ECONOMICS COMMENTARY — May 09, 2023

Monthly PMI Bulletin: May 2023

By Chris Williamson and Jingyi Pan

The following is an extract from S&P Global Market Intelligence's latest Monthly PMI Bulletin. For the full report, please click on the 'Download Full Report' link.

The global economic expansion accelerated at the start of the second quarter, buoyed primarily by faster services activity growth while manufacturing performance lagged. Consequently, developments on the inflation front likewise diverged, though a key question for the inflation outlook is how durable the ongoing service sector resurgence will be.

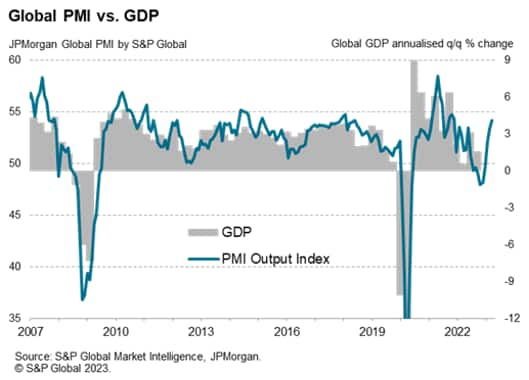

The J.P.Morgan Global Composite Output Index - produced by S&P Global - posted 54.2 in April, up from 53.4 in March. This marked the third consecutive monthly expansion of the global economy, at the fastest pace since December 2021. The latest reading is indicative of global GDP rising at a quarterly annualized rate of approximately 4.0%.

Although both manufacturing and service activity grew at faster rates, the gap between the rates of expansion widened for a second straight month to signal an increasing sectoral divergence. This was mainly accounted for by faster service sector growth amid increased demand, especially within the consumer services sector, where tourism activity further surged at the start of the second quarter. This consumer services surge was especially prominent in Asia, following the removal of COVID-19 containment measures in mainland China, but also reflects the global economy's first year of unrestricted global travel since the pandemic.

Meanwhile manufacturing sector output rose for a third straight month, albeit only mildly. While new orders for goods remained in contraction territory, the healing of global supply chains enabled the improvement in output performance. That said, the lack of demand growth remains worrying, especially if the surge in demand for services wanes in the months ahead.

© 2023, S&P Global Inc. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.