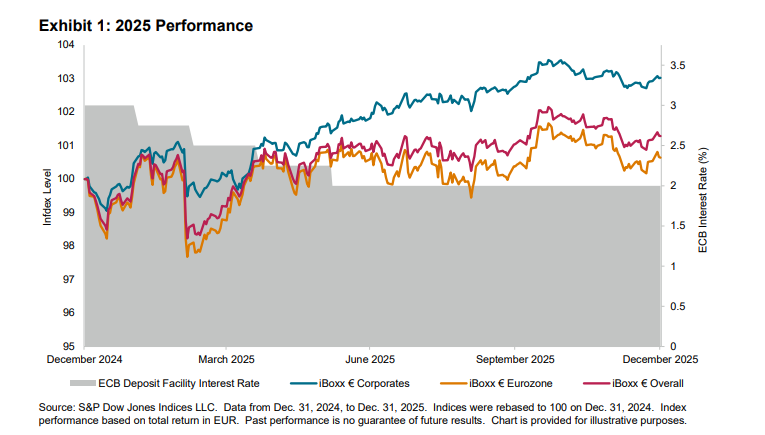

In 2025, the European Central Bank (ECB) noted signs of stabilization in economic conditions following the ratecutting cycle of 2024, with growth, labor markets and financing conditions showing greater resilience than was previously anticipated. However, the current geopolitical volatility and persistent supply chain strains underscore the broader need for stronger competitiveness and greater economic resilience across the eurozone. The ECB also warned that forwardlooking macroeconomic conditions remained highly uncertain, shaped by shifting trade policies, evolving tariffs, regulatory changes and broader geopolitical tensions, which could increase market volatility across sovereign and corporate segments.

Sovereign bonds have historically been more reactive to interest rate changes and sudden economic shifts, given their longer duration. This pattern was evident in March 2025, when the iBoxx € Eurozone declined relative to the iBoxx € Corporates following the ECB’s 25 bps policy cut from 2.75% to 2.50% in early March, as markets began pricing in fewer future rate cuts and a potential end to the easing cycle. In the second half of the year, returns were more stable, and the iBoxx € Corporates consistently outperformed the iBoxx € Eurozone. This coincided with tightening credit spreads, while sovereign bond performance was constrained by elevated eurozone fiscal deficits and greater government bond issuance as countries continued to increase their structural spending on areas such as defense. This divergence was further supported by markets pricing a higher probability of additional ECB policy easing in 2026. Over the whole year, the iBoxx € Corporates reported a 3.0% gain, outperforming the iBoxx € Eurozone by 2.4 percentage points.

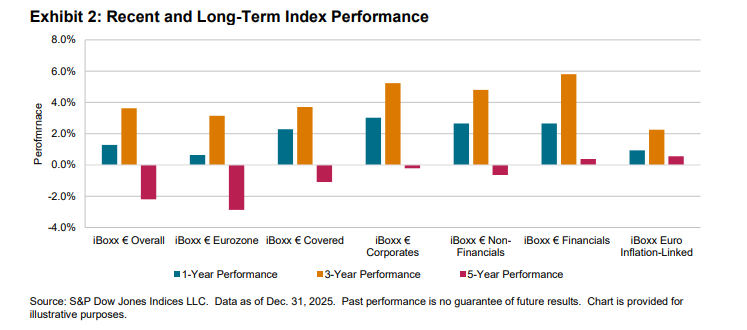

Across the iBoxx EUR Series, all headline indices delivered positive performance in 2025, ranging from 0.6% (iBoxx € Eurozone) to 3.0% (iBoxx € Corporates). The iBoxx € Corporates delivered the strongest performance, surpassing the iBoxx € Overall by 1.7% and 1.6% for the one- and three-year periods, respectively. Within the corporate space, iBoxx € Financials outperformed the iBoxx € Non-Financials across all time horizons.

Corporate bond performance benefited from tightening credit spreads and improved risk sentiment, while the iBoxx € Eurozone was held back by weaker sovereign performance amid elevated deficits and increased government bond issuance. Performance was also weighed down by sovereign rating downgrades, including France from AA to A. These factors explain the more recent outperformance of the iBoxx € Corporates, although longer‑term periods also reflect broader rate‑cycle and duration effects that have affected sovereigns.

All listed indices, excluding the iBoxx € Financials and the iBoxx Euro Inflation-Linked, posted negative five-year performance. Overall, the negative five-year performance reflects the impact of the rate‑hiking cycles over the years on duration-sensitive segments, whereas the iBoxx Euro Inflation-Linked was cushioned by the 2021-2023 inflation surge, which compensated market participants and offset the subsequent increase in real yields. Similarly, the iBoxx € Financials benefited from earlier monetary policy tightening which supported issuer profitability across the sector.