S&P Global — 30 May, 2023 — Global

Daily Update: May 30, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

The ‘What, Me Worry?’ Economy

The satirical publication Mad Magazine featured a fictitious mascot and frequent cover model named Alfred E. Neuman. Neuman’s catchphrase, “What, me worry?” indicated a heedless nonchalance in the face of criticism or danger. The global economy seems to have adopted a similar attitude as the first half of 2023 draws to a close. Despite frequent predictions of impending recession, economic indicators remain upbeat. But everything is not peachy for the global economy. The factors that led many economists to predict a downturn are still with us — lingering inflation, rising interest rates, bank failures and geopolitical tensions. Yet unemployment is low, demand remains high and many economies are still growing. Signs continue to point to recession, but the recession fails to arrive.

S&P Global Ratings Chief Economist Paul Gruenwald pointed out that the baseline forecast remains unchanged. The US and Europe will experience modest growth in 2023, but a downturn is still projected for the end of 2023 leading into 2024. China’s and India’s growth will continue to be strong. A notable outlier is the UK, where output is expected to contract 0.5% this year. However, some financial fragility revealed by the collapse of banks in the US and Europe means that risks for the global economy remain on the downside.

According to Gruenwald, there is a possible scenario in which “the recent turbulence and ongoing uncertainties lead to a pullback in spending, particularly for services, which have been driving outsize performance in recent quarters. This in turn leads to lower demand, output and employment, pulling down growth. It also will dampen both wage and inflation pressures.”

Balanced against this downside is the continued strength of the global economy. The service sector is resurgent, and the latest output numbers indicate that global GDP is rising at a quarterly annualized rate of about 4.0%. As shortages of semiconductors have eased, global automobile production and sales have bounced back. Commodity prices have moderated, particularly as the Global North enters summer and heating costs fall.

While demand for goods has eased and manufacturing new orders fell for the 10th successive month in April, the demand for services is keeping up inflationary pressure. Central banks have indicated a willingness to halt or pause rate increases as inflation shows signs of moderating. However, annualized inflation remains well above targets in both developed and emerging markets.

The aggregate picture is one of a global economy that continues to grow and a recession that remains “just a few quarters away.” But worrying issues threaten to derail the global growth story, including fragility in the banking sector and weak manufacturing numbers. There are plenty of good reasons the global economy should be in recession and only one reason it isn’t: The economy keeps growing.

Today is Tuesday, May 30, 2023, and here is today’s essential intelligence.

Written by Nathan Hunt.

Economy

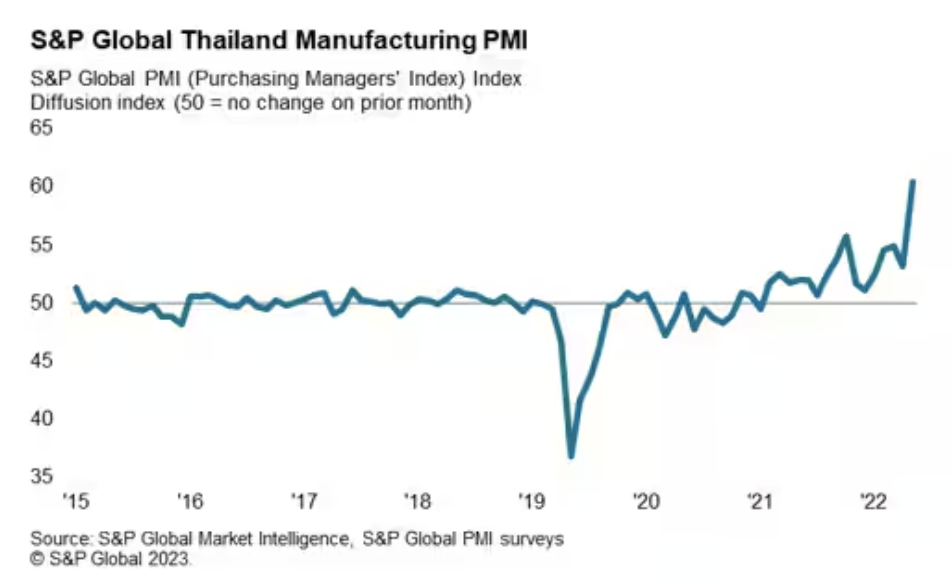

Thailand's Economy Rebounds In Early 2023 As Tourism Surges

Thailand has shown a gradual economic recovery from the COVID-19 pandemic during 2022, helped by rising international tourism arrivals. Real GDP growth rose from 1.5% in 2021 to 2.6% in 2022, with growth momentum expected to improve further in 2023. The latest S&P Global Thailand Manufacturing PMI survey results for April 2023 showed a strong upturn in manufacturing output and new orders. Due to the importance of international tourism for the Thai economy, the strong rebound in international tourism inflows evident in early 2023 signals that the tourism economy will be a key growth driver in 2023.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

