S&P Global — 21 Sep, 2023 — Global

Daily Update September 21, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Implications of United Auto Workers Strike

On Sept. 14, the four-year contract between the United Auto Workers (UAW) union and three legacy Detroit auto manufacturers expired. On Sept. 15, the UAW began a strike at a limited number of key plants focused on midsize truck and utility vehicles. Several offers from the three auto manufacturers — Ford, General Motors and Stellantis — were rejected by the union, and the parties remain far apart on issues including wages, benefits, job security and paid time off. The UAW suggested that additional plants may be added to the strike over time if an agreement is not reached. This could be as soon as Sept. 22, as the UAW has issued another deadline for making progress. Given that the UAW represents over 140,000 workers at the abovementioned auto manufacturers, and the role of the auto sector in the wider economy, this strike has implications for the auto industry, the US economy and global trade.

"While the UAW strike starts with three vehicle assembly plants, this signifies the beginning of a potentially long-lasting and damaging strike,” said Joe Langley of S&P Global Mobility. “This strategy aims to gradually intensify pressure on the manufacturers in the coming weeks with more plants expected to strike. It starts with daily losses of 3,264 units and could ultimately lead to cumulative losses reaching hundreds of thousands of units.”

S&P Global Mobility estimates that the strike as it currently stands could impact about 3,200 units per day, and that other plants have begun experiencing downtime as a result. Prior to the strike, the light-vehicle production forecast for the year at the three struck plants was already down 17% compared to 2022 in the midsize pickup-truck segment. Larger-scale, Ford, GM and Stellantis accounted for about 49% of US light-vehicle production in 2022. Many of the automakers have sufficient inventories of light vehicles that should allow them to meet consumer demand, depending on the length of the strike. If the strike continues at these specific plants, it could hand an advantage to rival Toyota, as it is about to launch a redesigned Tacoma into this segment. Additional plant strikes are expected to be announced on Friday by UAW leadership if substantial progress toward a new contract has not been made.

"The depth of the strike impact will depend on the length and whether it is expanded to other plants, and these are unknowns so far,” said Stephanie Brinley of S&P Global Mobility. “However, in terms of perception and consumer expectations, the uncertainty created by a well-publicized strategic strike has potential for a more immediate impact. This could play out in consumers looking to close vehicle purchases more quickly over a perceived concern for lack of inventory, while others may pull back and opt to wait it out.”

Auto manufacturers have dedicated their efforts to increasing the efficiency of their operations in recent years. As a result, labor costs are just 5% of manufacturing expenses for vehicles made in the US. However, should those costs increase significantly, adding perhaps 2% to the vehicle price, analysts at S&P Global Market Intelligence believe that may create a price disadvantage for US-made vehicles produced under this labor contract. The impact of a strike of limited duration would be small for US GDP. However, the impact for automotive supply chains, particularly in the US, Mexico and Canada, could be substantial.

S&P Global Ratings does not anticipate changes to corporate credit ratings for automakers as a result of this strike. A meaningful cushion for industry volatility is already incorporated into financial risk assessments for the auto industry. For auto suppliers, the S&P Global Ratings team also anticipates that the strike will have a limited impact on credit metrics. S&P Global Ratings anticipates that lost volume for auto suppliers would be recovered quickly when the strike ends.

Today is Thursday, September 21, 2023, and here is today’s essential intelligence.

Written by Nathan Hunt.

