BLOG — Aug 28, 2023

US Weekly Economic Commentary: ‘Until the job is done’

By Ben Herzon and Lawrence Nelson

Federal Reserve Chair Jay Powell, in strong and direct language, reiterated the Fed's commitment to bring inflation down to its 2% target in his remarks to the annual monetary policy conference hosted by the Kansas City Fed at Jackson Hole, Wyoming. He concluded his speech with this quote: "We will keep at it until the job is done."

These comments came in a week that brought further evidence that growth is not cooling rapidly enough and, in Powell's words, "has come in above expectations and above its longer-run trend, and recent readings on consumer spending have been especially robust." We raised our tracking estimate of third-quarter GDP growth at the end of last week. Above-trend growth would lead to further labor-market tightening, not the easing that is widely believed necessary to complete the job of reining in inflation. Something's got to give.

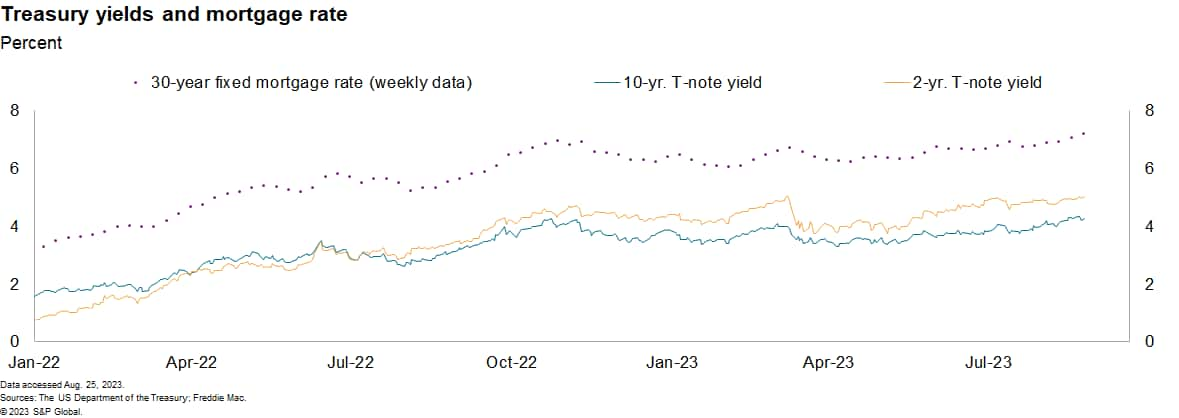

Powell noted that, "Evidence that the tightness in the labor market is no longer easing could also call for a monetary policy response." So, the risks remain tilted toward a further tightening of financial conditions. We expect another quarter-point tightening at the November policy meeting, but an earlier move at the September meeting is possible, and a further tightening cannot be ruled out. Financial markets edged in this direction this week. Financial futures have raised the odds to roughly 60% that coming out of the November policy meeting the Fed funds target range will have been raised at least 25 basis points. In recent weeks the 10-year Treasury note yield has jumped to roughly 4.25%, pushing the conventional 30-year mortgage rate to 7.23%, the highest in 22 years.

The rise in mortgage rates is definitely cooling housing markets. This is most evident in existing home sales, which are down about a third from the peak in 2022. New home construction and sales have fared better over the same period, but with construction financing costs high and rising, and mortgage rates at multi-decade highs, we expect new home construction to soften in the near-term. That will impart some drag to GDP growth. Consumer spending has surprised to the upside but higher loan rates on consumer durables, an expected slowing in employment gains, and a resumption of student loan payments constitute headwinds that we expect will slow consumer spending growth going forward.

Strength on the production side of the economy is keeping labor markets tight. Initial and continuing claims for unemployment insurance show little evidence of easing conditions. There have been improvements on the supply side of the market, as well as some evidence of softening demand. This has allowed wage gains to slow but to levels still well above a pace consistent with 2% inflation. After accounting for the uncertain lags from prior policy tightening to economic growth and inflation, it may still be likely that additional rate hikes will be necessary.

This week's economic releases:

- Consumer confidence (Aug. 29): We expect that, during August, the Conference Board Consumer Confidence Index declined 0.8 point to 116.2. While inflation has slowed somewhat in recent months, it remains uncomfortably elevated.

- Goods balance (Aug. 30): We estimate the nominal goods deficit widened by $2.7 billion in July to $91.5 billion.

- Q2 GDP (Aug. 30): We estimate second-quarter real GDP growth will be reported at 2.3% in BEA's second estimate.

- Personal income and outlays (Aug. 31): We estimate nominal personal income rose 0.3% in July, while nominal personal consumption expenditures (PCE) rose 0.7% and real PCE rose 0.5%. The estimated increase in real PCE in July would follow a solid, 0.4% increase in June and would leave real PCE on track for a healthy increase in the third quarter. We also look for a 0.2% increase in the core PCE price index in July. This would follow a like reading in June and imply a 3-month annualized increase of only 2.7%, the lowest reading since January 2021. While we believe the current underlying trend in inflation is higher than this, such a reading would nevertheless be a welcome development.

- Employment report (Sept. 1): Our view is that the US expansion is slowing, as the US labor force has been fully employed for some time now.

- Construction (Sept. 1): We estimate nominal construction spending rose 0.2% in July. This would continue a run of solid gains in recent months that has in part reflected firming construction prices but also the effects of recently authorized public infrastructure spending (from the late-2021 Infrastructure Investment and Jobs Act) and incentives for the construction of some private manufacturing structures (from the 2022 Inflation Reduction Act).

- Light vehicle sales (Sept. 1): We estimate light vehicles sold in August at an annual rate of 15.2 million units. This would be in line with averages over the last few months and materially above averages from one year ago (around 13 million). US auto manufacturers are assembling vehicles at rates in line with pre-COVID averages and are managing to build inventories at retail dealerships. This helping to prop up sales.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.