Research — 24 Jun, 2024

APAC smartphone market through 2028: China slowdown to drag regional shipments

By Milan Ringol

Highlights

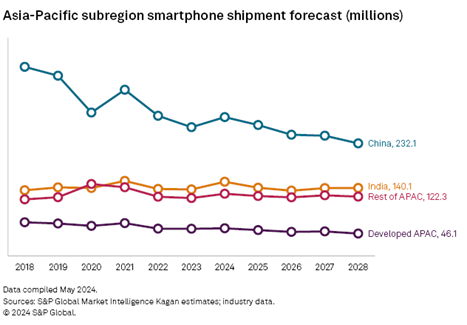

China's smartphone market is steadily slowing with shipments set to fall at a 2.7% CAGR through 2028, and its massive size, accounting for nearly half of the total installed base in Asia-Pacific, will have a strong influence on the region as a whole.

Smartphone shipments in the Asia-Pacific, by far the largest region by unit volumes, are set to decline at a CAGR of -1.3% from 2023 through 2028, sharper than the -0.8% slide we have modeled for the worldwide market over the next five years as China's slowly contracting population weighs on demand.

Kagan's global smartphone forecast is built on analysis of publicly available industry reports and proprietary data models. It provides estimates on shipments, installed base, revenue, average selling prices and replacement cycles with some regional breakouts. Kagan subdivides the Asia-Pacific region into Developed and Emerging market segments. The former includes markets such as Australia, Japan, and South Korea, while the latter is further subdivided to highlight China, India and the rest of the region.

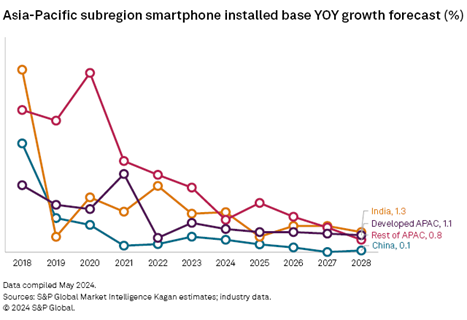

Mirroring the global trend, shipments into the Asia-Pacific region have been on a downward slope primarily due to market saturation and lengthening replacement cycles. This is most pronounced in markets across Developed Asia-Pacific, where smartphone penetration is approaching 95% in many markets and the replacement cycle is forecast to grow to almost four and a half years by 2028, according to Kagan estimates.

There remain opportunities to fill in isolated adoption gaps, especially as markets across the Asia-Pacific shut down 2G and 3G networks and make older feature phones obsolete. Simultaneously, cheap smartphones retailing for under $100 that boomed in African markets have entered markets in Emerging Asia-Pacific to make upgrading less difficult for low-income households. These factors combined impart a bit more forward momentum to smartphone shipments and installed base growth.

This mild acceleration, however, is expected to be offset by the deceleration in China as its population contracts, slowing installed base growth, and its smartphone replacement cycle extends to well over four years by 2028. China has been a core market for the rise of the smartphone in the Asia-Pacific and accounts for nearly half of the installed base in the region. Kagan forecasts China's population to steadily decline through 2028, effectively putting a damper on rapid growth in smartphone adoption with shipments forecast to decline at a 2.7% CAGR from 2023 through 2028.

As if to pick up the slack, India has become a key market in the region as well, with a large pool of untapped feature phone users and a growing population that surpassed China's at the end of 2023. With all that growth potential, Kagan forecasts India's smartphone installed base to reach 500 million units by 2028, expanding at a 1.6% CAGR from 2023, with shipments expected to grow at a 0.4% CAGR over the same period, beating the rate of growth for the region as a whole.