Economy

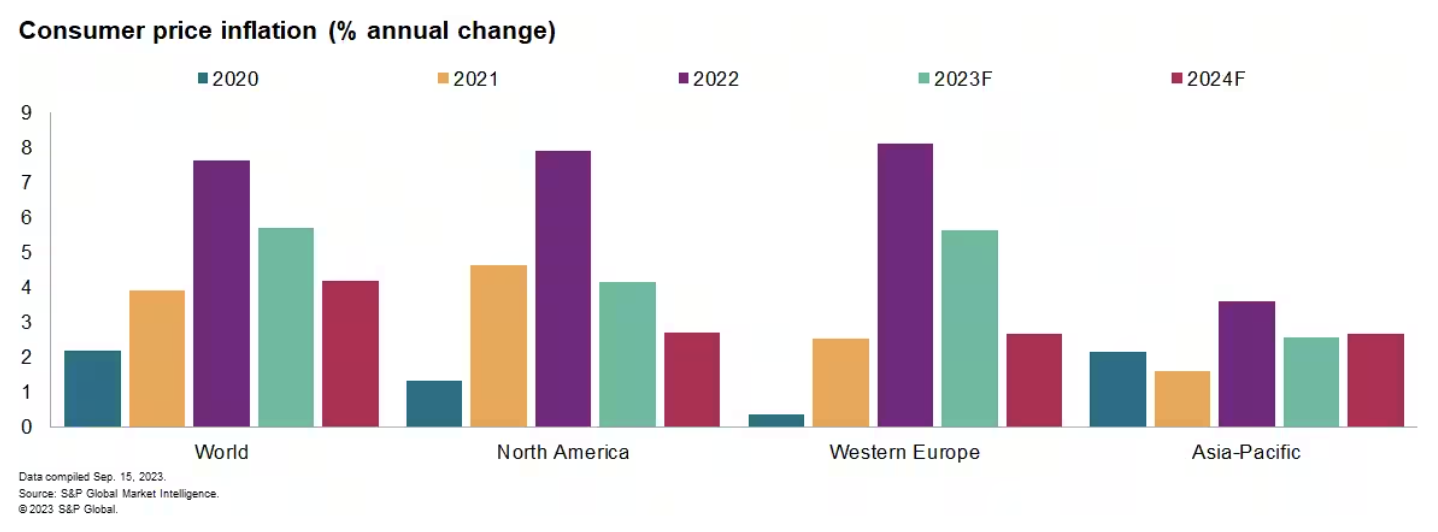

The Outlook For Inflation? It's Sticky

The near-term outlook for inflation has deteriorated. S&P Global Market Intelligence's September forecasts for global consumer price inflation have been revised higher in both 2023 and 2024. This partly reflects the impact of higher crude oil prices. The prices of some non-energy industrial commodities have also rebounded, although they remain well below the peaks of 2022. Sticky core inflation rates, particularly for services, are a prime concern given generally tight labor market conditions and elevated wage and unit labor cost growth.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

Big Banks Unperturbed By New Long-Term Debt Requirement

Banks and analysts anticipate a new regulatory proposal will only have modest impact on bottom lines even though large institutions would have to sell tens of billions of dollars of additional bonds. The rule would require banks with more than $100 billion of assets to issue long-term debt (LTD) that would be available to absorb losses in the event of failure, a standard that already applies to the eight largest and most complex banks in the US.

