BLOG — Jan 25, 2021

The impact of lower population and labor force projections on economic forecasts

When considering sources of uncertainty in economic forecasts, population projections are usually not the first things that come to mind. IHS Markit economists and other forecasters typically rely on projections of population trends from the US Bureau of the Census, the United Nations, and other official statistical sources. Because historically they have been subject to slow changes, demographic projections have been updated regularly, but not frequently—normally every three years for the United States.

Unfortunately, owing to a series of events and developments during the past decade—the global financial crisis, the opioid crisis, restrictive immigration policies, and the COVID-19 pandemic—recent population and labor force projections have been too high. Specifically:

- Assumed death rates have been too low,

- Anticipated birth rates have been too high, and

- Expected immigration rates have been too high.

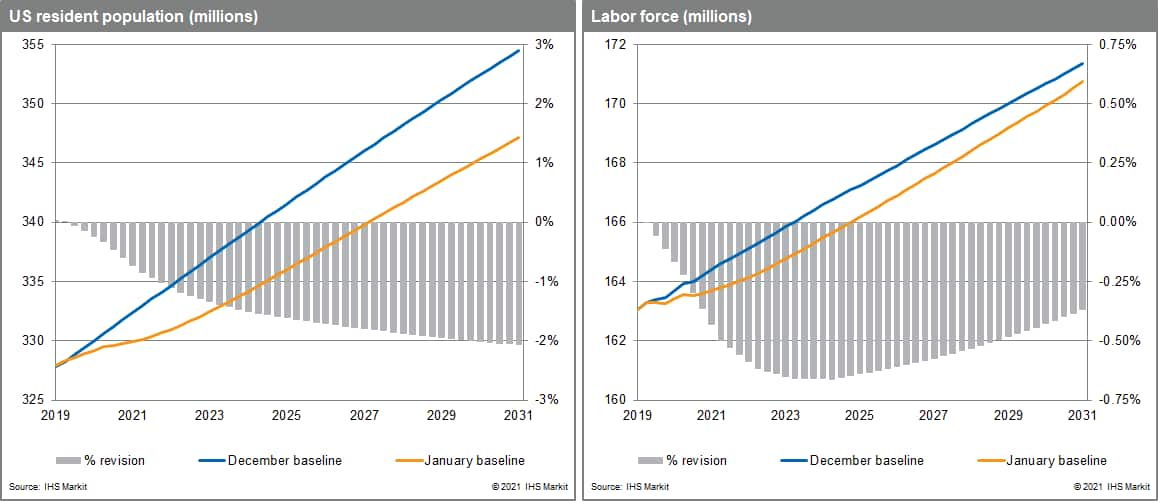

Our population experts—using proprietary models—have determined that, because of the adverse developments mentioned above, population projections for 2030 are likely to be roughly 2.0% lower than previous projections. These new projections are incorporated into the January 2021 IHS Markit baseline forecast for the US economy.

The result of these changes will be a near-term downward revision in total population growth and a permanent downward revision in the level of population. Each of the underlying changes will affect segments of the population differently—the changes in birth rate projections will affect the young population; the excess mortality projections will affect the middle-aged and elderly; and the immigration assumptions will be distributed more evenly across ages.

Demographic impacts

The changes in assumptions about death rates, fertility, and immigration in the new IHS Markit baseline population projections have the following demographic impacts.

Population

The level of US resident population by 2030 is projected to be roughly 2% lower than the prior estimate. With a lower projected fertility rate, the biggest impact (nearly 8% by 2030) will be on the 0-15 age cohort. The impact of the lower population projections for the young population will be reflected in the projections for the older cohorts beyond 2030.

Households

Household formation is projected to be 0.5% lower in the new baseline in 2021 compared with the old. It is then expected to rise to the level of the old baseline by 2025—to a rate of about 1.2 million annually.

The dependency ratio (children as a percent of the total population) is projected to fall faster in the new baseline (to below 18) by 2030, compared with the old baseline (to just under 19).

Working age population and labor force

The working age population is projected to rise to around 285 million by the end of the decade—roughly 0.7% lower than the old baseline.

The labor force participation rate is projected to continue falling in the next decade, mostly because of the aging of the baby boomers.

In the new baseline, the labor force rises gradually to around 168 million by 2030—roughly 2 million below the old baseline.

Macroeconomic impacts

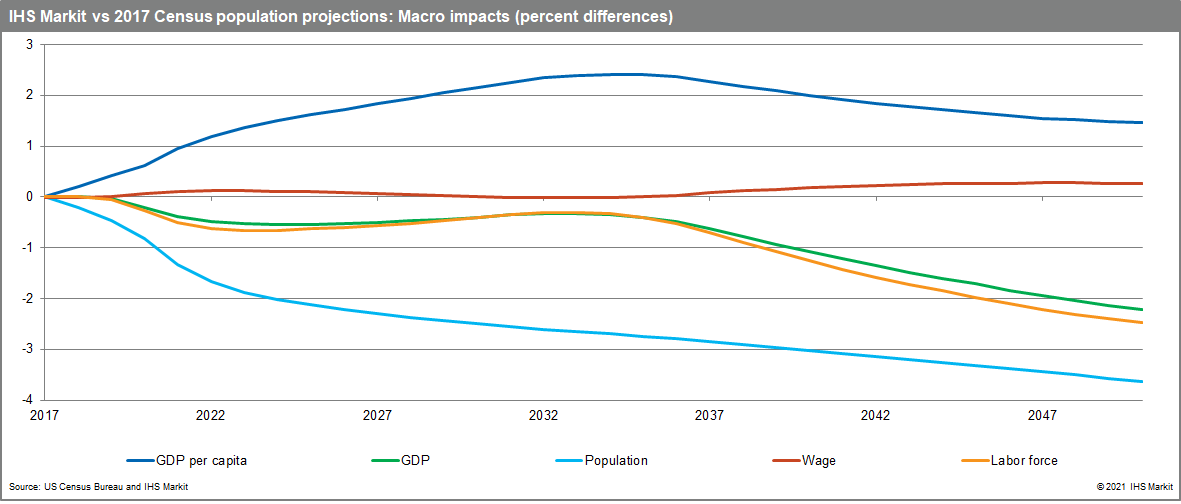

The January IHS Markit baseline forecast incorporates the demographic changes detailed above, as well as new data and changes in policy assumptions. Thus, a macroeconomic comparison of the December and January baselines would not give an accurate estimate of the demographic impacts alone. To provide such a "clean" estimate would require running the old (Census 2017) and new (IHS Markit) demographic assumptions through a small Solow-type growth model. The results can be seen in the accompanying chart.

An interesting result of this model run is that while GDP is down, GDP per capita is up. The main reason is that the decline in population under the age of 16 lowers the denominator of the GDP-to-population ratio. This upward pressure on per capita GDP is accentuated slightly by the standard results in a Solow-type growth model—that lower growth in the labor force slightly raises the productivity of labor (e.g., the real wage) by making labor scarcer relative to capital. The upward revision in the per capita GDP with the introduction of the new population assumptions is a feature of the IHS Markit January forecast.

Note that by 2030, GDP is down 0.40%. This accords closely with results from the larger IHS Markit macroeconomic model.