Blog — 24 Mar, 2023

Building Competitive Advantage and Avoiding Pitfalls with Credit Risk Automation

By Andrea Caruso and Karl Sees

This blog is written and published by S&P Global Market Intelligence, a division independent of S&P Global Ratings. Lowercase nomenclature is used to differentiate S&P Global Market Intelligence credit scores from the credit ratings issued by S&P Global Ratings.

In the past, only large financial institutions have ventured into deploying credit risk automation and workflow systems due to the volume of resources and investments required and the need to lock down processes. However, it is not uncommon today, to meet with a corporate credit risk officer who is looking to discuss the options, benefits, and risks of automating customer onboarding and credit risk management and monitoring processes.

Andrea Caruso, Head of Credit Analytics at S&P Global Market Intelligence, and Karl Sees, Head of CubeLogic Product Strategy at CubeLogic, discussed the risks and opportunities of Credit Risk Automation at the recent S&P Global Market Intelligence event Anticipate the Unknown - An Era of Change: Navigating Global Disruption and Credit Risk'. Here are the key take-aways from their session.

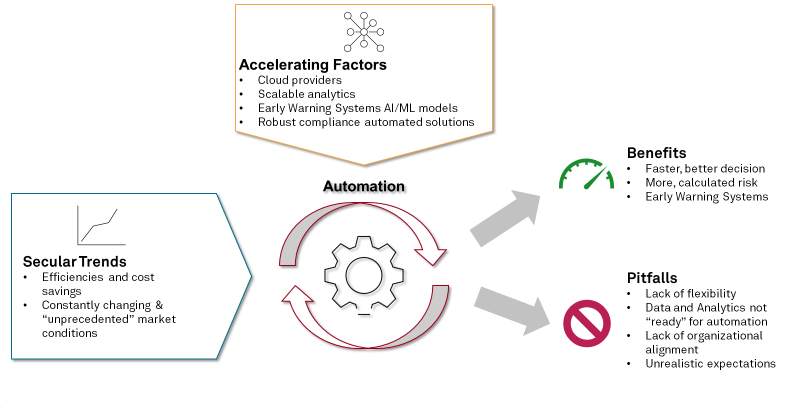

Drivers of Automation, Benefits, and Pitfalls

Source: S&P Global Market Intelligence, for illustrative purposes only.

#1 Why Automation and why now?

We have seen secular trends toward Automation driven by the quest for efficiencies and cost savings. Additionally, since the financial crisis, we have experienced constantly changing and unprecedented market conditions that have increased awareness of the need to manage credit risk effectively. Corporations might have taken too much risk – and experienced more losses than their policies or too little risk – and missed opportunities, especially during benign credit cycles.

Figure 1. FED Delinquency Rates 1985 - 2022

So why are we now observing a spike in the interest in Automation? We have observed four major trends:

- Cloud providers, such as Cubelogic, have shifted the investment from customization to configuration, offering a much more compelling ROI through the ability to identify which part of the process to automate – from one specific process, e.g., credit approval to the end-to-end customer lifecycle.

- Scalable analytics, such as Credit Analytics from S&P Global Market Intelligence, provide "out-of-the-box" credit assessment with limited or no financial information, facilitating the Automation of approval and credit limit decisions at the lower end of the exposure spectrum, where often a lot of time of credit manager is consumed with minimal returns.

- Analysis and Early Warning Systems Artificial Intelligence/ Machine Learning models leverage vast proprietary data and alternative data collected from customers through Automation, including financial, payment, and people data

- Robust compliance automated solutions are needed to cope with regulatory/audit pressure driven by increased geopolitical risk and the resulting desire for more supervision

#2 What is different about this wave of Automation?

Corporations increasingly see credit risk management as a way to increase competitive advantage and accelerate business growth, not just as something to avoid and manage. Credit departments can partner more effectively with commercial and vendor teams by speeding up credit approval, taking more risk within the corporation's policy, identifying markets with deteriorating or improving credit conditions, focusing on the riskiest and largest customers, and generating early warnings for customers and suppliers.

Finally, the pandemic followed by Russia's invasion of Ukraine produced a level of volatility and market dislocation that was both unprecedented and shocking. There was a sudden appreciation of the need to improve the speed and quality of "early warning" processes.

Better, faster decisions and early warnings are all capabilities enabled by Automation.

