16 October 2025

Auto insurance trends and emerging risks in 2026 and beyond

Article Summary

Explore how the accelerating shift toward electrification, automation, and software-defined vehicles is transforming auto insurance risk and profitability in the years ahead.

- Auto insurance trends: A market in transition

- The weight of electrification: Implications for auto insurance

- Automation and the future of autonomous vehicle insurance

- Software-defined vehicles and the next frontier of automotive insurance

- Implications for insurance industry performance

- Preparing for 2026 and beyond

A shift is underway in how vehicles are built, powered, and driven, leading to a transformation in the auto insurance landscape. Electrification, automation, and digitalization are changing not only what is on the road but how risk is modeled and priced, challenging long-standing assumptions about cost and exposure.

At our recent webinar, 2026 and Beyond: The Insurance Outlook for Electric and Autonomous Vehicles, experts from S&P Global Mobility and S&P Global Market Intelligence shed light on how these shifts connect to the evolving needs of insurers, underwriters, and investors preparing for the next decade.

Auto insurance trends: A market in transition

Vehicle automation is progressing steadily, though in a more incremental way than early forecasts suggested. The future of autonomous vehicles is no longer seen as a rapid leap to full autonomy. Instead, the market is advancing through continual enhancements to existing safety and driver-assistance systems.

Level 2 and Level 2 Plus driver-assistance technologies—where vehicles manage steering and speed but drivers remain responsible for supervision—are now the real volume drivers of automation across new-vehicle lineups worldwide. Growth in this space continues primarily under existing liability frameworks rather than through new regulation, shaping how insurers assess responsibility, exposure, and product design as automation deepens.

As automation capability expands, however, the line between assistance and autonomy continues to blur. Determining responsibility when an automated function fails is becoming more complex, particularly when both human and software inputs play a role. Questions of liability—whether attributed to the driver, the automaker, or the software provider—are emerging as defining issues for autonomous vehicle insurance.

These evolving frameworks are reshaping how insurers evaluate exposure and fault attribution, especially as higher automation levels enter commercial and fleet applications. Understanding these auto insurance trends will be essential for managing liability and pricing risk in the next era of automation.

Get a detailed breakdown in the Insurance Outlook for Electric and Autonomous Vehicles whitepaper. Download for free.

The weight of electrification: Implications for auto insurance

Electrified powertrains are contributing to a steady rise in vehicle mass. In North America, strong demand for utilities and pickups, combined with the widespread use of large-format batteries, is increasing the average weight of new vehicles across the market.

Average new-vehicle weight is projected to exceed 4,600 lb by 2026, reflecting a mix shift toward utilities and electrified drivetrains.

A heavier fleet has direct implications for auto insurance. Greater mass alters accident dynamics, raising the likelihood of more severe impacts even at lower speeds. Repair costs are also rising, particularly when high-voltage systems or integrated safety components are damaged.

At the same time, the growing presence of advanced driver-assistance systems (ADAS) that help prevent crashes is adding new cost layers. Replacing or recalibrating sensors, cameras, and radar modules can turn minor collisions into major repairs.

The result is a widening gap between frequency and severity. Crashes are less common, but when they occur, they are more expensive. Insurers will need to recalibrate assumptions about repair costs and loss ratios to maintain profitability in this high-complexity environment—especially for insurance for electric vehicles, which involves specialized components and costly repairs.

Automation and the future of autonomous vehicle insurance

Vehicle automation is progressing steadily, though in a more incremental way than early forecasts suggested. The future of autonomous vehicles is no longer seen as a rapid leap to full autonomy. Instead, the market is advancing through enhancements to existing safety and driver-assistance systems.

Taking a step back, regional dynamics reveal important differences in how these technologies are evolving. There’s a shift in focus across the supply chain — particularly toward China — as well as in the United States and Europe, which remain well-established technology markets. These differences underscore how local regulation, manufacturing ecosystems, and consumer adoption rates shape the pace of automation globally.

Level 2 and Level 2 Plus driver-assistance technologies—where vehicles manage steering and speed but drivers remain responsible for supervision—are now common across new-vehicle line-ups worldwide. Level 2+, in particular, represents the majority of current system deployment and is expanding rapidly—expected to account for roughly one-third of new-vehicle sales within the next decade. These systems are increasingly available beyond premium segments, supported by regulatory pressure for enhanced safety features.

By 2035, roughly 40% of global new-vehicle sales will feature Level 2+ to Level 4 automation, driven by OEM standardization and NCAP protocols. Levels 3 and 4 remain niche due to high cost and narrow operating domains.

