Launched in June 2024, the iBoxx LSF USD African Sovereigns Index measures the performance of USD-denominated bonds issued by African sovereigns, from countries eligible for the Liquidity & Sustainability Facility (LSF) repo program. The co-branded index aims to support the LSF’s mission of improving both the liquidity and sustainability of African sovereign Eurobonds, leveraging the fixed income expertise of S&P Dow Jones Indices (S&P DJI).

1. What differentiates LSF sovereigns from their LatAm and APAC peers? (LSF)

Markets in 2025 reopened for African sovereigns that raised about USD 20 billion in funding, up from USD 15 billion in 2024. While 19 (minus Namibia) countries in Africa have outstanding Eurobonds, the iBoxx LSF USD African Sovereigns Index’s 13 constituents reflect the bulk of the liquid, benchmark-sized universe, and the index excludes smaller or distressed issuers like Benin, Congo, Ethiopia, Namibia, Seychelles and Zambia. This allows for a more like-for like comparison.

LSF sovereigns are differentiated by four compounding characteristics relative to their peers: a persistent spread premium that survives rating-bucket controls; a shorter duration that creates a unique credit-risk-without-rate-risk profile; a complete absence of investment grade anchor credits that limit crossover demand; and a concentrated, homogeneous high-yield universe with limited internal spread diversification. LatAm is the best example for understanding what LSF could look like with deeper market development and broader rating coverage; APAC illustrates the extreme bifurcation that can exist within a single emerging market region when high-quality and distressed issuers coexist. For APAC, LSF sovereigns could be compared with the lowest-rated APAC issuers and demonstrate similar characteristics.

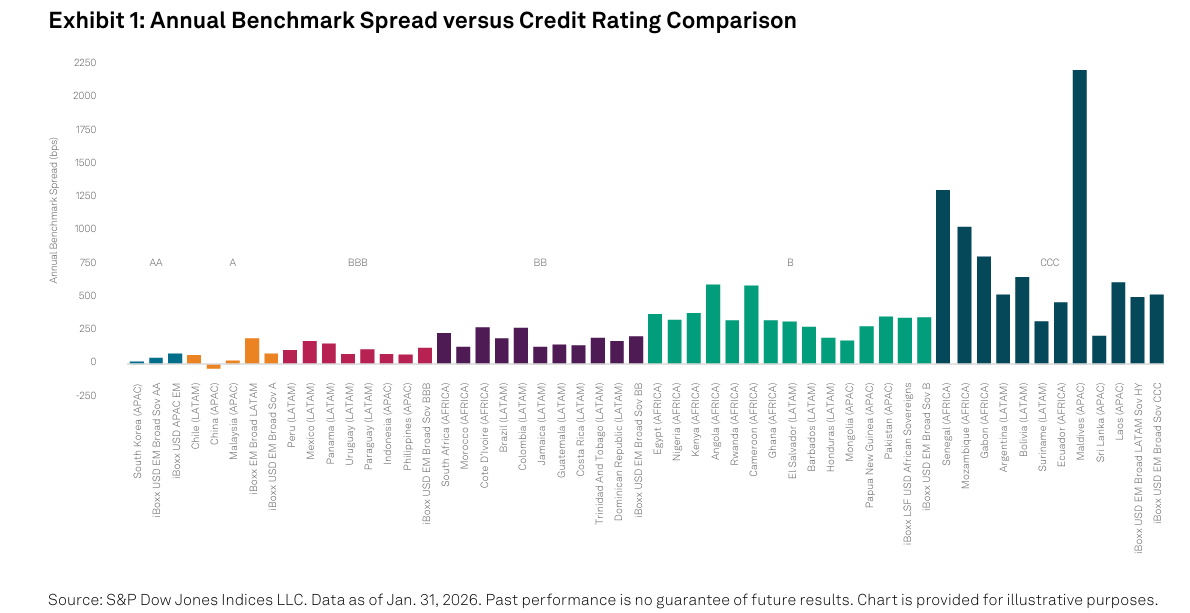

As of Jan. 31, 2026, the iBoxx LSF African Sovereigns Index traded at 346 bps, compared to 191 bps for the iBoxx Emerging Markets Broad Latin America and 77 bps for the iBoxx USD Asia-Pacific Emerging Markets. But the more analytically important finding is that this spread premium persisted even after controlling for credit rating. LSF B rated sovereigns averaged 417 bps versus 264 bps for LatAm B-rated peers and 269 bps for APAC B rated peers—a 153 bps premium that cannot be explained by rating alone. At the BB tier, the premium narrows to around 33 bps (LSF at 209 bps versus LatAm at 176 bps), but it widens dramatically at CCC, where LSF averages 1,046 bps against LatAm’s 488 bps. This persistent within-rating premium points to structural factors: thinner secondary market liquidity, a narrower and less diversified investor base, and elevated governance and political risk premiums that creditors add on as additional risk beyond/on top of the credit rating.

LSF African sovereigns average 4.6 years in duration, materially shorter than LatAm’s 6.5 years and APAC’s 6.4 years. This is not simply a function of the LSF universe being lower-rated—even LSF’s BB rated names (South Africa at 6.9 years, Morocco at 6.1 years and Côte d’Ivoire at 5.5 years) sit at the shorter end relative to comparable LatAm BB credits like Colombia (6.6 years) or Brazil (6.3 years). The short-duration characteristic of LSF sovereigns means investors are taking on credit risk with relatively limited interest rate sensitivity—the opposite of the long-duration investment grade positioning available in LatAm (Peru at 9.2 years, Uruguay at 8.9 years and Chile at 8.6 years). From a portfolio construction standpoint, LSF offers a credit risk premium with lower duration risk, which is a structurally distinct proposition compared to LatAm or APAC.

The LSF Index’s 13 sovereigns are heavily concentrated, with 54% in the B tier and the other 46% equally divided between BB and CCCs. The LSF sovereigns do not span the full credit rating universe, therefore they lack the internal diversification of spread levels and credit quality that characterizes LatAm, which spans from Argentina’s CCC at 518 bps all the way to Chile’s A at 64 bps. APAC is the most bifurcated of the three—ultra-tight investment grade names (South Korea at 16 bps and China at -36 bps) coexist with some of the most distressed credits in the emerging market universe (Maldives at 2,208 bps). By contrast, LSF’s spread range— from Morocco (129 bps) to Senegal (1,303 bps)—spans exclusively the high yield and distressed segment with no investment grade ballast. Botswana and Namibia, the only investment grade tickets, both exited the markets in 2025. The practical consequence is that LSF index metrics are more sensitive to idiosyncratic country-level events and offer less natural diversification across the credit quality spectrum. The total absence of investment grade credit from LSF means the index draws exclusively from the high yield and distressed investor universe, with no crossover demand buffer.