—Read the article from S&P Global Market Intelligence

Access more insights on capital markets >

Global Trade

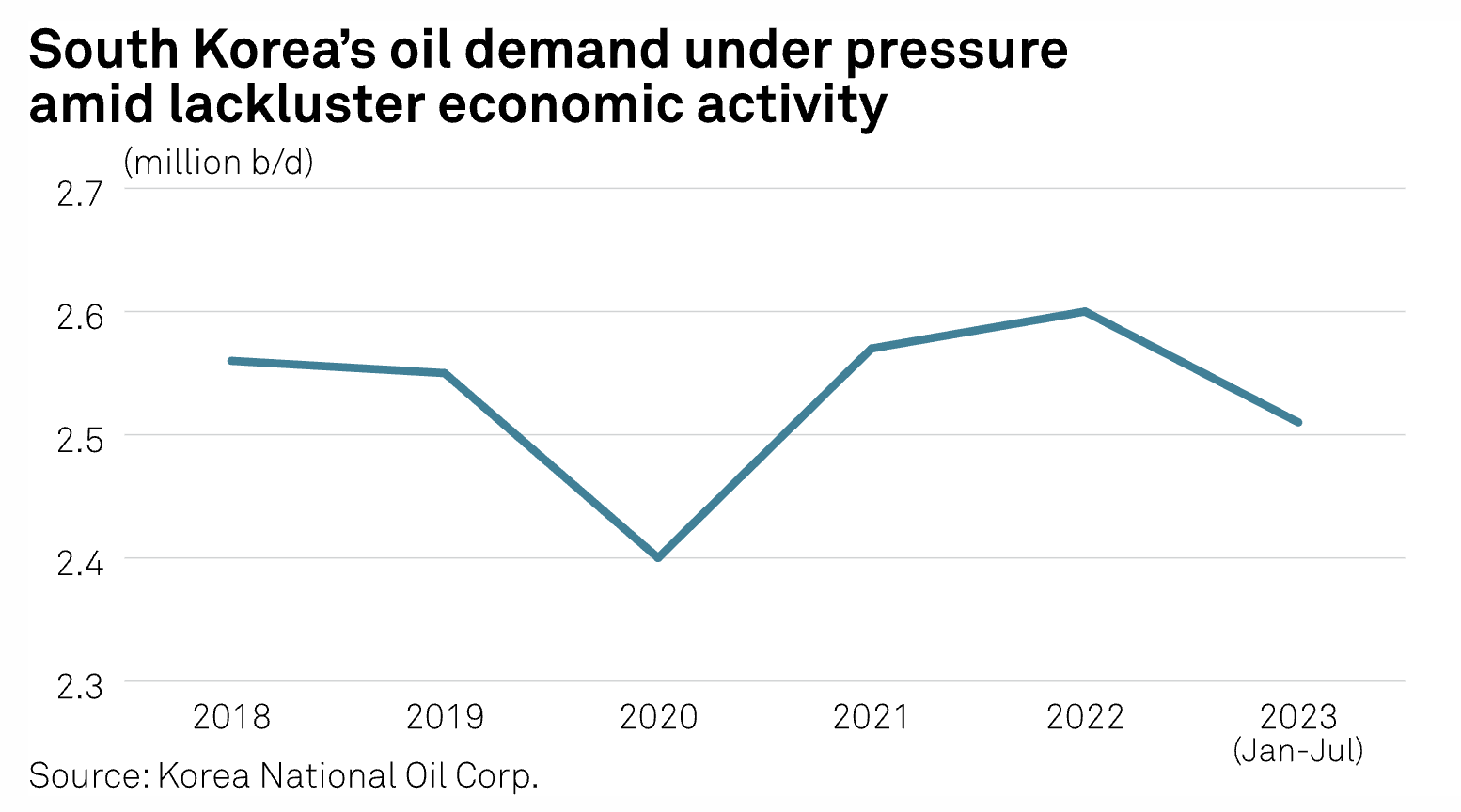

South Korea's Crude Imports Tumble To 30-Month Low In Aug Amid Lackluster Economic Activity

South Korea's crude oil imports tumbled to the lowest level in two and a half years in August as consumer spending in Asia's fourth biggest economy dwindled amid surging household debt and rising pump prices, while industrial fuel demand remained under pressure as manufacturing and construction sectors struggle, market participants said over Sept. 15-19 based on the latest customs data.

—Read the article from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

Sunak Set To Water Down UK Climate Commitments On Cars, Boilers, Home Efficiency

The UK is committed to reaching net-zero climate emissions by 2050 but it will not do so by bankrupting its hard-pressed citizens, Home Secretary Suella Braverman told BBC Radio 4 in an interview Sept. 20. Braverman was responding to reports UK Prime Minister Rishi Sunak is about to water down a range of climate policies on vehicles, gas boilers and energy efficiency in homes. "The prime minister will be setting out more detail in the coming days and I'm not going to pre-empt that, but what I support is an element of pragmatism and proportionality," Braverman said.

