BLOG — Jan 11, 2021

Monthly Global Trade Monitor - January 2021

2020 proved to be the worst year for global trade on record, global recovery is expected in 2021 with particularly strong growth impulse in Q2.

Main Observations

- Taking into account the first three quarters of 2020, all top economies suffered a decline in exports year-on-year (yoy) ranging from -0.9% for China up to -21.5% for Russia; this translates to a fall of -10.4% yoy for the whole top ten group; for imports, all top economies suffered a decline ranging from -2.6% for China up to -29.7% for India; the overall contraction in imports for the top ten group is equal to -10.9%

- Available monthly data for Q4 brings optimism. Overall, trends observed in the real value of exports by the top ten economies point to a gradual improvement of the situation in Q3 and Q4 of 2020 (in particular in Asia). Sharper recovery is predicted for Q1/Q2 of 2021 only

- China is the only top economy to show consistent recovery already in 2020 from June onwards; in November 2020, Chinese exports increased by 21.1% yoy

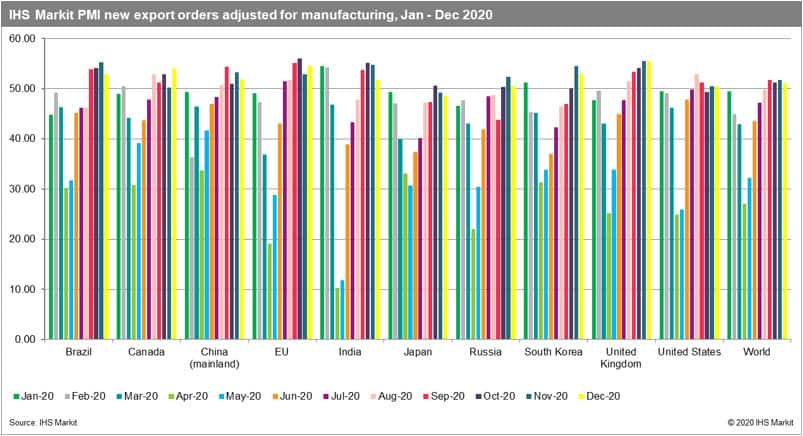

- The adjusted PMI new exports orders for manufacturing (PMI NExO) readouts for December 2020 are above 50.0 points for all the top 10 states apart from Japan and the global economy as a whole and are pointing to a recovery for the fourth month in a row

- The highest values of PMI NExO for December are reported for the UK (55.56) and the EU (54.47) which could reflect the success of talks on the UK-EU post-Brexit trade agreement - hard-Brexit scenario has not materialized after all which is clearly beneficial to both parties and for the global economy

- The optimism indicated in the PMI NExO is already reflected in the IHS Markit Commodities at Sea (CAS) statistics that offers near real-time visibility into the waterborne trade volumes of globally traded commodities and indicates positive net changes in December 2020 for most of commodities

- The new release of the GTA Forecasting model showed that global merchandise trade went down in 2020 to USD 16,382 billion or -13.5% yoy; we predict a year-on-year increase in the real value of global trade by 7.6% in 2021 and 5.2% in 2022

- We expect the global trade volume in 2020 to go down to 12.7 billion metric tons and to increase to 13.6 billion metric tons in 2021. Thus, we expect a decrease of approx. 11.2% in the global volume of trade in 2020 and the recovery in the forthcoming years with growth rates of 7.5% in 2021 and 4.1% in 2022

Changes in Trade of the Top Ten Economies

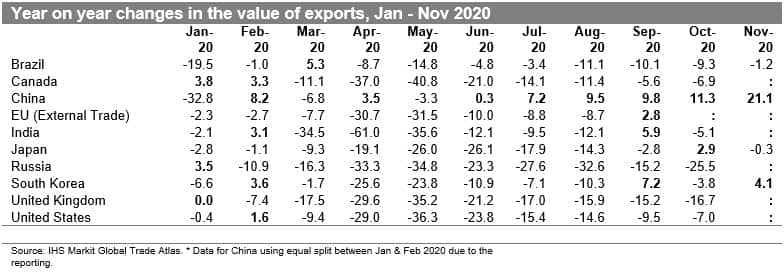

- In the first quarter of 2020, all top ten economies reported a yoy decrease in the value of exports ranging from -1.8% for Canada and South Korea to -12.8% and -13.4% for China

- The situation in the Q2 deteriorated rapidly in all the top 10 states apart from China (+0.1% yoy); the yoy changes in the remaining economies varied from -9.6% for Brazil to -36.5% for India; April and May 2020 proved to be particularly difficult which was related to extraordinary measures taken by states to limit the impact of the first wave of COVID-19

- Q3 2020 brought an improvement in exports of all the top ten economies, nonetheless, China was the only economy to report a yoy increase in their value (+8.8%); the change in the remaining economies varied from -3.4% in the case of South Korea and -4.9% in the case of EU external trade up to -25.0% in the case of Russia

- Taking the three-quarters Q1-Q3 2020 into account, all top economies suffered a decline in exports ranging from -0.9% for China up to -21.5% for Russia - a fall of -10.4% yoy for the whole top ten group

