S&P Dow Jones Indices — 11 Jul, 2020

A Conundrum in a Different Key

By Anu Ganti

Volatility, dispersion, and correlation are elements of what we’ve elsewhere characterized as The Active Manager’s Conundrum. Active managers should prefer:

- Low volatility, which is typically associated with higher returns

- High dispersion, which means a larger payoff for correct stock selections

- High correlation, which reduces the opportunity cost of a concentrated portfolio

The conundrum arises because low volatility, high dispersion, and high correlation almost never occur at the same time.

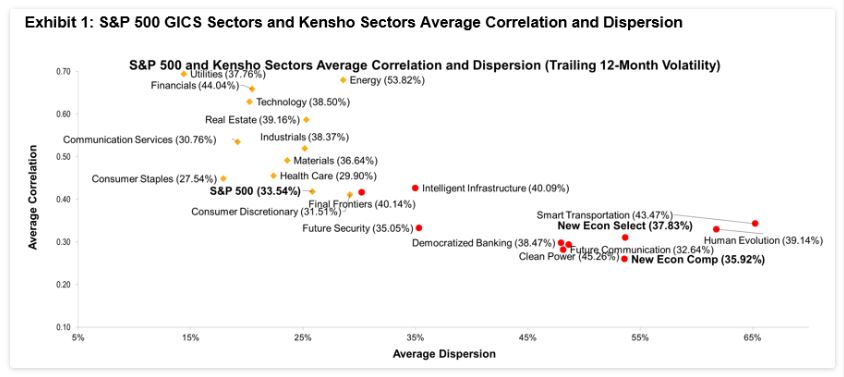

An excellent example of this conundrum lies within the Kensho New Economy Indices. From our Q2 S&P Kensho New Economies Dashboard, Exhibit 1 illustrates that the Kensho sectors have much higher dispersion levels than the traditional S&P 500 GICS sectors. Interestingly, the Kensho sectors also have much lower correlations compared to their S&P 500 counterparts, unsurprisingly given the more idiosyncratic nature of their constituents compared to those within the GICS framework.

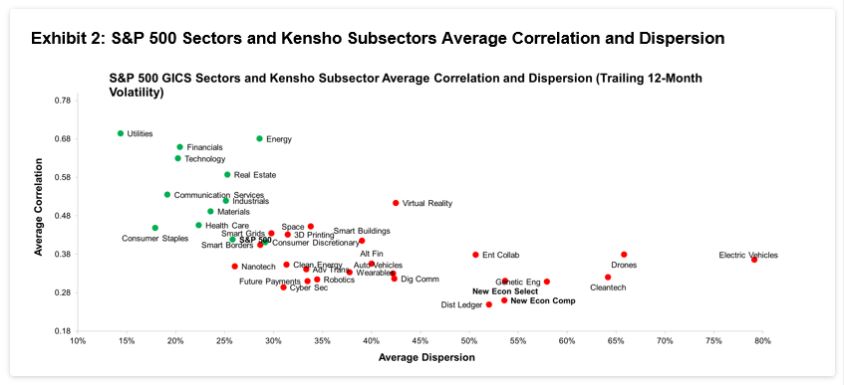

The results are even more striking in Exhibit 2, where we compare the S&P 500 GICS sectors to the Kensho subsectors, which have higher dispersion levels along with extremely low correlations.

Source: S&P Dow Jones Indices LLC. Data as of June 2020. Chart is provided for illustrative purposes.

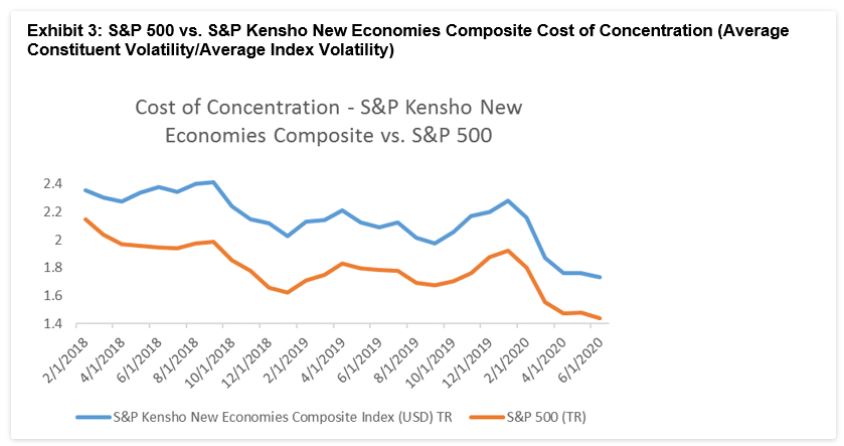

Active managers, almost by definition, run less diversified, more volatile portfolios than their index counterparts. When correlations are high, the incremental volatility associated with being less diversified and more concentrated declines. We define the cost of concentration as the ratio of the average volatility of the component assets to the volatility of a portfolio. A higher cost of concentration implies a higher hurdle for active managers to overcome.

Applying this logic to the Kensho New Economies, we would expect the cost of concentration for the S&P Kensho New Economies Composite to be higher than that of the S&P 500, as its low correlations create the possibility of less incremental portfolio volatility. We observe this to be the case in Exhibit 3, which shows that this cost is consistently higher for Kensho through time.

Source: S&P Dow Jones Indices LLC. Chart is provided for illustrative purposes.

This analysis has important implications for active management. Because of their high dispersion, there are immense opportunities for stock-pickers to add value by choosing among names in the Kensho New Economy Indices. But doing so requires active portfolios to bear a higher cost of concentration; the low correlation among the New Economies names means that stock-pickers forgo a huge diversification benefit. Investors who choose active management couple the possibility of higher returns with the certainty of higher volatility.

Content Type

Location

Language