BLOG — Feb 22, 2022

UK economy faces a difficult start to 2022 despite the end of COVID-19 restrictions

By Raj Badiani

- Despite the end of the COVID-19 restrictions from late January, the immediate outlook for the UK economy is uncertain

- Intensifying price pressures and imminent tax hikes will erode real household incomes.

- Persistent supply chain disruptions and acute labour shortages will continue to constrain output developments

- The narrow EU-UK trade deal weighs down on UK exports to the reviving EU economy.

UK real GDP grew by 1.0% quarter on quarter (q/q) in the fourth quarter of 2021, compared with an identical rise in the previous quarter.

In annual terms, the economy rose by 6.5% year on year during the same quarter, which implied that the economy grew by 7.5% in 2021, the largest gain since the Second World War. However, this was after a 9.4% contraction in 2020, with the UK enduring a larger-than-average hit from COVID-19 and public health restrictions.

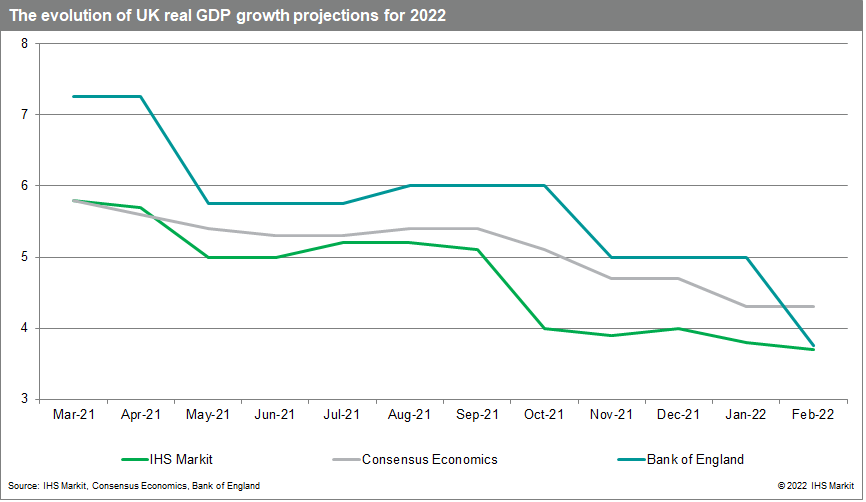

The UK outlook for 2022 is uniformly less upbeat, flagged by sliding growth projections.

Despite the end of most COVID-19 restrictions from late January 2022, we expect real GDP growth to slow in the first half of this year for the following reasons.

Many UK households face escalating cost of living pressures

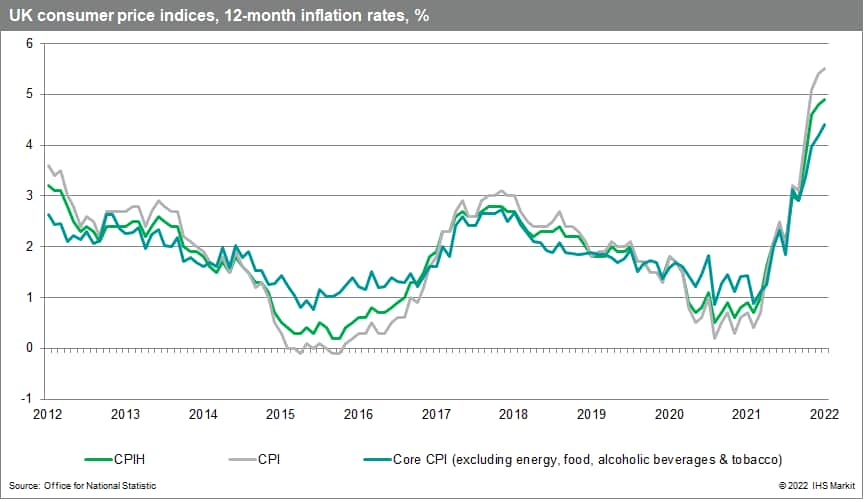

The consumer price index (CPI) in the twelve months to January increased to 5.5% in January, the highest rate since the series began in January 1997, and since March 1992 (7.1%) when using the historical-modelled data.

More inflation pain lies ahead. Elevated energy futures prices forced the UK energy regulator Ofgem, which sets the tariff caps twice a year in April and October, to announce significant hikes. The tariff cap in April this year will increase by 54%, the largest increase since the government introduced the cap in 2019. This will imply notably higher household utility prices for 22 million households from 1 April.

