BLOG — Oct 04, 2022

US Monthly GDP Index for August 2022

By Ben Herzon and William Magee

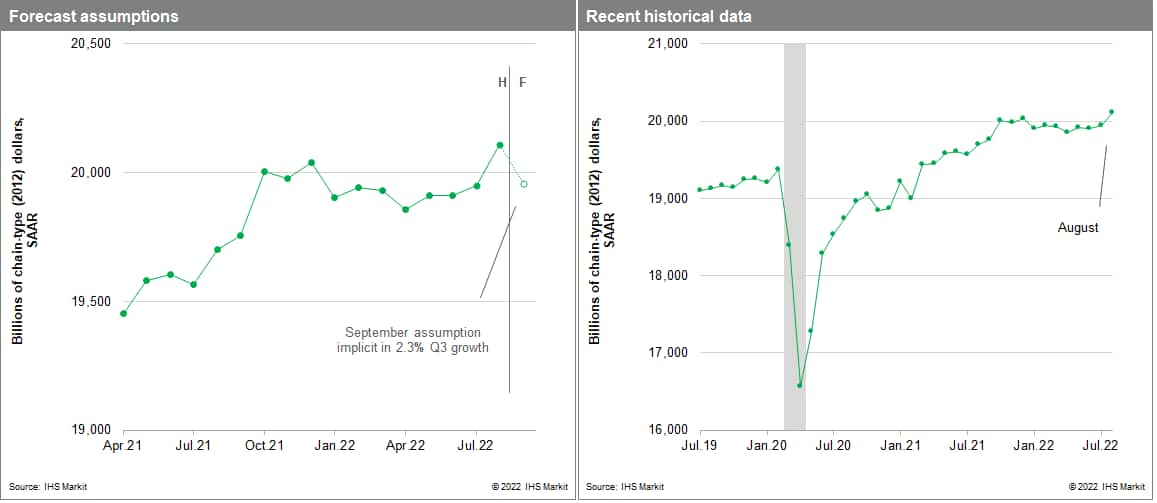

Monthly US GDP rose 0.8% in August following a 0.2% increase in July. The latter was revised lower by 0.2 percentage point. The increase in August was accounted for by large increases in nonfarm inventory investment and net exports. Final sales to domestic purchasers were essentially flat in August. The sharp gain in inventory investment in August is likely to be reversed in September, as inventories (outside of motor vehicles and parts), by our estimation, were already somewhat overbuilt heading into August. Indeed, implicit in our latest tracking forecast of 2.3% GDP growth in the third quarter is a 0.7% decline in monthly GDP in September that is mainly accounted for by such a reversal.

Our index of Monthly US GDP (MGDP) is a monthly indicator of real aggregate output that is conceptually consistent with real Gross Domestic Product (GDP) in the National Income and Product Accounts. The Monthly GDP Index is consistent with the NIPAs for two reasons: first, MGDP is calculated using much of the same underlying monthly source data that is used in the calculation of GDP. Second, the method of aggregation to arrive at MGDP is similar to that for official GDP. Growth of MGDP at the monthly frequency is determined primarily by movements in the underlying monthly source data, and growth of MGDP at the quarterly frequency is nearly identical to growth of real GDP.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.