Prime Assets Will Help Shield Australia's Office REITs From Rising Stress

Australia's office market is facing cyclical and structural threats. Heightened interest rates are an overall drag on the economy and have led to rising financing costs and increasing capitalization rates for office REITs. The sector is also structurally vulnerable to workplaces adopting flexible working practices. These factors will continue to weigh on office asset valuations, earningsa nd credit metrics. S&P Global Ratings believes prime-grade assets will be better positioned than secondary-grade assets, given their strong tenants and ability to adjust to changing market conditions. The seven office-focused Australian REITs (AREITs) it rates showed resilience to its stress tests on rental and asset-value declines.

—Read the report from S&P Global Ratings

Access more insights on capital markets >

Global Trade

Corn Tests Two Centuries Of US-Mexico Relations

The US and Mexico celebrated 200 years of diplomatic relations in December 2022, but the food crop corn is now testing that relationship. The North American neighbors have perhaps one of the closest bilateral ties in the world, backed by robust economic and trade relations, with both generating hundreds of billions of dollars in trade revenues for each other. Electronics, vehicles, fuels, minerals, plastics and machinery are the biggest US exports to Mexico. Fuel oil, gasoline, motor vehicle parts, passenger and commercial vehicles form the bulk of Mexican supplies to the US.

—Read the article from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

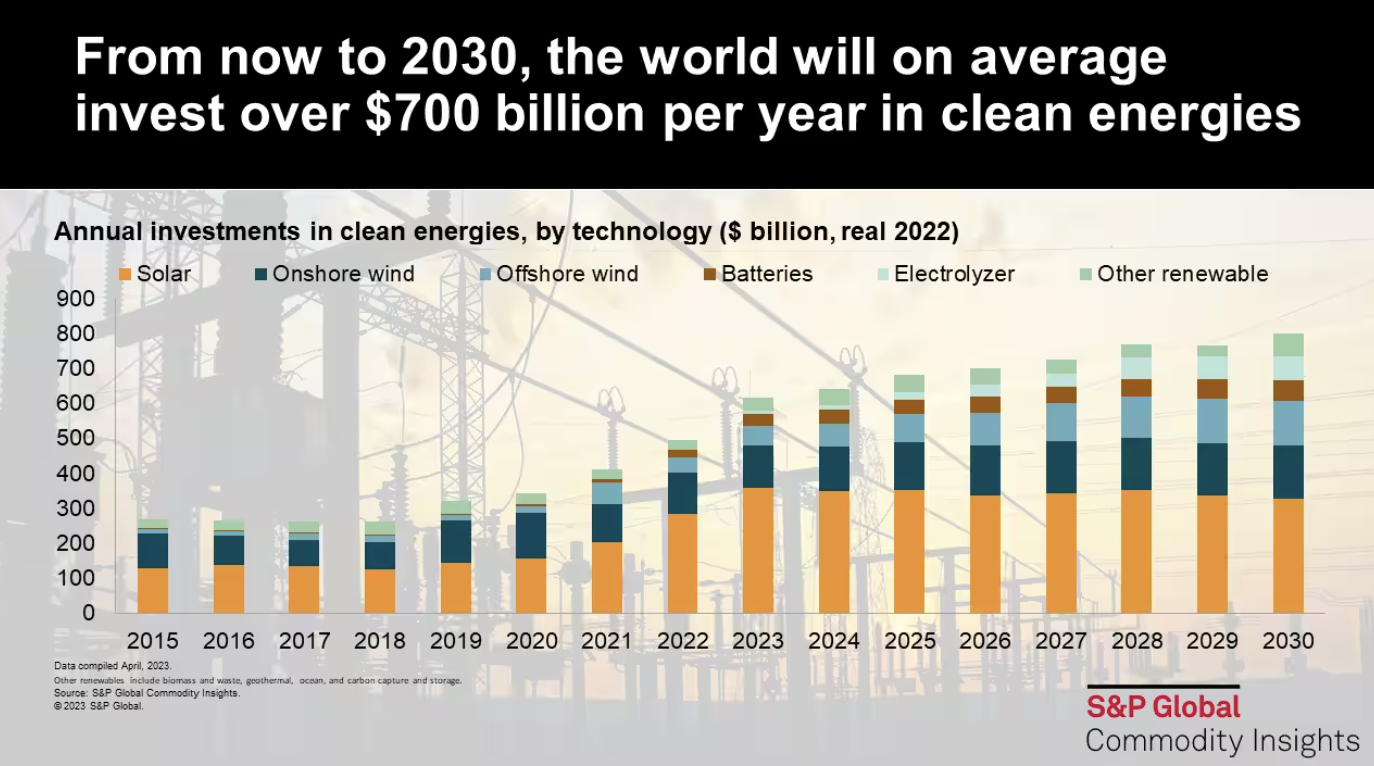

How Will Global Investments In Clean Energy Evolve To 2030?

