10 Feb, 2017 | 12:00

Origination Growth Increases Securitization Opportunity For Digital Lenders

By Eric Turner

Highlights

Securitizations backed by loans originated through prominent U.S.-based digital lending platforms saw another record year in 2016 as offerings bounced back in the second half, following a sluggish start to the year.

Securitizations backed by loans originated through prominent U.S.-based digital lending platforms saw another record year in 2016 as offerings bounced back in the second half, following a sluggish start to the year.

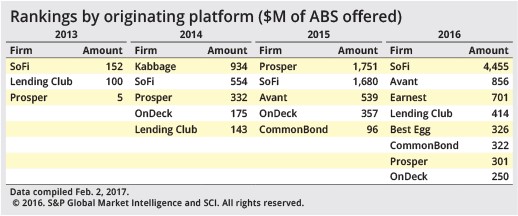

Despite credit concerns related to Prosper loan-backed issuances and a scandal at LendingClub, asset-backed offerings for companies covered in our U.S. digital lending landscape report grew 72.37% year-over-year to $7.62 billion. Student-focused lender Social Finance Inc., or SoFi, was the stand-out originator, responsible for 12 deals worth a total of $4.45 billion in 2016.

We analyzed data from Structured Credit Investor's asset-backed securities transaction database in conjunction with S&P Global Market Intelligence estimates for digital lending originations, which cover 13 companies operating in the personal, student-focused, and small and medium business lending segments. This analysis shows growth in loan originations far outpacing ABS issuance, which suggests there is room for even more digital lending securitization activity.

High second-half issuance offsets 2016's slow start

The year got off to a rough start in February 2016 as Moody's placed the class C notes of three Citigroup Inc. ABS offerings backed by Prosper Marketplace Inc. loans on review for downgrade. By March, Citi was offering a new $278.4 million Prosper loan-backed ABS deal in which the average weighted spread widened to 368 basis points, compared to 293 basis points for a similar offering in December 2015. After that deal, Citi backed away from purchasing Prosper loans and packaging them for sale to investors.

Despite the initial concerns, Moody’s confirmed the ratings on the class C notes in July 2016, noting that the underlying loans backing the transactions had not seen substantial deterioration and that structural features of the transaction combined with available credit enhancements would offset increased losses.

LendingClub Corp. presented its own set of challenges for the market with the discovery that the company improperly sold loans to Jefferies Group LLC for an ABS offering, despite knowing that the loans did not meet the requirements set forth by Jefferies. This led to Jefferies temporarily suspending its purchasing program with LendingClub and to the ouster of LendingClub CEO Renaud Laplanche in May 2016.

In the face of these issues, the market for securitizations backed by loans from digital lenders remained strong, with $7.62 billion of deals completed by eight of our 13 focus lenders during 2016. Of that amount, $4.55 billion, or 59.72%, was completed in the second half of the year. Citigroup went on to act as arranger on offerings for SoFi and Marlette Funding LLC, while Jefferies went on to complete two LendingClub ABS deals during the year totaling $205.1 million.

For 2017, we see another record year for securitized offerings amid growth in loan origination, increased utilization of securitization as a capital source, and increased involvement by investors and rating agencies. Potential headwinds include an adverse credit event in a seasoned ABS issuance, rising rates, and macro conditions that could lead to higher borrower defaults.

Successful offerings lead to new entrants and products

As digital lenders have grown loan originations to tens of billions of dollars a year, the industry has largely outgrown the peer-to-peer lending model and started tapping institutional investors and bank funding as sources of capital. Securitization has emerged as an important funding source. During the first three quarters of 2016, we estimate that the 13 focus lenders featured in our 2016 Digital Lending Landscape originated $20.64 billion in new loans; eight of those lenders completed, or had loans backing, at least one securitization during the year.

