S&P Global — 23 May, 2023 — Global

Daily Update May 24, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

The Slow-Motion Belly Flop of US Commercial Real Estate

In the wake of the pandemic, US office workers and their employers are showing a preference for working from home. While this preference is hardly universal — some companies and industries have insisted on a return to the office — office buildings are emptier, lunch reservations are easier to come by and commuter trains have more room than they did in 2019. This has led to dire warnings of a “doom loop” for major US cities. As US commercial real estate loans mature, the bill will come due. The question is whether the costs of a collapse in commercial real estate can be spaced out enough that losses are absorbed without contagion risk for the larger economy.

Commercial real estate (CRE) covers a wide range of assets including offices, warehouses, supermarkets and department stores. While retail spaces have also suffered through the pandemic and the widespread adoption of e-commerce, much of the concern in the CRE market is focused on offices. Traditionally, office rentals have been a lucrative and reliable source of regular income. Real estate investment trusts created portfolios of real estate assets that have been popular with investors. Some REITs focus on office spaces, while others focus on warehouses, datacenters or retail spaces. New funding into REITs had slowed to a trickle as of April 2023, down 61.3% year over year.

Vacancy rates in commercial office spaces have increased since the COVID-19 pandemic. In New York City, San Francisco and Atlanta, vacancy rates stand at about 20%, which exceeds the level from before the pandemic. Anecdotally, landlords have been offering reduced rents and concessions to maintain occupancy. Because office leases tend to extend over multiple years, it is possible that vacancy rates will increase further as businesses choose not to renew, or to reduce, their office footprint. According to real estate services firm Colliers, 93.95 million square feet of office space was available in Manhattan, NY, as of April 2023, up 74.5% from March 2020.

According to S&P Global Market Intelligence, about $1.078 trillion in CRE loans are scheduled to mature in 2023 and 2024. Most of these loans are held by regional banks, which are already under pressure due to deposit flight after the high-profile failures of some regional banks. However, some market observers believe that the losses in CRE loans will be spread out over time, so most banks should be able to absorb the losses. Almost half of US office REIT leases expire in five or more years. This gives regional banks, insurance companies and investors time to book losses or sell assets, as well as time for the market to turn. The majority of US banks started tightening CRE lending standards in the first quarter of 2022.

According to a report from CBRE Group, CRE investment in the US fell 57% year over year in the first quarter. Short sellers have been quick to notice the decline, and short positions in the real estate sector have jumped to 3.35% since the end of February as investors anticipate further losses in the CRE market. Insurance companies such as Aflac, which invested almost 30% of its portfolio in CRE, are anticipating losses. Approximately $500 million of Aflac's commercial mortgage loans are expected to enter some form of foreclosure.

While empty offices may be grim news for some investors, there are years to go before most losses will be realized. If the last three years have taught us anything, it’s that a lot can change in a relatively short period of time.

Today is Wednesday, May 24, 2023, and here is today’s essential intelligence.

Written by Nathan Hunt.

