To strengthen the Indonesian capital market ecosystem and increase the global competitiveness of Indonesian equity indices, S&P Dow Jones Indices (S&P DJI) and the Indonesia Stock Exchange launched a series of co-branded indices in 2025.1 As a pioneer in the dividend space, S&P DJI has a track record of creating and maintaining a wide variety of dividend indices for over 30 markets for more than 20 years. Previously, we highlighted the importance of dividends for the Indonesian market and showcased the historical outperformance of a high dividend yield strategy in a non-Shariah universe in the paper Exploring Dividend Opportunities in Indonesia. In this article, we will focus on a high dividend yield strategy that meets Shariah standards, exploring its historical performance and characteristics.

The S&P/IDX Indonesia Shariah High Dividend Index measures the performance of 30 high-dividend-yielding stocks from the S&P Indonesia BMI Shariah that comply with Indonesia Sharia Stock requirements. From Jan. 31, 2011, to Dec. 31, 2025, the index had an average trailing 12-month gross dividend yield of 4.79% and an average annual excess return of 1.92% compared with the S&P Indonesia BMI Shariah.

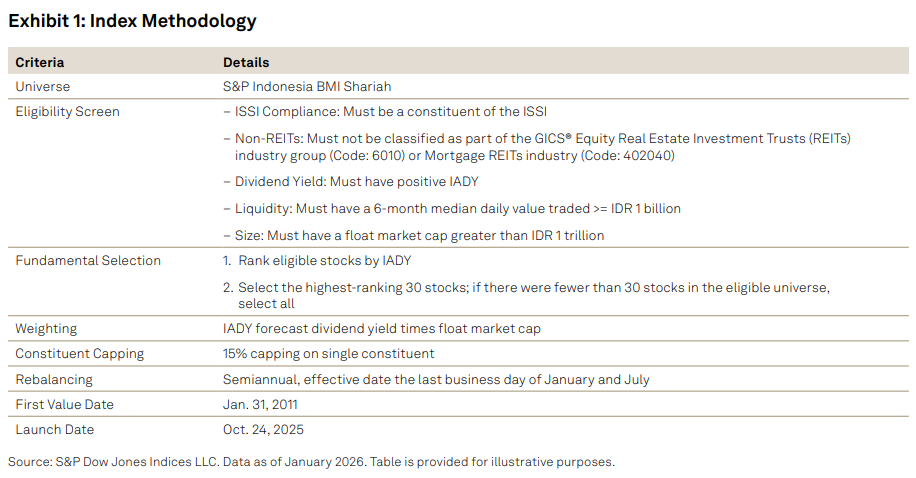

1. How Does the Index Work?

The S&P/IDX Indonesia Shariah High Dividend Index follows a transparent and rules-based methodology that is publicly available on the S&P DJI website. The index starts from non-REIT stocks from the S&P Indonesia BMI Shariah that have a positive indicated annualized dividend yield (IADY). Meanwhile, eligible stocks must meet size and liquidity requirements and must be members of the Indonesia Sharia Stock Index (ISSI). Out of this eligible universe, the 30 stocks with the highest dividend yield are selected as constituents. In the case that the count of eligible stocks is fewer than 30, all eligible stocks are selected.

The index is weighted by the product of the IADY and float market cap. Single stocks are capped at 15%. The index reconstitutes semiannually in January and July