The eye-watering rise in utility prices will ratchet up the anticipated peak in the 12-month rate in the CPI to over 7% in April 2022. Worryingly, Ofgem is expected to announce a further sharp increase in October, pointing to a higher-than-previously-anticipated inflation rate at the end of 2022. Meanwhile, households face more challenging fiscal and monetary policy conditions.

Employees face rising social security contributions from 1 April 2022 to finance the overhaul of the social care system and to allocate more resources to deal with the backlog of non-COVID-19 illnesses. The plan entails a 1.25-percentage-point rise in the National Insurance from April 2022. Meanwhile, the continued and broad-based climb in inflation prompted the Bank of England (BoE) to announce its first back-to-back interest rate hike in seventeen years in its February 2022 meeting. Furthermore, we expect further increases at both the March and May meetings, taking the Bank Rate to 1.0%. In addition, we acknowledge the increasing probability of an additional hike to 1.25% in November 2022.

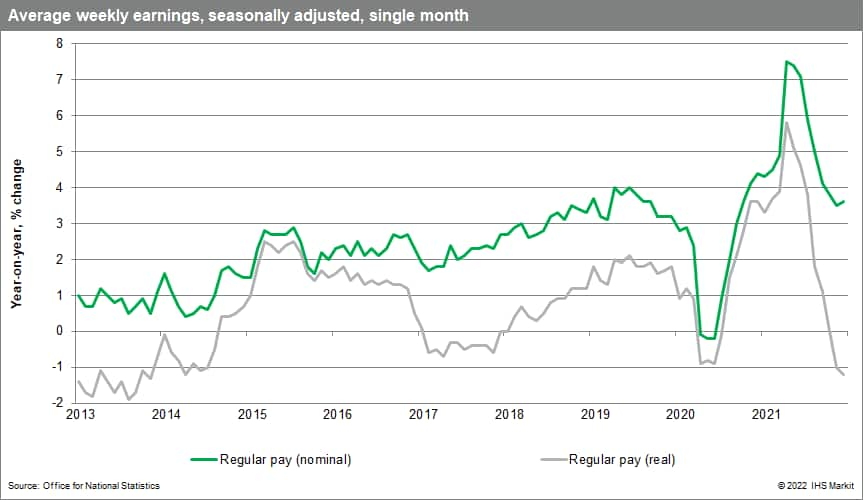

Overall, we expect an intensifying squeeze on household confidence and real incomes. Early indicators are not encouraging, with real wages in retreat from late-2021. Furthermore, we now expect household disposable income adjusted for inflation to shrink in 2022, which would be the third time that it has fallen since 1990.

In addition, a greater share of savings accumulated during the lockdowns could be required to finance spending on essential goods as opposed to consumer durables and leisure and hospitality services.

Intensifying pressure on household budgets will weigh down on consumer spending developments and act as a handbrake on the pace of GDP growth in the next few quarters.

Supply constraints spill into 2022

The IHS Markit/CIPS UK Composite PMI survey reveals a continued shortfall of workers in January, preventing many companies from achieving full capacity.

Supply chain disruptions continue to elevate input cost inflation in January, with manufacturers and service providers having to lift aggressively their prices charged.

Firms cite rising salary payments alongside higher energy and logistics costs as significant obstacles.

Brexit strikes again

With the UK leaving the EU single market and Customs Union, UK exporters face additional checks for safety and security documentation, and customs papers, implying that the new EU-UK trading relationship does not deliver frictionless trade.

This is flagged by UK exporters failing to exploit the revival of domestic demand across the EU. According to Eurostat data, UK merchandise exports to the EU in nominal terms shrunk by 13.0% during 2021, compared with US and Chinese exports to the EU rising by 14.3% y/y and 22.6% y/y, respectively, over the same period.

The much-delayed full UK custom controls on EU imports are now enforced from 1 January 2022, adding to the supply chain disruptions because of tougher logistical cs industry warned that even if UK firms get their paperwork in order, they are dependent on hundreds of thousands of small- and medium-sized (SME) exporting businesses from across the EU.

Activity is likely to regain momentum temporarily from mid-2022.

Global supply chain constraints should ease alongside receding consumer price inflation and corporate cost pressures. In addition, uncertainties linked to COVID-19 developments should diminish.

Business investment plans are lifted by temporary tax breaks, which will end in April 2023.