S&P Global — 6 Jun, 2023

Daily Update: June 6, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Some Find Opportunity in Shrinking Private Credit Markets

When interest rates were low and credit was abundant, private credit markets grew rapidly. The midmarket companies that tapped private credit tended to lack the investment-grade profile of companies participating in the broadly syndicated loans market. However, creditors and debtors benefited from the tighter covenants and higher returns typical of private credit. As interest rates have climbed across the world due to persistent inflation, credit markets have contracted. While private credit has been undermined alongside public credit, there are still areas of strength. Private credit remains immensely popular with private equity firms and midmarket companies looking for capital.

Given the opaque nature of private markets, it can be challenging to compare private credit to the broadly syndicated loans market. However, a recent analysis by S&P Global provides a glimpse of private credit through the lens of credit estimates on middle-market collateralized loan obligations (CLOs) and credit ratings on business development companies (BDCs) that are issuing private debt. Of middle-market CLOs with a credit estimate, about 75% have a score of “b-” and about 10% are in the “ccc” range. Most BDCs do not have a credit rating, but many of the larger, more established BDCs do. Of the BDCs rated by S&P Global, all but one are rated BBB-. This implies that the majority of private credit would be considered speculative grade if it were rated using the same methodologies as public corporate debt.

The riskier nature of private credit has not prevented its adoption by alternative asset managers such as private equity firms. Large alternative asset managers such as Apollo Asset Management, Ares Management, Blackstone, Brookfield Asset Management, The Carlyle Group and KKR have invested roughly $1.4 trillion in credit markets, approximately doubling the allocation of 2019.

As banks have become increasingly reluctant to provide capital in the form of loans to growing companies, private equity has stepped in to provide direct loans through the private market, according to S&P Global Market Intelligence. In a squeezed market for capital, private equity has been able to command higher interest rates and stricter covenants from borrowers, including payment-in-kind loans, which allow borrowers to make payments with additional debt or equity rather than cash.

Take-private transactions funded by private credit have remained very popular even as private equity transactions have declined over the past two years. In a typical year, take-private transactions account for about 20% of private equity deals, but that share doubled to about 40% in 2023. Unlike most private credit, which involves direct lending between borrower and creditor, take-private transactions involve a consortium of lenders, including one “legacy sponsor” that holds existing private debt. Because this debt predates the current increase in interest rates, the cost of capital for the total deal can be kept lower.

Larger private equity firms have used their extensive reserves of dry powder to lend capital when capital is expensive. This has worked substantially to their advantage. According to Jonathan Gray, president and COO of Blackstone, current market conditions have created "a golden moment for private credit."

Today is Tuesday, June 6, 2023, and here is today’s essential intelligence.

Written by Nathan Hunt.

