06 Aug 2019 | 16:46 UTC — Insight Blog

How big oil’s bet on gas turned sour: Fuel for Thought

Europe’s largest oil companies shared a common theme in their second-quarter financial reports: Shell, Total and BP all blamed tepid gas markets partly for their lackluster earnings.

Hyped as the fuel of the future, LNG has become an increasingly tricky commodity for the industry to manage. This could be because of three powerful economic forces now converging and complicating the outlook for the fuel.

Firstly, producers continue to invest billions of dollars into building new LNG projects, despite a growing glut of supply.

Secondly, climate change is prompting some consumers, perhaps for the first time, to question the fuel’s long-term green credentials.

Finally, the weakness of the global economy and increasingly unpredictable weather cycles are making fundamental drivers for seasonal demand even harder to forecast.

Despite, all these concerns, Shell – Europe’s biggest producer of LNG – is convinced its multibillion-dollar bets on the fuel’s future will pay off for investors in the long term.

“We are strong believers that LNG demand will grow by 50% by early 2030, which will require more supply to meet that demand,” said Jessica Uhl, Shell’s chief financial officer. The company reported a 25% quarterly decline in profits from its integrated gas arm, despite benefiting from having about two-thirds of its LNG deals linked to the value of oil.

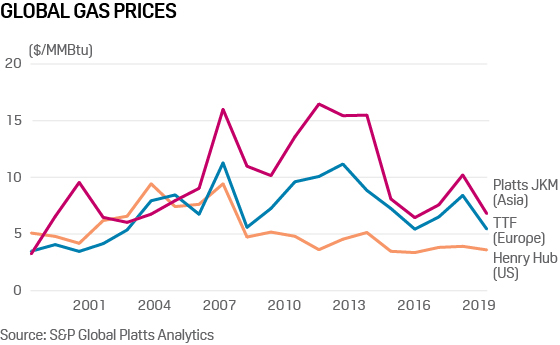

Sinking spot prices

Traditionally, the majority of the world’s LNG has been indexed to crude, with buyers and sellers locked into long-term inflexible contracts at fixed prices. However, the rapid increase in demand for the fuel in Asia and a growing oversupply has led to the creation of a bigger and more liquid spot market as more customers demand the flexibility to renegotiate.

The benchmark S&P Global Platts JKM Asian LNG spot sale price hit $4.11/MMBtu at the end of July, down from a $12/MMBtu-high in September last year.

“This is a big challenge in the LNG market right now because you have a lot of long-term contracts signed linked to oil, which are disconnected from the spot price,” said Jeff Moore, manager of Asian LNG Analytics at S&P Global Platts Analytics.

“This is creating tension in the market where you have relatively low spot prices compared to term prices. Contracts will likely need to be renegotiated or resigned on different pricing mechanisms in order to reflect a better representation of market prices as gas and oil are impacted by a different set of fundamental factors.”

More supply on the way

Despite this weakness in price, even more LNG is about to flood onto the market. Qatar – the world’s LNG superpower – has committed to increase its output of the fuel by up to a third in the next five years.

Producers in Russia, Australia and the US are all preparing to add more capacity. Many of these projects benefit from also producing more high-value petroleum liquids, known as condensates, which add to their profitability.

Go deeper: Read S&P Global Platts' special report on the future of LNG markets

“One of the main challenges we see even in a low gas price market is that there are still a lot of projects that have liquids associated with the production volumes, so they are still economic even in a low gas price environment,” Moore said.

“This will put pressure on projects that are drier and have less liquids production. This is the main difference between now and a few years ago, when we saw similar gas prices, which is that oil prices are much higher than they were in 2015 or 2016, so you have the liquids uplift.”

More-industrialized nations committing to zero emissions targets in response to climate change concerns could also hit the industry. LNG was once presented as a magic bullet for the environment and a clean energy transition, but this view could now be shifting. The UK depends on LNG for about a fifth of its gas, but still plans to phase out its domestic use in homes to meet emissions targets.

Still, Platts Analytics expects LNG demand to grow by 40% over the next decade, largely due to growth in Asia’s booming economy. However, the fuel has been caught up in America’s trade dispute with China. Beijing raised import tariffs on US shipments in May in retaliation to President Donald Trump’s trade policies. It is the kind of unpredictable event the once-stable LNG industry is learning to absorb.