As automation capability expands, however, the line between assistance and autonomy continues to blur. Determining responsibility when an automated function fails is becoming more complex, particularly when both human and software inputs play a role. Questions of liability—whether attributed to the driver, the automaker, or the software provider—are emerging as a defining issue for autonomous vehicle insurance.

These evolving frameworks are reshaping how insurers evaluate exposure and fault attribution, especially as higher automation levels enter commercial and fleet applications. Understanding these auto insurance trends will be essential for managing liability and pricing risk in the next era of automation.

Software-defined vehicles and the next frontier of automotive insurance

Electrification and automation are only part of the transformation. The next wave of change lies in software-defined vehicle design, which brings new challenges for automotive insurance providers.

Modern vehicle architectures rely on standardized hardware platforms, with most functionality controlled by software and frequently updated over the air. Capabilities such as lane-keeping, adaptive cruise control, and energy-management systems can be activated or modified after purchase.

For insurers, this introduces a new dimension of risk. Two vehicles that appear identical on paper may perform differently depending on their software configuration. This variation affects performance, safety, repair procedures, and even replacement-part compatibility.

Artificial intelligence adds further uncertainty. Algorithms that govern perception and decision-making can evolve with each software update, producing results that are difficult to replicate or predict. As vehicles become more intelligent, transparency and validation will play a greater role in risk assessment and claims handling, creating a new frontier for auto insurance risk modeling.

Implications for insurance industry performance

Auto insurance has traditionally been one of the most stable segments of the property and casualty market, but the cost dynamics of new technology are testing that stability.

Claims frequency continues to decline thanks to improved safety systems and changing driving behavior, yet severity remains high. Advanced materials, specialized labor, and supply chain constraints are driving repair costs upward. In commercial auto, litigation trends and large jury verdicts add further pressure.

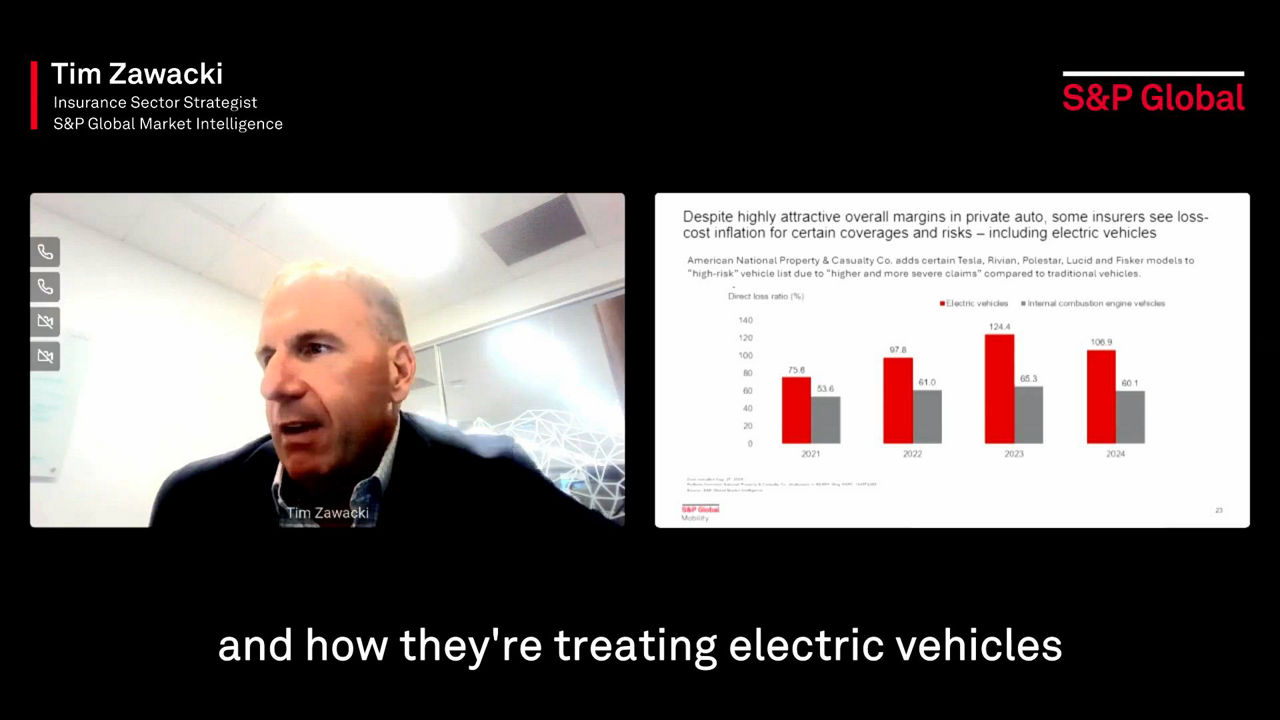

Despite strong overall margins in private auto, some insurers are experiencing higher loss-cost inflation, particularly for electric vehicles. American National Property & Casualty Co., for example, has added select Tesla, Rivian, Polestar, Lucid, and Fisker models to its “high-risk” list due to higher and more severe claims compared with traditional vehicles.

