ECONOMICS COMMENTARY — Jun 11, 2021

Week Ahead Economic Preview: Week of 14 June 2021

The following is an extract from IHS Markit's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

The highly anticipated Federal Open Market Committee (FOMC) meeting will take place alongside central bank meetings in Japan, Taiwan and Indonesia in the coming week. At the same time, retail sales and industrial production data will be due from the US, eurozone and China, as well as employment and inflation data from the UK, the latter especially keenly awaited following the recent rise in price pressures seen in the US and China.

Without a doubt, the June 15-16 FOMC meeting will be the key focus in the coming week with the Fed having spent more time of late talking about their intention to start talking about tapering. Whether the Fed will let the market down easy will be scrutinised with the upcoming June meeting.

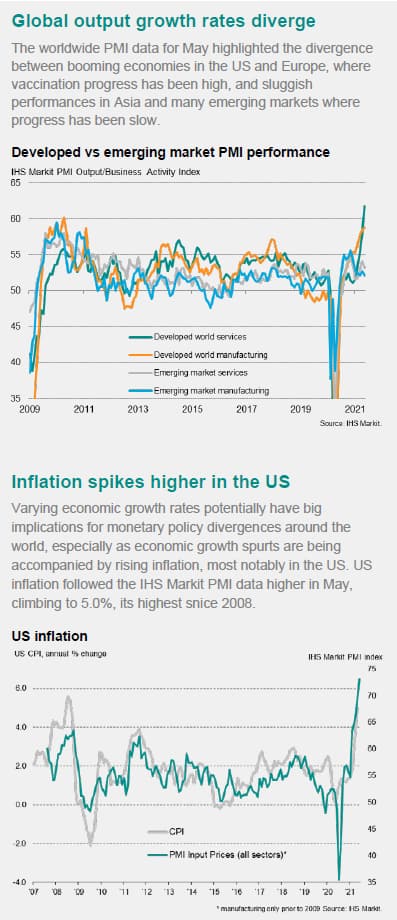

For fear of sounding like a broken record at this point, recent US data including PMIs have reflected improving economic conditions and confidence. At the same time, price pressures have built, pointing in the direction of tapering. In turn, markets have been caught in a bind between celebrating the positive economic surprises and the growing possibility of sooner than previously anticipated tapering. While guidance is awaited, one should not be surprised to find market watchers holding their breaths ahead of the meeting.

Separately, Asia central banks are expected to stay on hold, grappling with lingering COVID-19 implications. The further flow of data will, however, be of interest to assess economic conditions across the regions.

Contact us

PMI commentary: Chris Williamson, Jingyi Pan

Europe commentary: Ken Wattret

APAC commentary: Rajiv Biswas

© 2021, IHS Markit Inc. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI™) data are compiled by IHS Markit for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Location