“Know what you own, and know why you own it.”

Peter Lynch,

Manager of the Fidelity Magellan Fund from 1977 to 1990

These words from Peter Lynch were primarily aimed at stock investors, but the advice may also be relevant for those allocating to discretionary fund managers (DFMs). The ARC™ Private Client Indices (PCI), which measure the performance of more than 375,000 private client discretionary portfolios managed by over 140 firms, provide transparency on the performance of DFMs catering to private clients.

The PCI serve as a unique set of benchmarks to evaluate the performance of an individual portfolio or the average performance of a DFM versus an appropriate peer group over a reasonable time period. Over shorter time periods, DFMs may suffer periods of relative performance variation. During these periods, it is important that investors understand the approach being followed (what they own and why they own it) in order to consider performance in the context of their stated investment objectives and time horizon.

There are certain factors affecting performance that the underlying investor might reasonably expect the DFM to manage on their behalf. These factors would include portfolio construction, tactical asset allocation and stock selection. But there are other factors that can have a material impact on performance, relative or absolute, that the DFM may not be attempting to manage. These factors are often driven by the DFM’s investment philosophy and how this philosophy is implemented. Only with a thorough understanding of the approach being employed can performance be put into context.

The starting point is to understand, at a high level, what the DFM is striving to achieve. Is the objective to outperform an index, or to simply generate the best possible risk adjusted returns? These are important questions, as the two approaches can lead to materially different results.

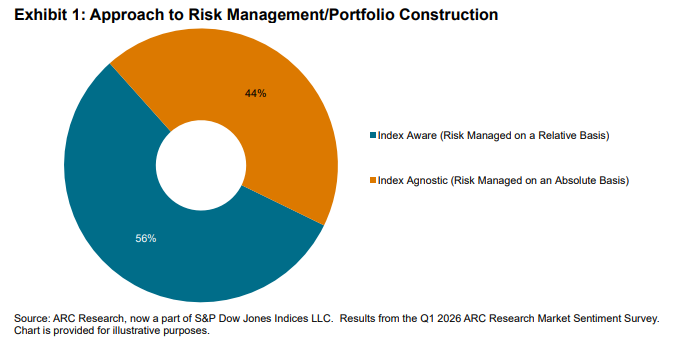

In the recent ARC Research Market Sentiment Survey (MSS) this question was put to the peer group. The results are provided in Exhibit 1.

The responses were quite evenly split, as 56% of respondents described their approach as “index aware,” the starting point being an index or benchmark, with value added through tilts away from that benchmark. The remaining 44% described their approach as “index agnostic,” meaning these DFMs aim to construct the optimal risk-adjusted portfolio without reference to an index.

Regardless of the approach, it is important for the investor to also understand the level of risk being taken by a DFM. To help with this, the PCI are categorized based on realized volatility (standard deviation of returns) relative to global equity markets. Sterling-denominated portfolios with realized volatility between 60% and 80% of global equity markets will sit in the ARC Sterling Steady Growth PCI (Steady Growth PCI).