Economy

An Asynchronous Global Economic Expansion

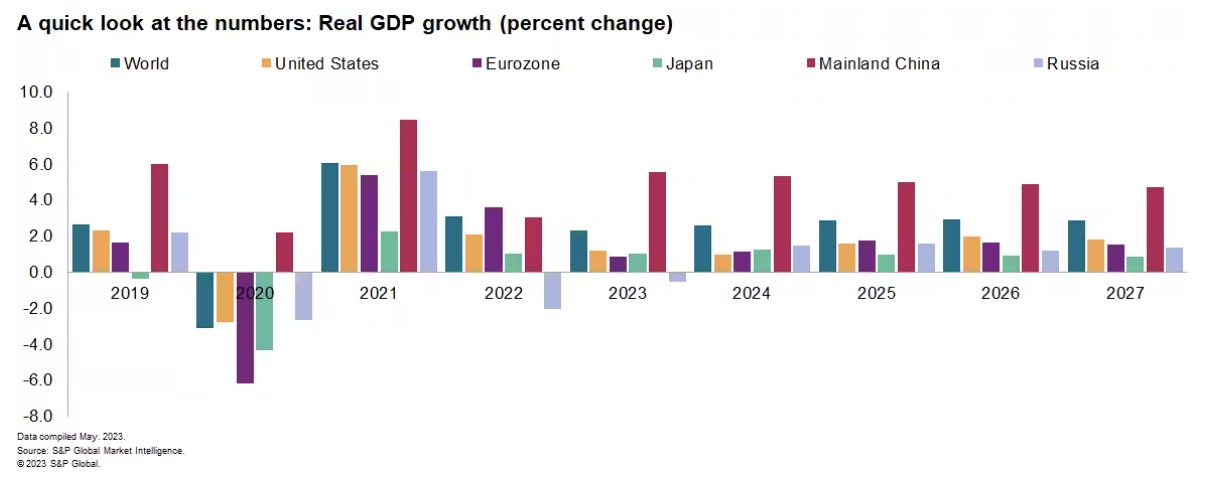

Despite the challenges of high inflation, tightening financial conditions and geopolitical conflicts, the global economy is likely to avert a recession. World real GDP growth picked up from an annual rate of 1.6% quarter over quarter in the final quarter of 2022 to 2.5% in the first quarter of 2023. Aside from a mild deceleration in the second quarter, this moderate growth pace will likely be sustained. After a 3.1% advance in 2022, the S&P Global Market Intelligence forecast calls for world real GDP to increase 2.3% in 2023, 2.6% in 2024 and 2.9% in 2025.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

A 5-Year Sector View Of Global Limited Partner Co-Investments With Private Equity

The slowdown in private equity fundraising and hurdles to dealmaking has prompted both limited partners and fund managers to team up on more co-investment opportunities. Sovereign wealth funds (SWF) tend to do fewer deals but write bigger checks. Over the past five years, SWFs invested the highest total amount of the limited partner groups at $331.41 billion across 469 co-investments. Pension funds have a similar dynamic. They executed only 288 deals for a total amount of $193.40 billion but had the highest average median deal at $165.20 million.