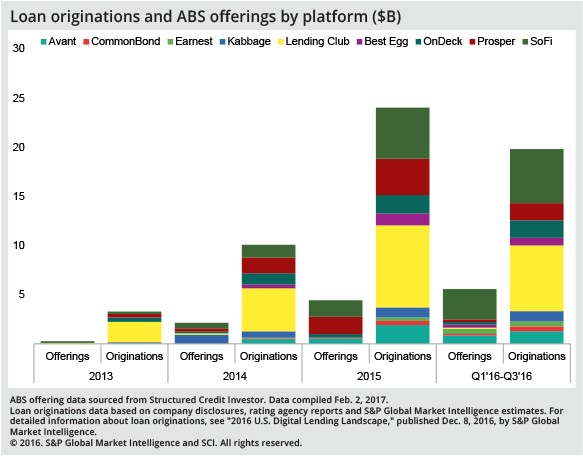

Securitization has been used by financial institutions for decades but only reached the digital lending industry in 2013, with a modest total of $257.1 million offered throughout the year. SoFi, Prosper, and LendingClub loans accounted for these issues, though SoFi was the only lender to work directly with a bank to offer loans to investors.

Offerings backed by Prosper and LendingClub loans were created by Eaglewood Capital and Insikt through the purchase of whole loans directly from the respective platforms. These loans were packaged into securities and sold to investors. Three deals backed by loans from personal lending platforms accounted for $105.3 million of offerings during the year while a single SoFi transaction accounted for $151.8 million.

A combination of issuances backed by loans from Kabbage and On Deck Capital Inc. made small and medium business-focused lenders the dominant platforms for securitization in 2014. A single $933.7 million Kabbage deal was the largest associated with any lender and accounted for 43.69% of the $2.14 billion in ABS offerings during the year.

In 2015, securitizations backed by loans from personal-focused lenders amounted to $2.29 billion. This also marked the first year in which a single platform accounted for more than $1 billion in ABS deals, as Prosper and SoFi ended the year with $1.75 billion and $1.68 billion in new offerings, respectively.

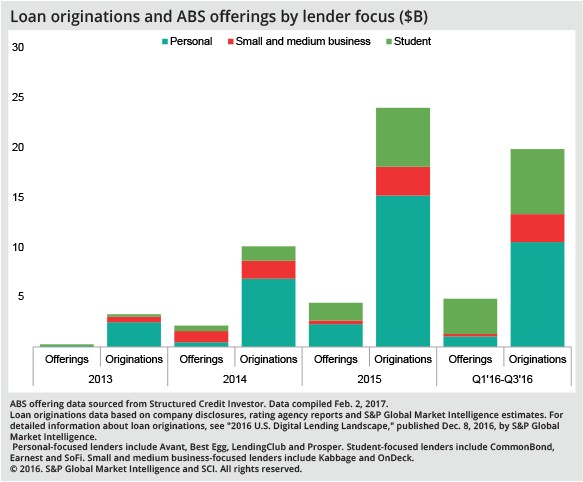

During 2016, student-focused lenders SoFi, Earnest and CommonBond in aggregate accounted for more ABS issuance than personal- or business-focused digital lenders. These student-focused lenders primarily rely on balance sheet or credit facility funding to make loans. As loans build up on the balance sheet, lenders often find it necessary to sell them to free up capital or pay down credit facility balances. Because securitized offerings are an efficient way to do this, these lenders will likely remain a steady source of new deals.

SoFi also introduced the residential mortgage category to the digital lending ABS space in 2016 with its $158.6 million RMBS offering arranged by Barclays Capital Inc. SoFi has made great strides in the mortgage business and is likely to account for at least one RMBS deal in 2017. We are unlikely to see RMBS activity from other focus lenders as SoFi is the only platform currently offering a mortgage product.

Even with rapid deal growth, new issuance capacity remains

Since 2013, nine of the 13 lenders on our focus list have had loans backing at least one securitization. Through the third quarter of 2016, we estimate that these nine lenders had originated $19.82 billion in loans. Of the focus lenders that had been previously active in the ABS market, Kabbage was the only one not associated with a new ABS transaction in 2016.

SoFi was by far the most dominant digital lending platform in terms of securitization during the year, accounting for 58.42% of total deal volume. It buoyed an ABS market that would have otherwise been brought down by an 82.82% decline in Prosper loan-backed offerings, which was largely due to the end of Citigroup’s loan purchase program with the platform.