#3 What are the benefits and Pitfalls of Automation? Key learnings from customer integrations:

Benefits

- Limit human error through manual processing

- Easier to manage 'big data' - Deploy credit policy through business rules

- Reduced loss experience

- Reduction in costs, increase in efficiency, i.e., 150% ROI

- Regulatory importance

-

Better, faster decisions

-

IT infrastructure that scales with their business

-

Significant business process automation

-

Improved business intelligence

-

Less time spent gathering data and more time spent managing credit risks in the portfolio

A recent client case study typifies the challenges, motivations, and benefits experienced by firms embarking on a drive to automate their credit risk processes. The firm is one of the largest trading companies in the world, which, at the time, was trading 1.35 million trade legs a day with a team of credit managers overseeing a business with revenues over $115bn. Their challenges included consolidating vast data sets and timely risk reporting across multiple transaction systems, supporting complex business and credit processes, improving portfolio insights, and reducing operational risks and costs. To tackle this sizable initiative, the firm made phased changes to its overall strategic plan. Rapid and incremental improvements were executed as a result of a flexible business process and workflow solution that was able to quickly adapt to changes in the business as well as through learnings from the project itself. Significant cost savings and efficiencies were realized as a result of users being more self-reliant.

Pitfalls

- Workflow systems need to be flexible and capable of adapting as the business processes evolve. Too many firms get "locked" into legacy processes because their workflow systems are too slow and costly to change as their business model evolves. Alternatively, that fear of being "locked" into an immature process results in firms shying away from innovation and never implementing Automation.

- Data and analytics not "ready" for Automation

- Lack of organizational alignment or an organizational culture that prefers the status quo

- Unrealistic expectations of what Automation can achieve – focus on the wrong processes/outcomes

- Trying to “boil the ocean” and automate everything all at once rather than identifying high-priority processes and tackling those first

Many of these pitfalls can be avoided through careful choice of technology. Workflows that can be easily configured and quickly adapted as the organizational processes evolve. Similarly, data availability and quality are never static: solutions that include a “Data Transformation” or EDM layer enable a Firm to improve its processes and analytics as its data improves continuously.

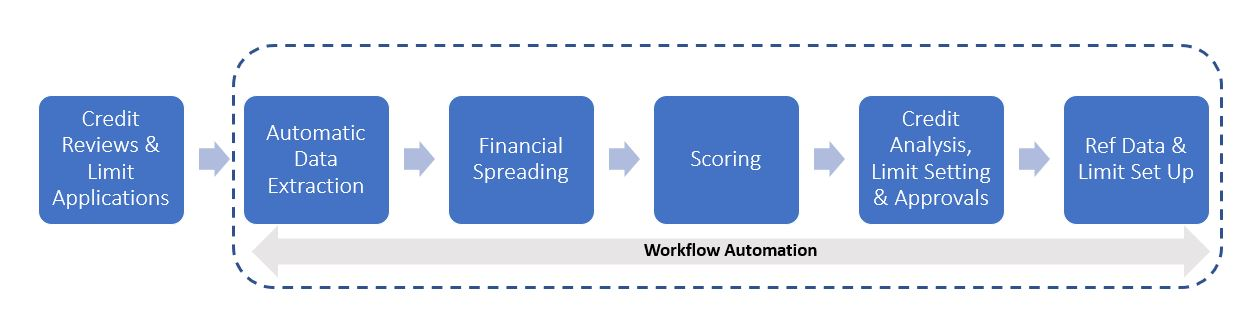

#4 What's next in Automation? The evolution.

So much has been done to ensure we have "good data", but how can you manage that more efficiently/create future-looking processes?

One example of a “future-looking” process is depicted in the Figure 2 below. It depicts a typical client onboarding and credit approval process. Rather than being performed via multiple IT systems, spreadsheets, word processing documents, etc., this workflow is executed within an end-to-end solution. An automated process like this can reduce the time it takes to onboard and approve a new client from weeks to hours/days. Not only does this reduce operating costs, but it also improves the competitiveness of the origination business by ensuring that the most attractive business does not go to faster competitors.

Figure 2. Automated Credit Risk Decisioning

Source: S&P Global Market Intelligence, for illustrative purposes only.

Early warning signals of deterioration or improvement are a big area where clients are increasingly focused. The challenge is that no single signal is sufficient for a portfolio. For a diverse multi-asset business covering public and private companies, you will need a range of signals:

- Market prices: equity, CDS, bonds

- Sentiment data

- AR Payment Experience

- Credit Ratings and credit scores for the unrated universe

- Modeled probability of default changes

#5 Where to start: Implementing Automation and progressive Automation.

Automation is not an either-or scenario. Corporations can roll out Automation in steps to maximize the benefits while solving the challenges that are hardest to tackle with a manual process.

For example, connecting the system of record with an Early Warning System/dashboard to analyze, stress, and monitor the exposure without implementing an end-to-end process.

Another approach to test Automation is to start with managed service – by outsourcing a workflow, such as onboarding while leveraging a vendor system, before "locking" the processes.

Today, credit departments can increase the competitiveness of their corporation by leveraging Automation without having to embark on large, long, and costly implementation while unlocking the value of the data collected through their customer and supplier interactions.

If you are interested in speaking with a credit specialist about Automation and Credit Risk, request a meeting here.

Theme

Products & Offerings