29 Jun, 2017 | 11:15

Multichannel Services & VSPs Outlook

Highlights

The following post comes from Kagan, a research group within S&P Global Market Intelligence.

To learn more about our TMT (Technology, Media & Telecommunications) products and/or research, please request a demo.

The intensifying erosion of traditional multichannel subscribers in the U.S. is further splintering a video landscape in which streamed bundles, online subscription services, self-aggregation and even over-the-air delivery are playing more prominent roles.

The inexorable impact of changing consumption habits have multichannel service providers bracing for mounting losses, while virtual service providers (VSPs) are lining up to capitalize, despite their own economic challenges and over-the-top options taking advantage of the inflection.

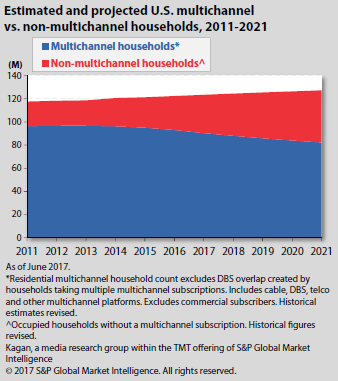

Estimated and Projected U.S. Multichannel vs. Non Multichannel HHs (2011 to 2021)

The frenetic transformation has amplified the conditions for change and instability in the market, according to the latest segmentation of video delivery options among U.S. households from Kagan, a media research group within S&P Global Market Intelligence.

While households with a traditional multichannel subscription are positioned to remain in the solid majority in the five-year outlook, upward momentum lies firmly with alternative services, which combined account for a non-multichannel tally on pace to exceed one quarter of occupied households in 2017, and crest one third by 2021.

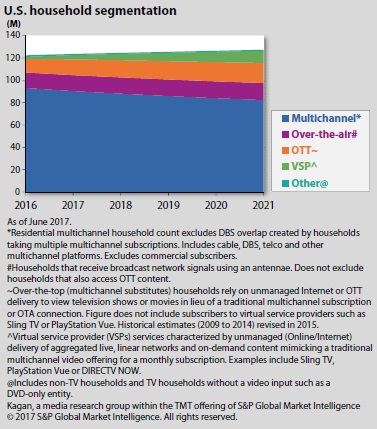

U.S. Household Segmentation

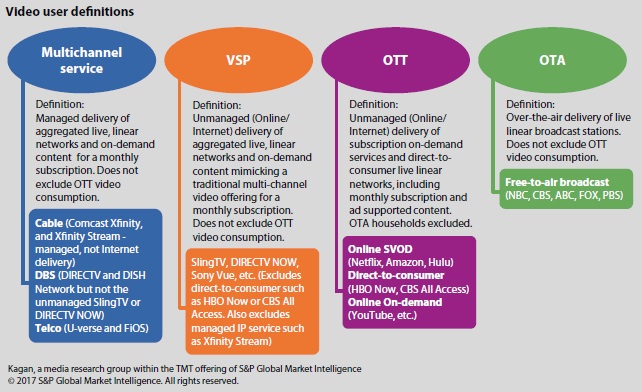

The segmentation of non-multichannel households includes three primary subgroups: OTT-only, VSP, and OTA households. The key directions in the outlook ended 2021 are as follows:

- Total multichannel subscriptions down 11.4 million to 86.6 million

- Residential multichannel households down 10.8 million to 82.3 million

- OTT up 5.8 million to 17.9 million

- VSPs increasing 9.1 million to 10.9 million

- OTA gaining 1.4 million to 15.3 million