Research — 11 Feb, 2022

Lithium supply race heats up

By Shunyu Yao

Highlights

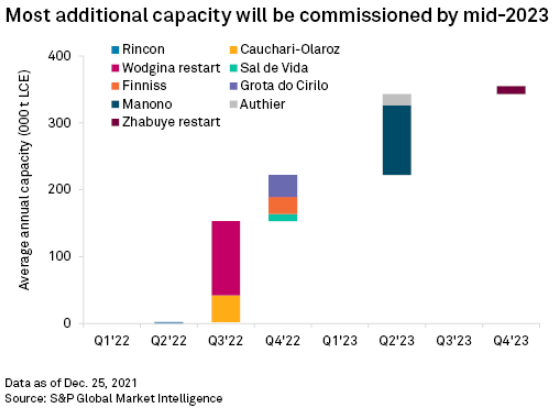

Strong lithium price momentum over the past 12 months has stimulated miners to accelerate projects amid increasing market tightness. We expect new and restarting lithium assets to add 355,000 tonnes of LCE capacity by 2023.

Spodumene projects will account for 81.8% of the capacity increase. Four new projects signed partnership agreements in 2021 to take advantage of high prices.

Commissioning of new and restart projects, as well as the expansion of existing operations, will be much needed to keep pace with unprecedented demand growth. Early production will benefit from persisting market tightness.

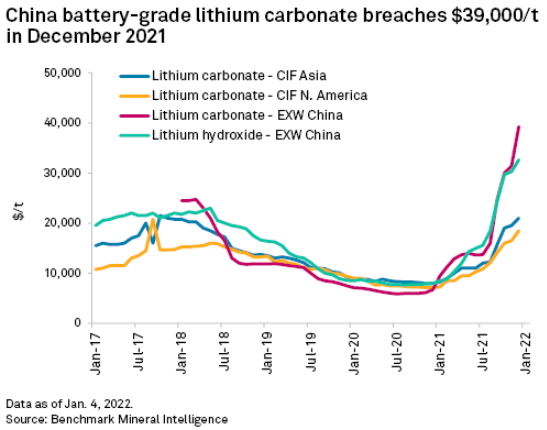

The Chinese battery-grade lithium carbonate ex-works price more than quadrupled in 2021 and has risen more than 500% from its lowest level in July 2020. Record lithium prices have been driven by strong demand from the electric vehicle market. S&P Global Market Intelligence expects a 2025 lithium price of $13,861 per tonne to stimulate lithium miners to press ahead with new projects in order to meet demand growing at a 20.0% CAGR over 2021-25. We have identified nine assets that have set the first shipment targets in 2022-23, comprising seven new projects and two restarts. These nine projects will bring around 355,000 tonnes of lithium carbonate equivalent, or LCE, capacity online by the end of 2023.

* Strong lithium price momentum over the past 12 months has stimulated miners to accelerate projects amid increasing market tightness. We expect new and restarting lithium assets to add 355,000 tonnes of LCE capacity by 2023.

* Spodumene projects will account for 81.8% of the capacity increase. Four new projects signed partnership agreements in 2021 to take advantage of high prices.

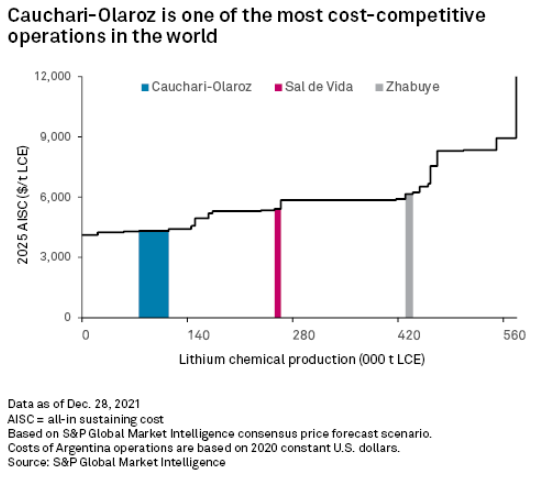

* Cauchari-Olaroz will be one of the world's most cost-competitive lithium chemical operations but will have relatively high capital requirements.