- All economies apart from the EU have already reported the data for October 2020; the readouts vary from -25.5% in the case of Russia and -16.7% yoy in the UK to -3.8% for South Korea, only two economies reported yoy increase in the value of exports, namely China (+11.3%) and Japan (+2.9%)

- In November 2020, Chinese exports increased by 21.1% yoy and South Korean by 4.1%, the values were negative in the case of Japan (-0.3%) and Brazil (-1.2%)

- China is the only top ten economy to report a positive and accelerating trend and thus a sustained recovery in exports starting from June 2020;the only countries to report a yoy increase in one or two months since the beginning of the COVID-19 pandemic are from East or South Asia, thus it seems that this part of the world is the origin of the recovery

- Trends observed in the real value of exports for the top ten economies point to a gradual improvement in the situation in Q3 and Q4 2020. Sharper recovery is however predicted for Q1/Q2 of 2021 and will depend on the dynamic of the pandemics (possible third wave) as well as steps and measures adopted by individual states

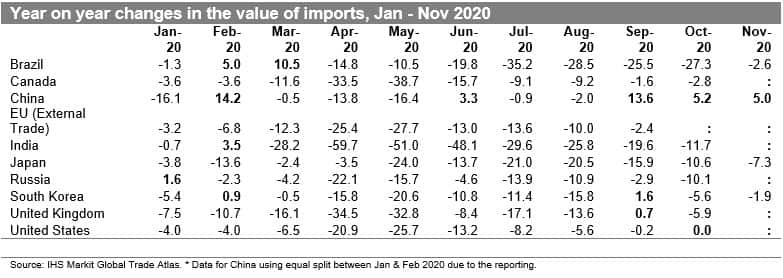

- In Q1 of 2020 only one of the top ten economies showed an increase in the value of imports - Brazil (+4.3%), the remaining economies showed decreases ranging from -1.8% in South Korea and Russia up to 11.6% in the case of the UK

- Similarly to exports, Q2 proved to be catastrophic - the yoy decrease ranged from -9.3% in the case of China up to -52.9% in the case of India (with a fall larger than by 20% in the case of the US, the EU, the UK, and Canada)

- The situation in Q3 improved in all the states, apart from Brazil (-29.9% yoy); China was the only economy to report a yoy increase in the value of imports by +3.6%; the yoy decreases were also significant in the case of Japan (-19.1% ) and India (-25.1%)

- Taking into account the first three quarters of 2020, all economies suffered a decline in imports yoy ranging from -2.6% for China up to -29.7% for India; the overall contraction for the top ten group is equal to -10.9%

- The readouts for October 2020 show an increase only in the case of China (+5.2%). The value of US imports was equal to their 2019 values for the first month in the year (with a clear upward trend from May 2020 onwards). The worst situation was reported for Brazil - 27.3% yoy, interestingly the situation deteriorated in South Korea (similarly to exports).

- The data for November is available for a limited number of countries; the data shows a yoy increase of +5.0% in China (the recovery, in this case, seems to be sustainable with yoy increase shown the third month in a row); for the remaining economies it's negative and ranges from -1.9% for South Korea, through -2.6% for Brazil to -7.3% for Japan

- The weaker results for imports could be indicative of lower consumer confidence with some planned purchases being postponed or canceled completely which could weaken the expected recovery; the incoming data for December 2020 are likely to show the first results of strengthening confidence due to the introduction of the first mass vaccination programs in the most advanced economies of the world

Prospects for the Forthcoming Months

- The reaction in trade in 2020 was consistent with the escalating global COVID-19 pandemic and steps taken by individual countries/territories in controlling or mitigating it. The situation in 2021 is likely to be similar and the substantial change dependent on the success of mass vaccination programs. The cumulative number of confirmed cases of COVID-19 globally in 2020 reached 79.2 million and 1.75 million deaths (WHO Weekly epidemiological update from 27 December 2020); The worst affected regions from the global perspective are the Americas, Europe, and South-East Asia

- On a positive note, the UK-EU trade agreement, negotiated and ratified in the last possible moment, took effect from 23:00 GMT on 31 December 2020; thus potential hard-Brexit did not materialize - the outcome will be beneficial to both the UK and EU27

- The adjusted manufacturing PMI new exports orders for manufacturing (PMI NExO) readouts for December 2020 are above the benchmark value of 50.0 points for all the top ten states apart from Japan and are pointing to a global recovery for the fourth month in a row. The value of the index for global manufacturing now stands at 51.10

- The highest values for December are reported for the UK (55.56) and the EU (54.47) which could reflect the success of talks on the UK-EU post-Brexit trade agreement

- The PMI NExO readouts for manufacturing point to optimism for the forthcoming months - first quarter of 2021

- In comparison to November readouts, we have to note a significant increase for Canada, EU, and the UK, the index has fallen in all other states (India and Brazil in particular) and the world as a whole

- The trend in the PMI NExO is clear and consistent showing a gradual improvement in market confidence from May 2020 onwards

- The most recent real GDP growth forecasts from IHS Markit Comparative World Overview (published on 15 December 2020) once again point to a recession in most of the top economies throughout 2020 and Q1 of 2021, apart from China (recovery already in Q2 2020).