Economy

Connecting The S&P/ASX 200 To U.S. Equity Icons

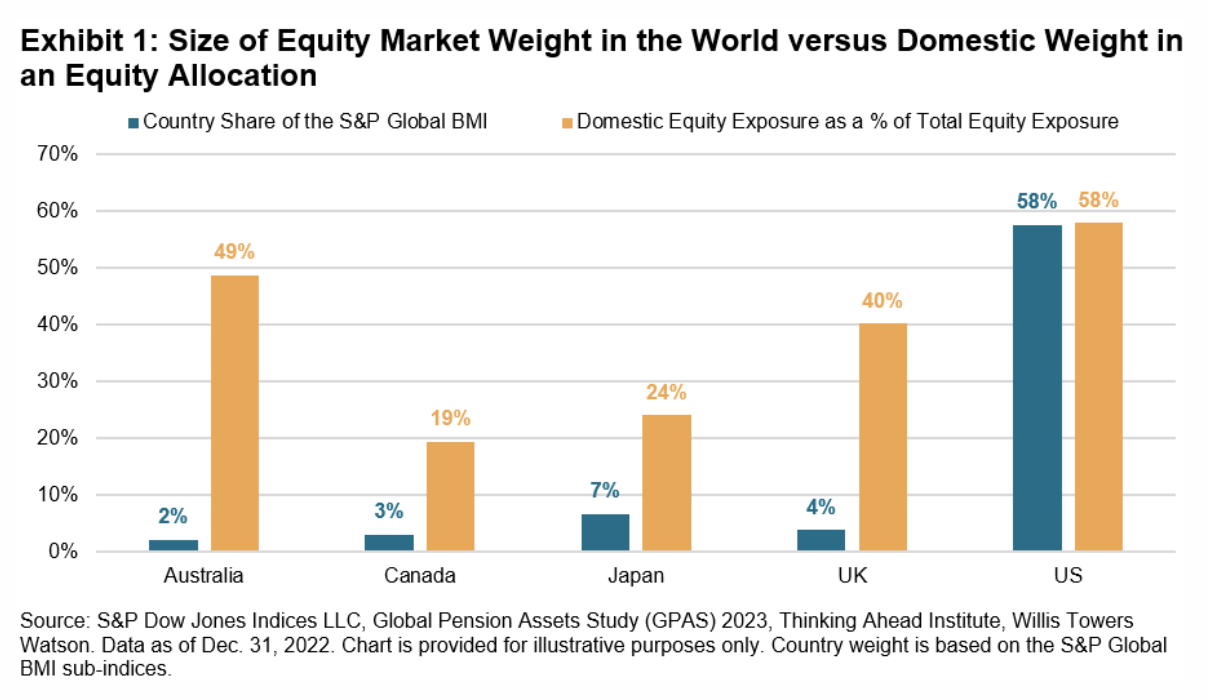

Many market participants have a “home bias,” typically having larger exposures to domestic securities than would be determined by their representation in the global opportunity set. Australia is no exception: compared to Australia’s 2% weight in the S&P Global BMI, Australian investors allocated an estimated 49% of their total equity allocation to domestic stocks at the end of 2022.

—Read the article from S&P Dow Jones Indices

Access more insights on the global economy >

Capital Markets

Stressful Conditions For US Commercial Real Estate Are Raising Refinancing Risks

The Federal Reserve's aggressive monetary policy tightening in the face of nagging inflation, combined with secular shifts in CRE (particularly in the office sector), are heightening refinancing risks for many borrowers and the strains won't likely ease any time soon. Pressures on credit quality for rated REITs and CMBS look set to persist for at least the next one to two years, as declining demand dampens rental growth and occupancy rates while borrowing costs escalate. This comes as turbulence in the banking sector further strains financing conditions, given that US banks account for the bulk of CRE lending.

—Read the report from S&P Global Ratings

Access more insights on capital markets >

Global Trade

Listen: Is The Global Price Cap On Russian Oil Sustainable?

US sanctions and export controls against Russia have centered on a dual mandate of squeezing the Kremlin's oil export revenues and ensuring the continued flow of Russian oil supplies to the global market. With that in mind, price caps were devised as a carve out for EU and G7 maritime service providers to continue aiding with the seaborne transport of Russian fuels, as long as they are sold at or below cap levels set by a coalition of countries.

—Listen and subscribe to Capitol Crude, a podcast from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

Listen: How The Aviation Sector Is Charting A Net-Zero Flight Path

The latest episode of ESG Insider is exploring how the hard-to-abate aviation sector is approaching net-zero goals. This episode brings you on-the-ground interviews from a sustainable aerospace forum hosted by Boeing and Financial Times Live that took place in Seattle on May 17. To understand what steps airlines are taking to decarbonize, hear from Lauren Riley, United Airlines chief sustainability officer and managing director of global environmental affairs. We also sit down with Alaska Airlines Senior Vice President of Public Affairs and Sustainability Diana Birkett Rakow.