* Commissioning of new and restart projects, as well as the expansion of existing operations, will be much needed to keep pace with unprecedented demand growth. Early production will benefit from persisting market tightness.

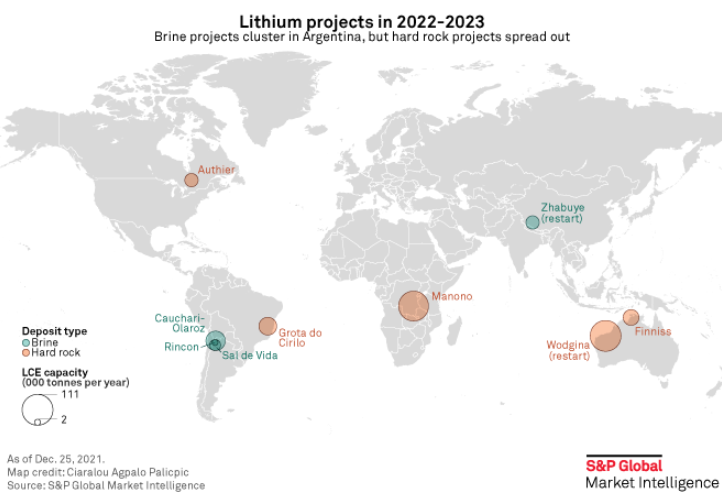

Of the nine projects, five are hard rock mines and four are brines. The hard rock mines are scattered across the world, while three of the four brines are concentrated in Argentina. The spodumene projects will account for 81.8% of the expected 355,000-tonne LCE capacity increase. The biggest spodumene project is the Albemarle Corp. and Mineral Resources Ltd. joint venture, Wodgina, in Western Australia. The project is expected to produce up to 750,000 tonnes per year of 6% spodumene concentrate, or SC6. The mine was put into care and maintenance in 2019 and aims to restart production in the third quarter of 2022. Albemarle will also manage a 50,000-t/y-capacity lithium hydroxide conversion plant in Kemerton, Western Australia, with part of the material produced from Wodgina used as feedstock. AVZ Minerals Ltd.'s Manono mine in Democratic Republic of the Congo is the largest new hard rock project penciled in for 2022-23. The mine is targeting 700,000 t/y of SC6 and 46,000 t/y of primary lithium sulfate.

AVZ expects to make the first shipment of SC6 in the second quarter of 2023 and has begun a pre-feasibility study to produce lithium hydroxide products from sulfate feedstock.

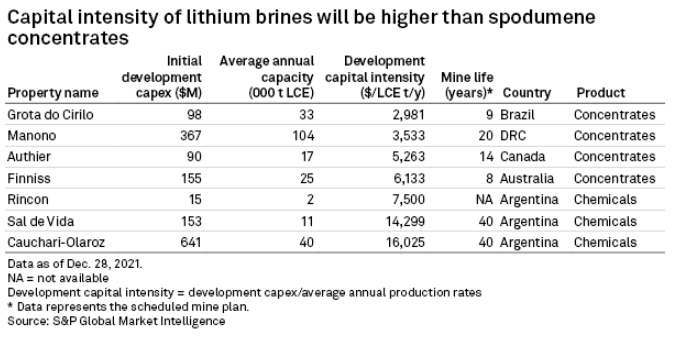

Lithium Americas Corp.'s Cauchari-Olaroz in Argentina will be the largest new brine project to be commissioned in 2022. Lithium Americas plans to kickstart stage 1 production of 40,000 t/y of battery-quality lithium carbonate by mid-2022 and to have announced additional details of the stage 2 expansion earlier in the year. Sal de Vida, Finniss and Grota do Cirilo are also exploring opportunities for potential stage 2 expansions. Argosy Minerals Ltd.'s Rincon operation is currently the smallest of the planned brine projects. It is located close to the $825 million Salar del Rincon project. Although unable to fulfill the original 10,000-t/y plan, Argosy has decided to start with a 2,000-t/y battery-grade lithium carbonate operation by mid-2022.