—Read the article from S&P Global Commodity Insights

Access more insights on sustainability >

Energy & Commodities

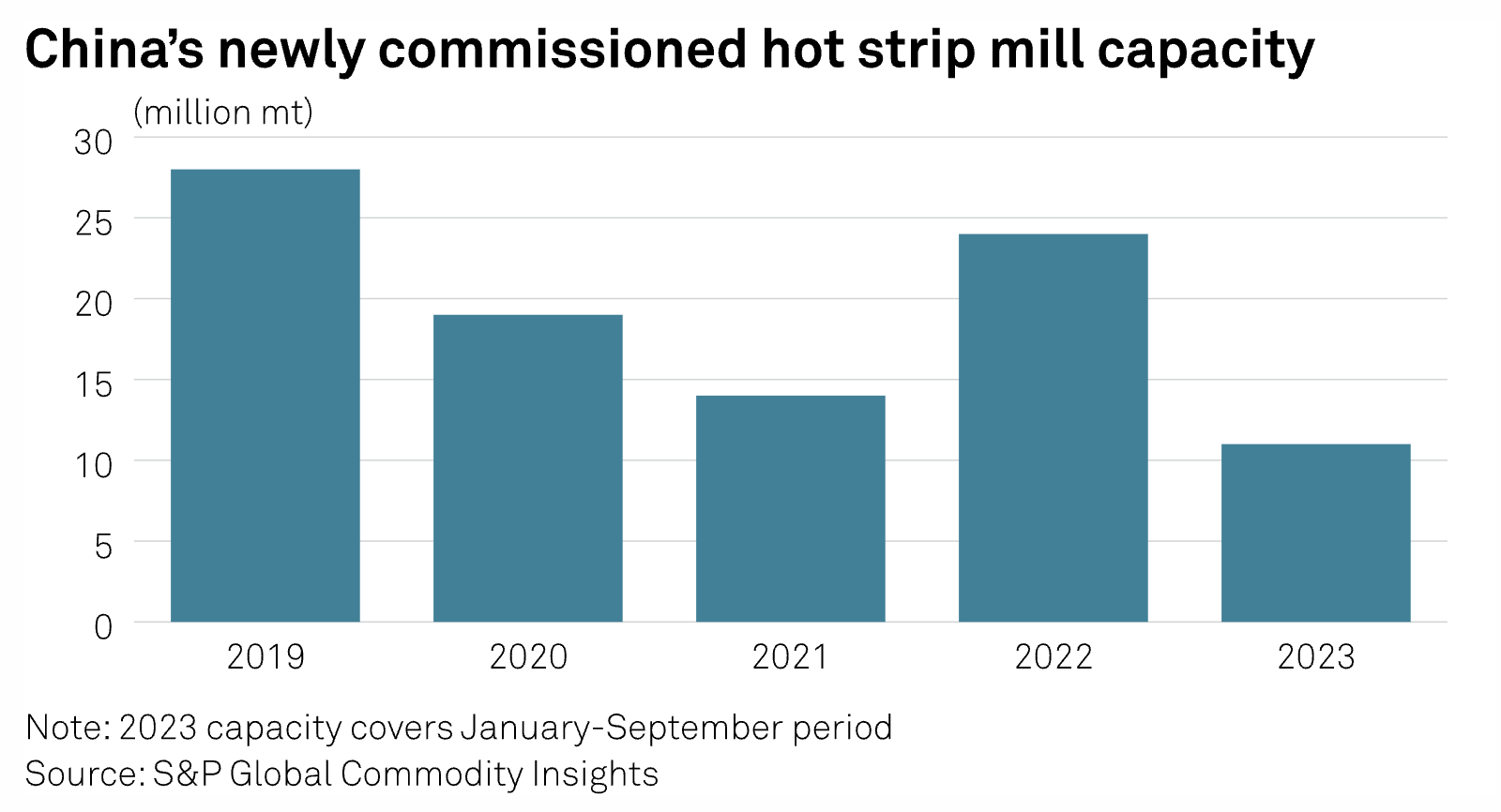

China's Rising HRC Capacity Weighs On Margins But Favors Downstream Sector

With China's shift from long steel production to flat steel continuing in 2023 amid more brand-new hot strip mills coming on stream, profit margins for hot-rolled coil face pressure, but this has lent support to the downstream sector, according to market sources. The rise in flat steel production in tandem with the capacity expansion is in line with the economy's gradual shift from the property sector to the manufacturing sector, market sources said. However, such rapid capacity growth has also weighed on flat steel prices, they added.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

Listen: Next In Tech: Ep. 133 — Digital Infrastructure Roundup

The last month has seen larger players in digital infrastructure make the case for their views on how it should be built and what’s needed to embrace generative AI. Jean Atelsek, Melanie Posey and Henry Baltazar return to the podcast to look at what was pitched at VMware Explore, Google Cloud Next and other recent industry events. Access to data is a key decision point, but many are still wrestling with cloud operating models. Fundamental questions on managing compliance concerns loom large.

—Listen and subscribe to Next in Tech, a podcast from S&P Global Market Intelligence

Content Type

Theme

Location

Language