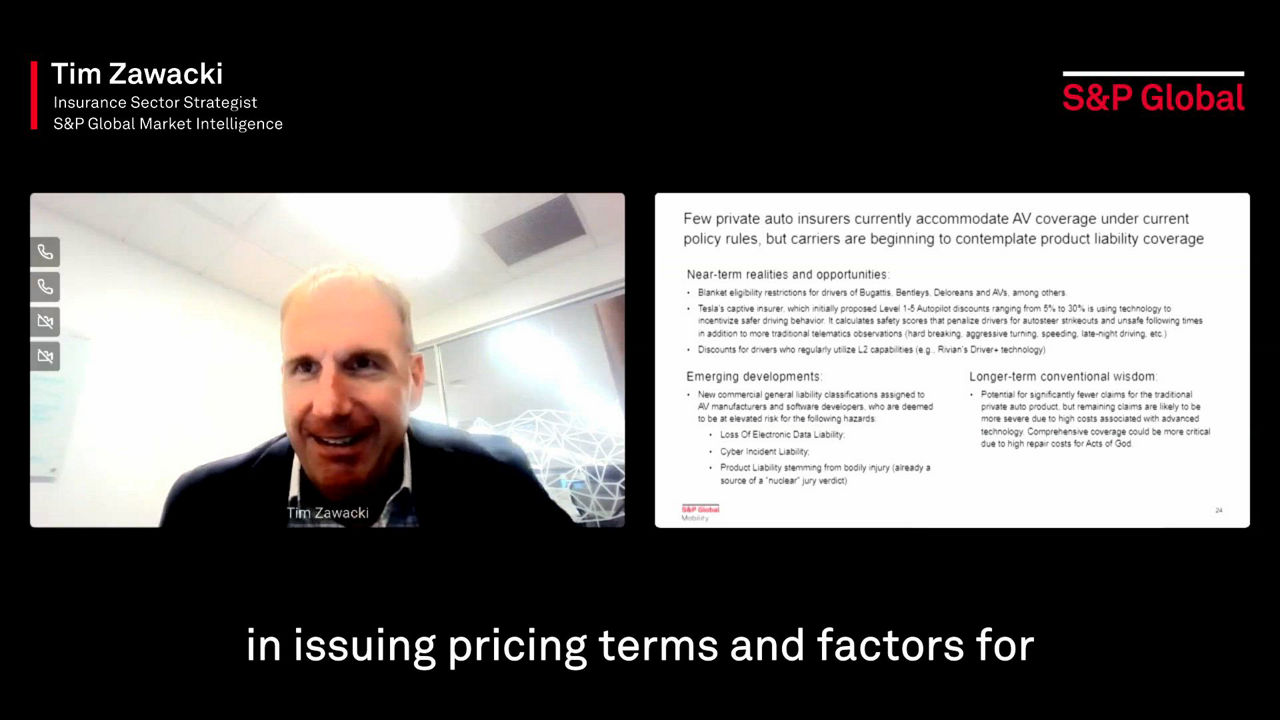

Further to this, in our recent webinar, Tim Zawacki discusses Tesla, Rivian, and GM’s entry into insurance markets and how OEM-led MGAs could redefine underwriting precision and data access:

At the same time, connectivity and telematics are creating new opportunities to refine pricing and underwriting. Real-time data on driving behavior, vehicle usage, and performance allows for more granular risk assessment. Growing partnerships between insurers, automakers, and technology providers are increasingly bridging the gap between product design and coverage.

Balancing these forces will be essential. Insurers that can adapt pricing, claims handling, and partnerships in step with technological change will be better positioned to manage volatility while maintaining long-term competitiveness. These insurance trends will define the next chapter of performance across the global insurance industry.

Preparing for 2026 and beyond

The vehicles entering the market today will shape risk exposure for the next decade. As electrified, automated, and software-defined vehicles become standard, insurers will need to evolve not just rate structures but also repair networks, claims operations, and data capabilities.

Success will depend on an ability to anticipate technological change while responding dynamically to new forms of risk. The industry’s long-term resilience will hinge on how effectively it can integrate vehicle-level insight, regulatory awareness, and operational agility.

To explore these dynamics in greater detail, with practical data solutions and insights, read our recent whitepaper. Get your free copy now.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.