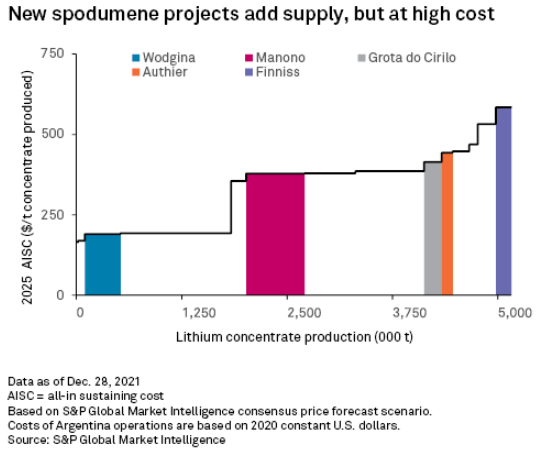

These new hard rock projects will add high-cost supply, with Grota do Cirilo, Authier, and Finniss in the upper quartile of the 2025 lithium concentrate cost curve. In previous research, we anticipated that the availability of higher margins would push concentrate producers to move forward with developing conversion facilities to produce lithium chemicals, including carbonate and hydroxide. Building a concentrate plant is nevertheless the first step. Severe market tightness is also propelling a short-term focus to accelerate time-to-market in meeting downstream refinery demand and demand from battery-makers, as they are relying on these materials to meet production plans. All four new projects signed partnership agreements in 2021 — Authier with Piedmont Lithium Inc., Manono with Yibin Tianyi Lithium Industry Co. Ltd., Finniss with Ganfeng Lithium Co. Ltd. and Grota do Cirilo with LG Energy Solution. Ltd. This has happened against a backdrop of rising prices, with the Shanghai Metals Market SC6 CIF China price exceeding $2,000/t in December 2021.

The two new brine projects with more than 10,000 t/y of LCE capacity are expected to be in the lower half of the 2025 lithium chemicals cost curve. Cauchari-Olaroz will be one of the world's most cost-competitive assets. Latin American brine assets tend to be attractively positioned in the low-cost quartile. The development capital requirements, however, will be higher for lithium brines compared with concentrate production from hard rock assets. Cauchari-Olaroz will have the highest capital intensity among the nine projects, at $16,025/t per year. Development capital of the hard rock projects will be significantly lower; Grota do Cirilo has the lowest capital intensity, at $2,981/t/y.

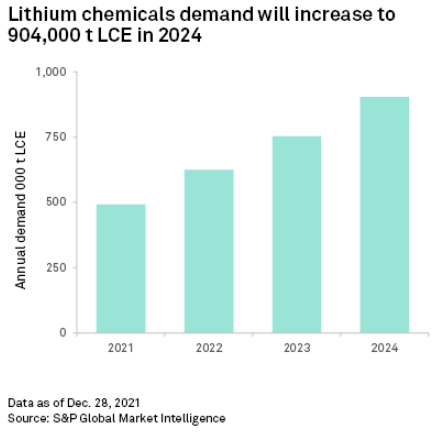

With lithium prices embarking on a new upward price cycle since 2021, lithium projects have accelerated. We expect lithium chemicals demand will rise to 904,000 tonnes of LCE in 2024 from 492,000 tonnes in 2021. While the nine assets considered here will contribute to meeting much of that demand if they successfully ramp up to full capacity, there remains room for additional development. This also implies a race to develop the projects. The earlier a project goes into production, the earlier it can gain from elevated prices due to market tightness, as the supply increases of the new projects will help ease the tightness. We expect the soaring prices could soften in the next two years as a result of these supply increases.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Products & Offerings