Personal-focused lender Best Egg, which is part of Marlette Funding, and student-focused lender Earnest had their first ABS deals in 2016. Best Egg has been a standout in the personal lending space, growing from just $600,000 in originations in the first quarter of 2014 to an estimated $248.6 million in the third quarter of 2016. There were two Best Egg loan securitizations in 2016, and Marlette has signaled its desire to continue offering ABS in the future.

Even as the dollar value of new securitization deals continues to increase, there is still capacity for new offerings. Annual originations continue to far outweigh new offerings at our focus lenders. ABS offerings totaled only $4.42 billion in 2015, compared to $24.04 billion in estimated loan originations by focus lenders that have been involved in securitizations. This represents an 18.40% new offering-to-origination ratio, which was lower than the 21.18% ratio observed in 2014.

This drop was mainly due to higher originations in 2015. ABS offerings grew 107% between 2014 and 2015 while estimated originations grew more than 138%. During the first three quarters of 2016, there were $5.35 billion in new ABS deals, compared to $19.82 billion in loans originated by the nine focus lenders that have been involved in securitizations. This 26.98% new offering-to-origination ratio is the highest of any year in our analysis.

Even as this ratio grows, it remains relatively low. This illustrates the ability for lenders to meet potential increased demand from investors even after accounting for loans that do not meet the criteria for an offering, are held by the lender, or are included in new offerings as credit enhancement.

More growth, a solidifying investor base, and new participants seen for 2017

As the market has proven resilient in the face of headwinds, the use of securitization is unlikely to slow down, and 2017 stands to be another record year for deals in the space. Already in 2017, SoFi has announced a new $564.0 million issuance of consumer loan-backed securities and made it clear that it plans to continue with RMBS transactions following the inaugural December 2016 issuance. The company continues to grow its mortgage business and recently launched the product in New York State. In addition to SoFi’s RMBS offerings, we could see deals from niche players, such as Money360 or RealtyShares, which offer digital lending to fund commercial real estate transactions.

The continued need for capital at incumbent lenders, coupled with the entry of new lenders in the space, will help fuel increased offerings for the year. We will likely see more platforms move away from a marketplace model and become primarily direct or hybrid lenders. Direct lenders use only balance sheet, credit facility or ABS financing. Hybrid lenders use a combination of direct lending and a marketplace, where investors can directly purchase single whole loans. Some historically marketplace-focused lenders have started to rely more on internal capital and bank funding to meet loan demand, moving them toward a hybrid model. Platforms like SoFi and Avant have already started to make this move, and if capital remains available, it may make sense to hold more loans for investment and securitize as needed. LendingClub, a longtime proponent of a pure marketplace model, has recognized the value in facilitating the purchase of large loan portfolios from its platform.

As offerings have grown in size and number, the market has built a solid investor base as well. Offerings from SoFi in particular have proven appealing to institutional investors, including large insurance companies like Zurich Insurance Group Ltd. and Chubb Ltd., as well as asset managers like Jeffrey Gundlach’s DoubleLine Capital that have been active buyers of personal and student loan-backed ABS. We view this as a positive indicator for future growth since these investors have likely conducted a significant amount of due diligence on the platforms and their offerings, making them more likely to purchase new securities in the future. SoFi has served as a prime example of how steady issuance appeals to large investors looking for on-the-run offerings for valuation and liquidity purposes. As investor interest has increased, rating agencies have taken note of the space, with S&P Global Ratings, Moody’s, Fitch Ratings, Kroll Bond Rating Agency and DBRS all rating issues backed by loans from digital lenders.

While it appears that 2017 will see smooth sailing, the market could face potential headwinds. A credit event, such as a large default affecting a seasoned ABS issuance, or a ratings downgrade could push investors to the sidelines. As interest rates rise, investors may also demand higher yields, making new offerings economically unappealing to originators. While the majority of ABS have performed within the limits established at the time of the offering, it remains to be seen how loans in the industry perform in an adverse economic environment. In the event of a market downturn, we would likely see the disappearance of marketplace loan-backed offerings as third-party purchasers exit the space. Direct and hybrid lenders would still need capital to continue operations, and yield spreads would widen on new offerings.