- According to our new estimates growth in real GDP for the world as a whole was equal to -1.76% yoy for Q3 and -1.70% for Q4 of 2020, with a forecasted rebound in Q1 2021 to + 2.90% and a very strong growth impulse of +9.24% in Q2 2021.

- Growth impulse will be particularly strong in China in Q1 2021 followed by a recovery in other top economies in Q2 2021 which is forecasted to be particularly strong in India, the UK, Canada, and the EU, and the most moderate in South Korea and Russia

The predictions of the GTA Forecasting model for 2021 and forward

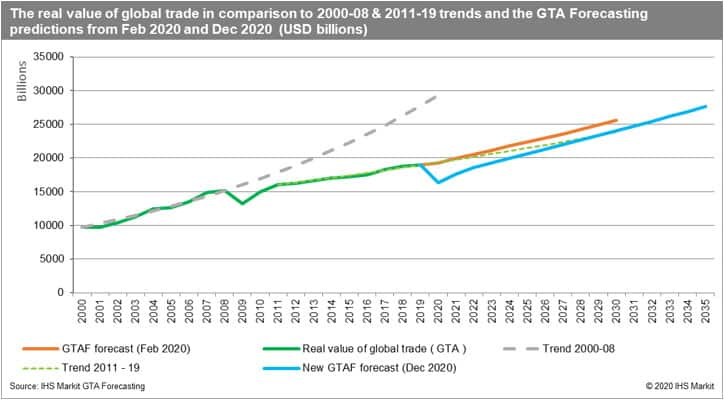

- The new release of the GTA Forecasting model from December 2020 accommodated the most recent macroeconomic forecasts of the IHS Markit Global Link Model, the actual data for the first two quarters of 2020 from the Global Trade Atlas for all monthly reporting states, and updated COVID-response factors. Please note that it covers all trading partners and thus is not restricted to the top ten economies of the world.

- The GTA Forecasting model shows that global merchandise trade went down in 2020 to USD 16,382 billion or -13.5% yoy (it represents a slight downward adjustment from the values predicted in the last release - USD 16,672 billion or by 12.2% yoy).

- Our estimated contraction in global trade value for the entire 2020 is close to the results reported by the OECD and IMF and close to the estimated optimistic scenario of the WTO from April 2020.

- We predict a yoy increase in the real value of global trade of 7.6% in 2021 and 5.2% in 2022. This accommodates the forecasted recovery in global GDP and particularly strong growth impulse in Q2.

- The predicted CAGR for the period 2021-2030 equals 3.5%

- In terms of volumes, we expect global trade in 2020 to contract to 12.7 billion metric tons and to grow to 13.65 billion metric tons in 2021 and 14.2 billion metric tons in the following year. Thus, after a decrease of approx. 11.2% in the global volume of trade in 2020, we predict a recovery in the forthcoming years with growth rates of 7.5% in 2021 and 4.1% in 2022. This will allow global transport to regain momentum and to recoup some of the losses from the trade collapse of 2020

- The forecasted CAGR for global trade volume stands now at 3.2% in the period 2021-30. For comparison, the CAGR averaged 3.6% in the period 2000-19 and an impressive 5.6% in the period 2000-08 preceding the global financial crisis. The CAGR for the period 2011-19 was 2.1% (please note that global trade volume declined in 2019 by 0.4% already)

- Furthermore, the forecasted fall in global trade volume in 2020 (-11.2%) is higher than the fall in 2009 (-7.7%) thus the adverse impact of COVID-19 on global trade volume is larger than the impact of the global financial crisis.

- The forecasted average growth rate for the period 2021-30 is above the average for the period 2011-19 but significantly below the growth path of global trade volume preceding the global financial crisis

- In general, our forecast is close to the "optimistic" scenario (shallower contraction) for the development of world merchandise trade published by the World Trade Organization in April 2020. Please note that the plunge in trade in 2020 in terms of real value puts the global economy at roughly 2011 levels. The overall fall in global trade is the largest on record with the worst quarter clearly being Q2 2020.

- The expected recovery can be strong enough to bring trade close to its pre-pandemic trend (2011-2019) but only around 2029.

- The forecasts should be treated with a large degree of caution. Several scenarios are still possible. Economic developments will critically depend on the shape of the pandemic curve and the severity of containment efforts taken globally and by individual states. The recent analysis performed by the GTA Forecasting team showed that COVID-19 impacted bilateral trade flows adversely and in a statistically significant manner. This effect on global trade endures from March 2020 onwards

This column is based on data from IHS Markit Maritime & Trade Global Trade Atlas (GTA) & GTA Forecasting.

The full version of this article is available on the Connect platform for IHS Markit clients with subscription to GTA/GTA Forecasting.

Subscribe to our monthly newsletter and stay up-to-date with our latest analytics