From 2015 to 2022, worldwide deployment of clean energy resources grew from 120 GW per year to 325 GW per year. By 2030, in S&P Global Commodity Insights’ reference outlook, this figure reaches 540 GW annually. This evolution is transforming power market operations worldwide, stimulating the sector's supply chains and advancing the global effort to decarbonize.

—Read the article from S&P Global Commodity Insights

Access more insights on sustainability >

Energy & Commodities

Listen: From Russia To Asia: Oil's New Map May Prompt Policy Rethink By OPEC+

As Asian oil demand recovery shows signs of sustaining the strong momentum, there were two key questions that's keeping refiners on tenterhooks — if purchasing Russian crude would increasingly get tougher following the recent pledge by G7 leaders to ensure stricter policy enforcement. And, if OPEC and its allies would aim for further cuts as prices have climbed down to relatively modest levels.

—Listen and subscribe to Platts Oil Markets, a podcast from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

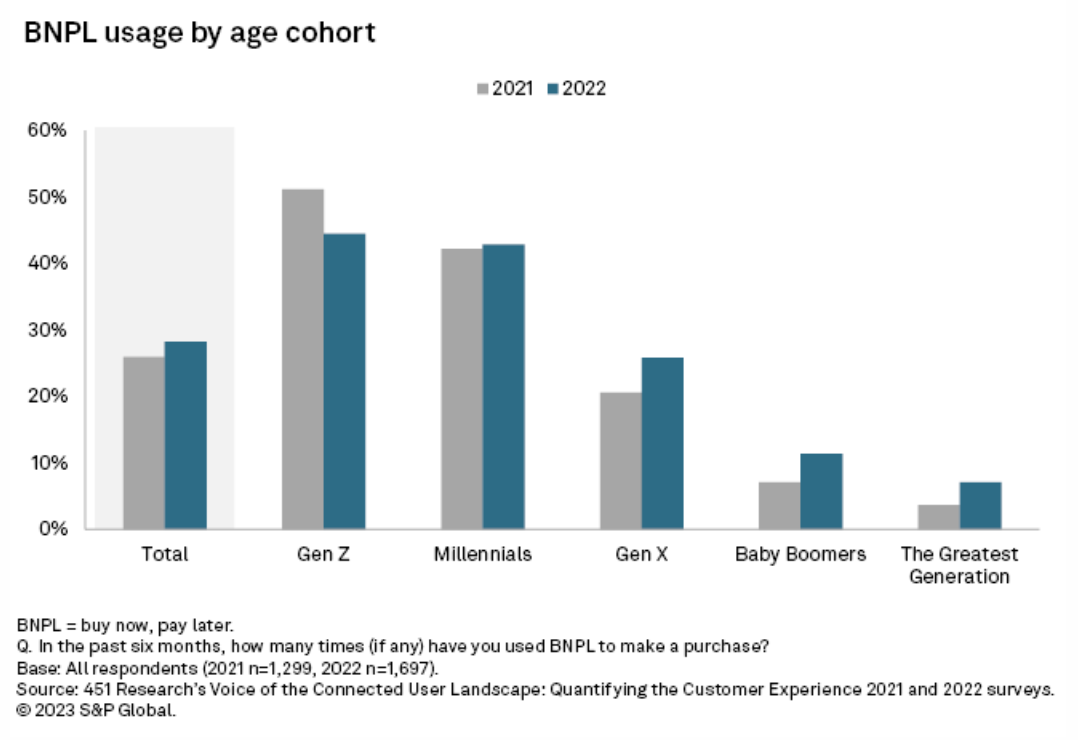

Apple Entry Adds To Ecosystem Turbulence In 'Buy Now, Pay Later' Market

After years of momentum, the dust has yet to settle in the "buy now, pay later" (BNPL) market. Apple Inc. on March 28 launched Apple Pay Later, which enables Apple Pay users to split payments into four interest-free installments over six weeks. It is in its pre-release phase for select users, with a wider rollout planned. Apple's entrance into BNPL signifies the maturity of the market and a potentially widening opportunity for large financial technology companies to play a more prominent role in providing BNPL. On the other hand, rising interest rates are compressing BNPL providers' margins, and a lack of consumer ability to make repayments remains a concern across the industry.

—Read the article from S&P Global Market Intelligence

Content Type

Location

Language