—Read the article from S&P Global Market Intelligence

Access more insights on capital markets >

Global Trade

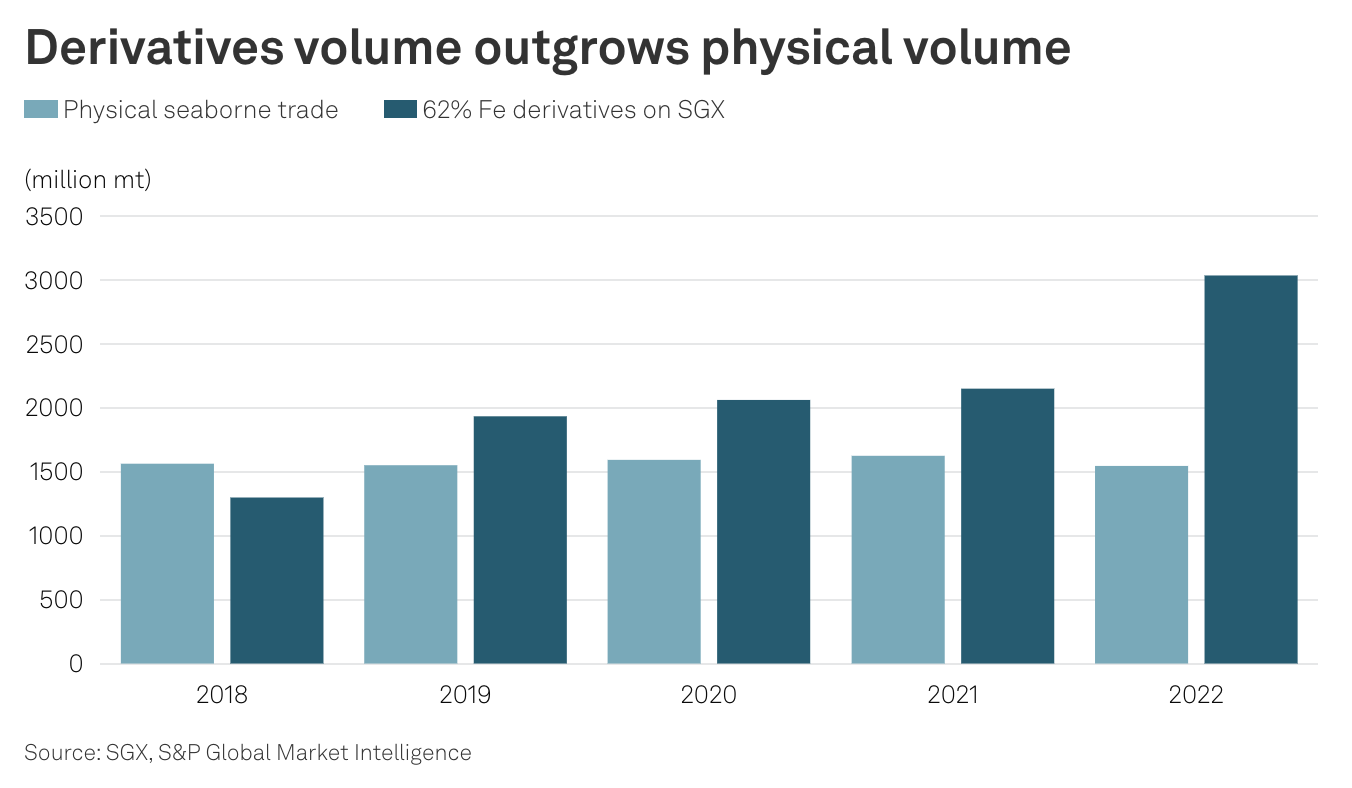

Futures Rising: A Surge In Iron Ore Derivatives Is Bringing The Market To The Cusp Of A New Evolutionary Stage

In this report, S&P Global Commodity Insights and S&P Dow Jones Indices examine the recent growth in iron ore derivatives trading, increasing market transparency and their interface with spot price assessments for the physical market. Iron ore as an investment tool from a financial perspective is also considered.

—Read the report from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

Listen: A Net-Zero Future Could See Gas Utilities Tap The Heat Beneath Our Feet

How can we heat and cool homes in a safe, non-emitting and affordable way? Well, one nonprofit says networked geothermal systems are the answer. Networked geothermal uses ground source heat pumps to heat and cool buildings without fossil fuels in neighborhoods or city blocks, cutting down on methane leakage. The nonprofit Home Energy Efficiency Team is working with natural gas utilities and state policymakers to transition gas utilities to use more networked geothermal systems.

Zeyneb Magavi, the group's co-executive director, joined the podcast to discuss current efforts to transition more of the country from gas to geo. She spoke with S&P Global Commodity Insights reporter Tom Tiernan about projects in the works, policies that are aiding the move to geothermal and the costs both utilities and utility customers could expect from transitioning to a networked geothermal system.

—Listen and subscribe to Capitol Crude, a podcast from S&P Global Commodity Insights