—Listen and subscribe to ESG Insider, a podcast from S&P Global Sustainable1

Access more insights on sustainability >

Energy & Commodities

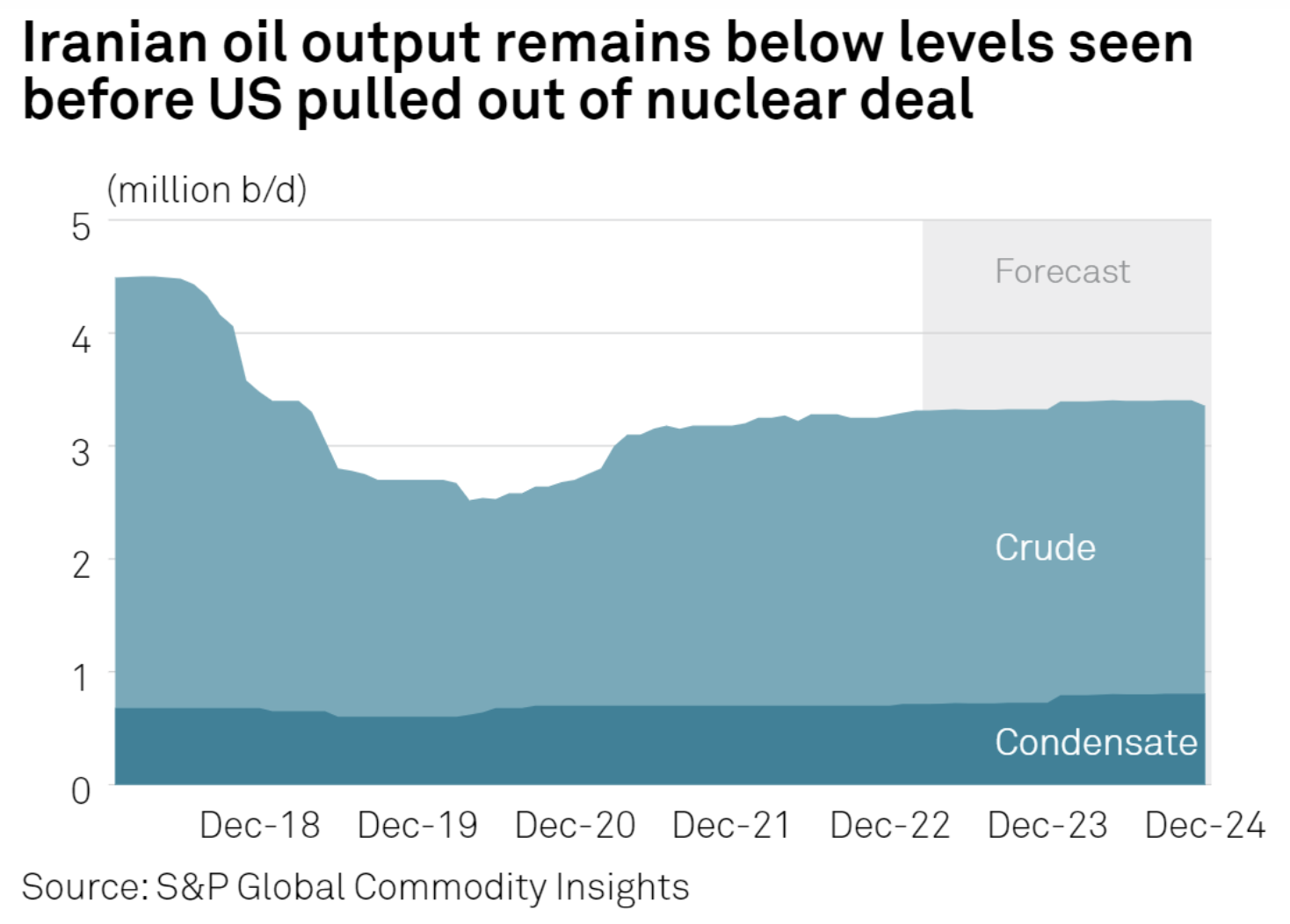

Insight From Washington: US Walks Tightrope To De-Escalate Iran’s Nuclear Progress Without Disrupting Oil Supply

