ECONOMICS COMMENTARY — Nov 05, 2021

Week Ahead Economic Preview: Week of 8 November 2021

The following is an extract from IHS Markit's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

The coming week sees some important updates on inflation from the US and China, as well as some fresh UK GDP data to help steer policy at an indecisive Bank of England. Also watch out for third quarter GDP data updates from the Philippines, Hong Kong SAR and Norway, loan data from China and industrial production numbers from the eurozone.

With the US Fed starting to taper its asset purchases, joining a gang of hawkish central banks which now includes the Reserve Bank of Australia and the Bank of Canada, the focus will be on upcoming US inflation numbers. CPI and PPI updates as well as consumer inflation expectations will help gauge the extent to which price pressures are mounting and whether the announced taper pace of $10bn will need to be adjusted in coming months.

In contrast, the Bank of England pulled back from a heavily-trailed rate hike, preferring to await more information on the resilience of the economy, and in particular the labour market. GDP data for September will therefore provide policymakers with a more detail on the UK economy's recovery momentum.

From a broader perspective, the future direction of monetary policy around the world remains to a large extent dependent on the degree to which current inflationary pressures are transitory. In that respect, producer price data published for China could prove illuminating, especially as any steep increase could flame concerns that higher exported goods prices could feed through to global inflationary pressures.

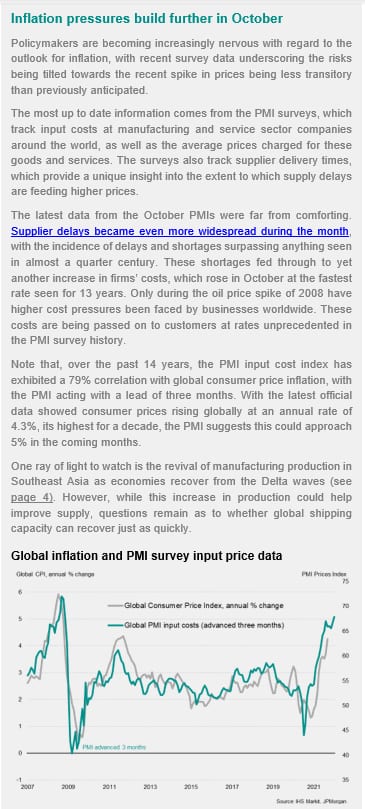

PMI commentary: Chris Williamson, Jingyi Pan

APAC commentary: Rajiv Biswas

© 2021, IHS Markit Inc. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Location