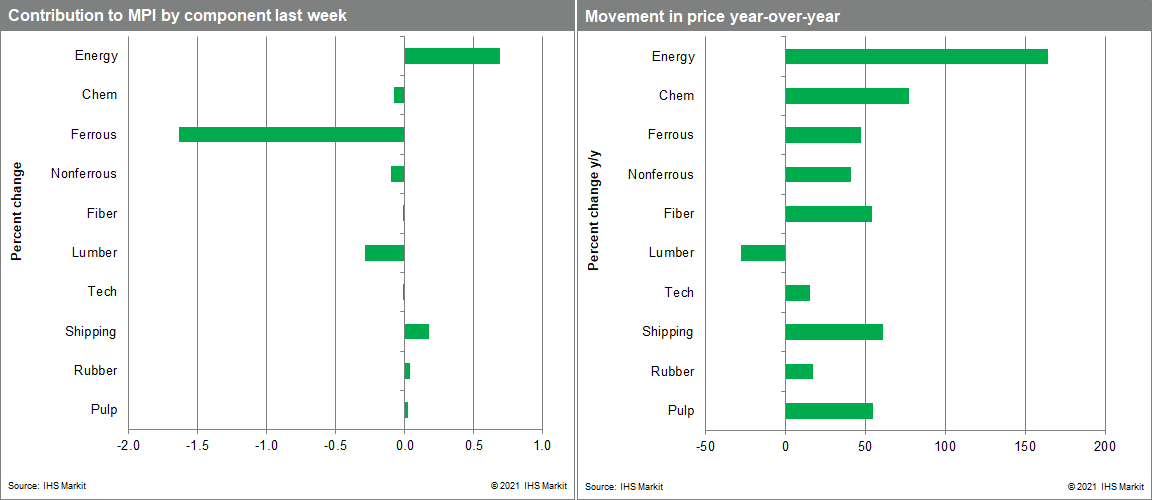

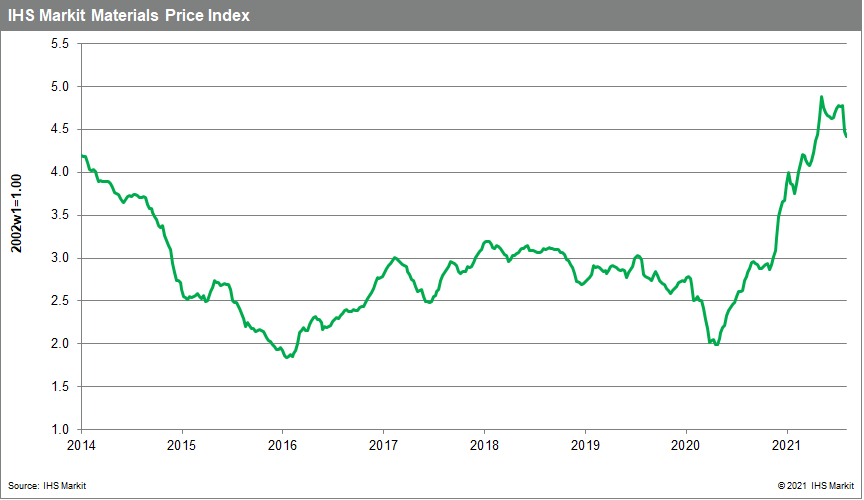

Our Materials Price Index (MPI) fell 1.2% last week, following a 6.4% drop the previous week. This latest move means commodity prices are back at April 2021 levels, reversing most of their second quarter rise. Although softening recently, prices collectively are still at an eight-year high.

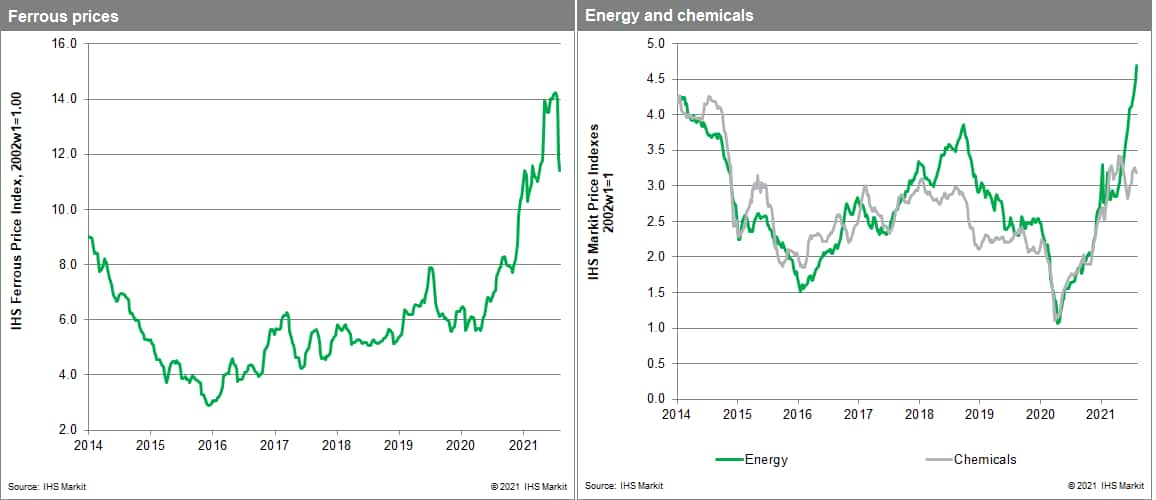

Industrial metals were the main contributor to the MPI's decline last week with steel making raw materials prices continuing to slide. Our ferrous sub-index was down 4% as both iron ore and scrap steel prices fell. This is the fourth consecutive weekly decline in the sub-index with iron ore prices down to $167 a tonne last week, the lowest level since early April. Scrap prices also dropped, falling to $456 a tonne, down from a high of $518 in late May. Recent weakening in iron ore and scrap prices is linked to uncertainty over future Chinese steel consumption. Authorities in mainland China have asked steel mills to limit production to help reduce energy consumption and meet carbon emission targets and are threatening punishment for noncompliance. This intervention has reduced demand for iron ore and scrap steel, sending prices lower. Industrial metal prices are also reacting negatively to weaker demand signals from mainland China. Copper prices were down 1.5% with Chinese copper import volumes in the first seven months of 2021 down compared to the same period in 2020. Further downward pressure on commodity prices was evident in chemical markets last week as global ethylene prices dipped. An improving supply picture and lower crude oil costs caused prices to drop 6.4% last week.

Yet another drop in the MPI reinforces our sense that the year-long rally in commodity markets has run its course. While we have been expecting a better supply-side performance in markets to bring about a change in pricing, it has been on the demand-side that recent softness has emanated. Growth has begun to slow, with markets now anxious about the spread of the COVID-19 Delta variant and what this may mean for future growth. Supply-chain disruptions and bottlenecks continue to plague markets with vendor performance not only poor but with little sign that conditions are even stabilizing. More worrisome, service sectors are now experiencing the same kinds of problems manufacturing encountered last year, which means top-line inflation pressures may persist until year-end or even into early 2022. Recent declines in commodity prices are encouraging in the sense that the acute cost pressures now present in supply chains will begin to dissipate if this recent trend continues. This said, the threat of higher inflation will not end until problems on the supply-side are resolved.