Access more insights on sustainability >

Energy & Commodities

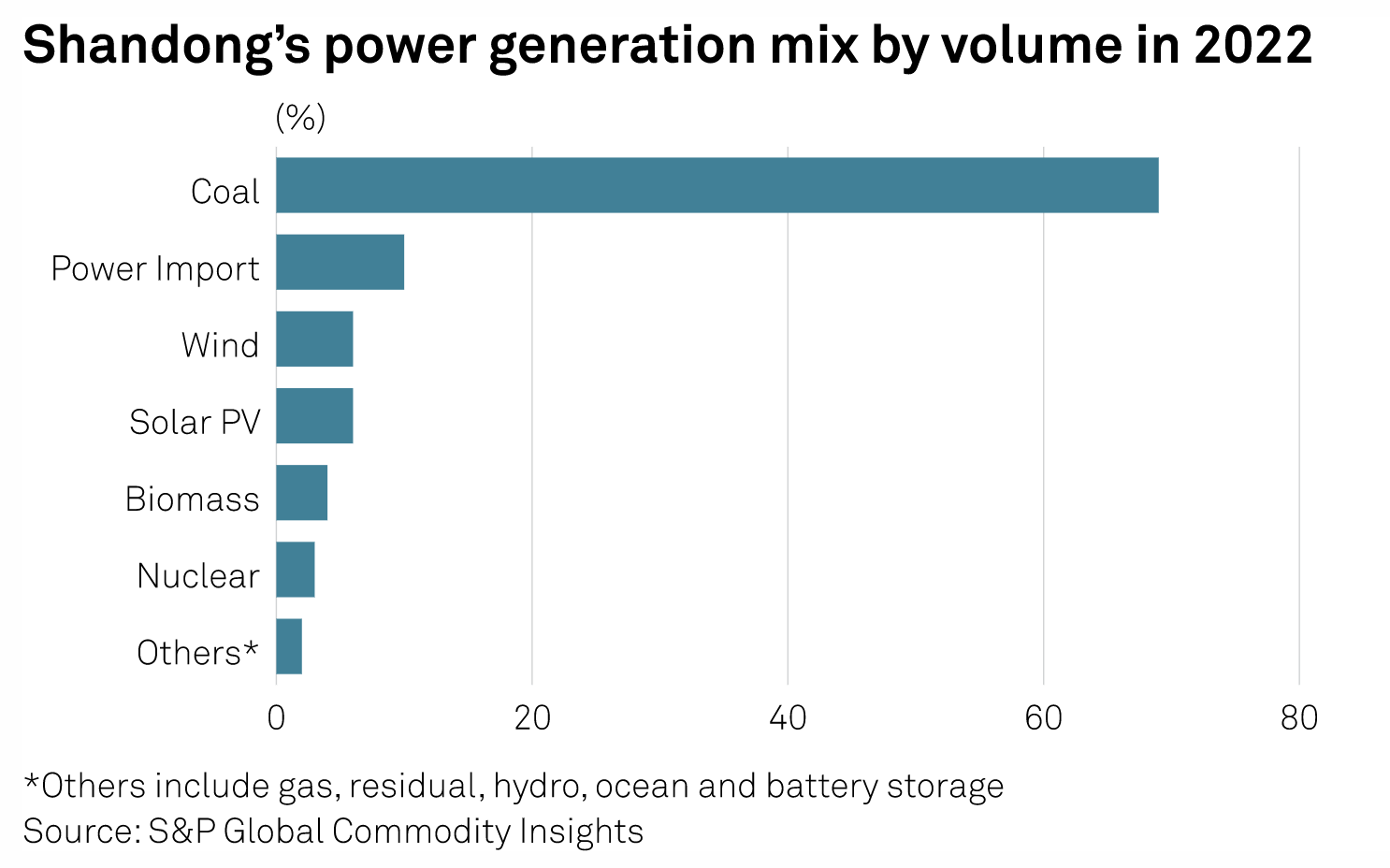

Negative Electricity Prices In Shandong Put Spotlight On China's Energy Transition Challenges

China's northeastern province of Shandong is the country's second-largest power producer and third-largest power consumer by volume. It also hosts China's highest solar PV generation capacity and was the largest coal-fired power producing province in 2022. In recent weeks, Shandong has exhibited a phenomenon that has become the hallmark of energy transition in the power sector in several parts of the world including Australia, the US and Europe — negative electricity prices.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

China's Internet Regulation: Fewer Surprises, Not Zero Surprises

China's internet sector has emerged from its regulatory shakeup. Policymakers are signaling support and seem done with big legal changes or sweeping actions. The period of big surprises is likely in the rear-view mirror. Yet changes made will not be unmade. S&P Global Ratings believes operating conditions are forever altered. Stricter enforcement of China's anti-monopoly law means that internet companies will need to invest in their core businesses and perhaps selectively in new businesses to ensure they are not disrupted. And social media companies may need to spend more resources on content moderation to control regulatory risks.

—Read the report from S&P Global Ratings

Content Type

Location

Language