US efforts to rein in Iran's nuclear program have moved out of the spotlight, but the administration of President Joe Biden continues to pursue a diplomatic solution in hopes of staving off geopolitical unrest and military conflict that would roil global oil markets and worsen the ongoing energy crisis. With Iran's crude and condensate exports topping 1 million b/d despite US sanctions, any disruption to those exports — either through tightened sanctions enforcement or factors that limit Iran's production and export capabilities — would have a bullish effect on the oil market.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

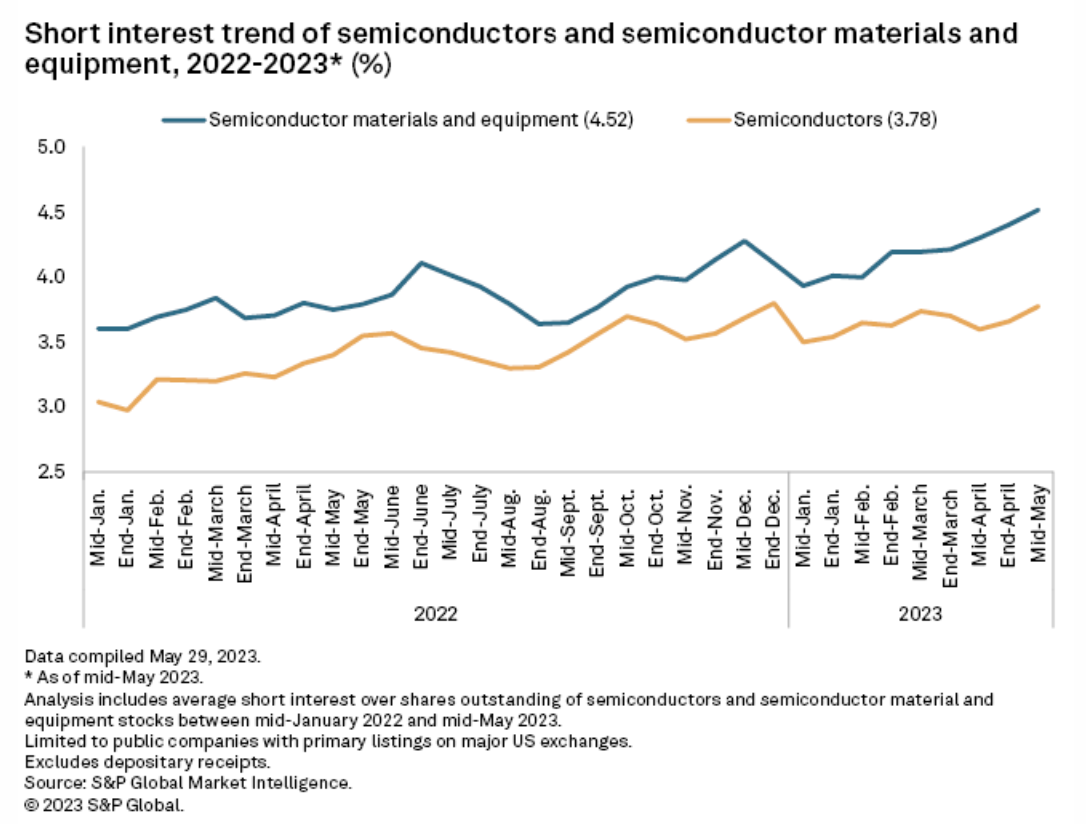

Short Sellers Boost Bets Against Semiconductor Stocks

Short sellers appear to be increasing their bets against the semiconductor industry amid a push by the US government to bolster the domestic industry and reduce America's reliance on foreign nations for these materials. As of mid-May, short interest in semiconductor materials and equipment stocks has risen 77 basis points year over year to 4.52%, according to the latest S&P Global Market Intelligence data. Short interest in semiconductor stocks was at 3.78% in mid-May, up 38 basis points in a year.

—Read the article from S&P Global Market Intelligence