BLOG — Aug 18, 2021

Daily Global Market Summary - 18 August 2021

By Ana Moreno and Chris Fenske

Major APAC and European equity markets closed mixed, while all major US indices closed lower. US government bonds closed mixed with the curve flatter on the day, while most benchmark European bonds closed higher. IG subindices closed flat across European iTraxx and CDX-NA, while high yield indices were slightly wider on the day. Natural gas closed higher, the US dollar was flat, and oil, gold, silver, and copper closed lower.

Please note that we are now including a link to the profiles of contributing authors who are available for one-on-one discussions through our newly launched Experts by IHS Markit platform.

Americas

- All major US equity indices closed lower; Russell 2000 -0.8%, Nasdaq -0.9%, S&P 500 -1.1%, and DJIA -1.1%.

- 10yr US govt bonds closed flat/1.26% yield and 30yr bonds -2bps/1.90% yield.

- Data from Google Trends indicates that the relative number of Google searches (0-100 scale) in the US for the term 'delta variant' in 2021 (YTD as of Aug 15) began to increase noticeably in June and negatively correlated with the cumulative change in 10yr US Treasury bond yields since June 1.

- CDX-NAIG closed flat/30bps and CDX-NAHY +2bps/295bps.

- DXY US dollar index closed flat/93.14.

- Gold closed -0.2%/$1,784 per troy oz, silver -1.0%/$23.42 per troy oz, and copper -2.0%/$4.12 per pound.

- Crude oil closed -1.7%/$65.21 per barrel and natural gas closed +0.4%/$3.85 per mmbtu.

- Tight gas market fundamentals in the US continue to point to strong fall and winter natural gas prices. As a consequence of capital discipline and supply inelasticity in the face of strong and resilient demand fueled by the twin engines of limited domestic coal switching and booming global LNG markets, the price impact of storage deficits is being amplified on the upside, both in terms of price at a given inventory level and price responsiveness to changes in inventories. For the first time in many years, US gas markets are displaying a lack of confidence that the US shale supply system can balance itself without gas prices materially above $3/MMBtu, leading to the ongoing process of price discovery. This new relationship indicates that the possibility of winter price spikes is higher than in recent years, and that even absent a spike-worthy winter weather event, volatility could be higher. (IHS Markit Energy Advisory's Roger Diwan and North America Natural Gas' Matthew Palmer)

- The minutes of the meeting of the Federal Open Market Committee (FOMC) held on 27 and 28 July were published this afternoon (18 August). At that meeting, the Committee maintained the stance of monetary policy, with unanimous support among voting members. The target for the federal funds rate was kept at a range of 0.00-0.25%, large‑scale asset purchases were continued at their current rate, and the Committee repeated forward guidance for both interest‑rate and balance‑sheet policies. FOMC participants heard staff presentations on options for reducing the pace of asset purchases (the taper) and held an in‑depth discussion about tapering but made no decisions. Most FOMC participants are prepared to start reducing asset purchases this year if economic conditions, especially in labor markets, evolve as they expect. However, several other participants prefer a more patient approach to tapering asset purchases. In response to the revelation in the minutes that "most" participants prefer to start tapering asset purchases this year, we have moved up our assumption for the start of the taper from January 2022 to this November. The impact on our forecasts for bond yields is minor because a slightly earlier start to the taper would have a relatively small impact on the trajectory for the Fed's securities portfolio. (IHS Markit Economists Ken Matheny.

- US single-family permits, arguably the most important number in the monthly new residential construction report, dropped 1.7% in July (plus or minus 0.8%; statistically significant) to a 1.048 million rate. This category fell for the fourth straight month; it stands 4% above its February 2020 pre-pandemic reading, but 17% below a January 2021 peak. (IHS Markit Economist Patrick Newport)

- Soaring home prices have shifted demand from the single-family to the multifamily market. Multi permits soared to a 587,000-unit annual rate, the third-highest monthly reading in 30 years. Builders have taken out 321,000 permits this year through July, the highest year-to-date total since 1986.

- Total permits, which increased 2.6% in July (plus or minus 0.9%; statistically significant), were down 13.0% from a January peak, but still up 11.0% from February 2020, the month before the pandemic struck.

- Housing starts fell 7.0% (plus or minus 8.9%, not statistically significant) in July to a 1.534 million annual rate; single-family starts dropped 4.5% (plus or minus 9.9%, not statistically significant) to a 1.111 million rate; multifamily starts plunged 13.1% to a 423,000 rate.

- The price deflator for new residential structures increased at a 14.6% annual rate in the second quarter, the highest reading since 1973; this followed a 12.6% first-quarter reading. Higher construction costs have played a key role in slowing a housing market that at the start of this year was on fire.

- Housing starts likely peaked in the fourth quarter. We expect them to gradually dip over several quarters before stabilizing in about two to three years at a level set by increases in the number of households.

- More than two dozen shrimp products sold throughout the US by retailers including Target and Whole Foods are now being recalled, due to ongoing concerns about an outbreak of Salmonella Weltevreden linked to frozen cooked shrimp manufactured by Avanti Frozen Foods of India. In the latest development of the unusual Salmonella outbreak, Avanti Frozen Foods announced August 13 it is expanding an existing June 25 recall to include certain consignments of various sizes of frozen cooked, peeled and deveined shrimp sold in various unit sizes. The recalled products were distributed nationwide from November 2020 to May 2021 and are being recalled due to concerns over potential Salmonella contamination, the company said. The Avanti shrimp was sold under various brand names, including Nature's Promise, Meijer, Food Lion, Ahold, Censea, Seacove, Hannaford and more. (IHS Markit Food and Agricultural Policy's Margarita Raycheva)

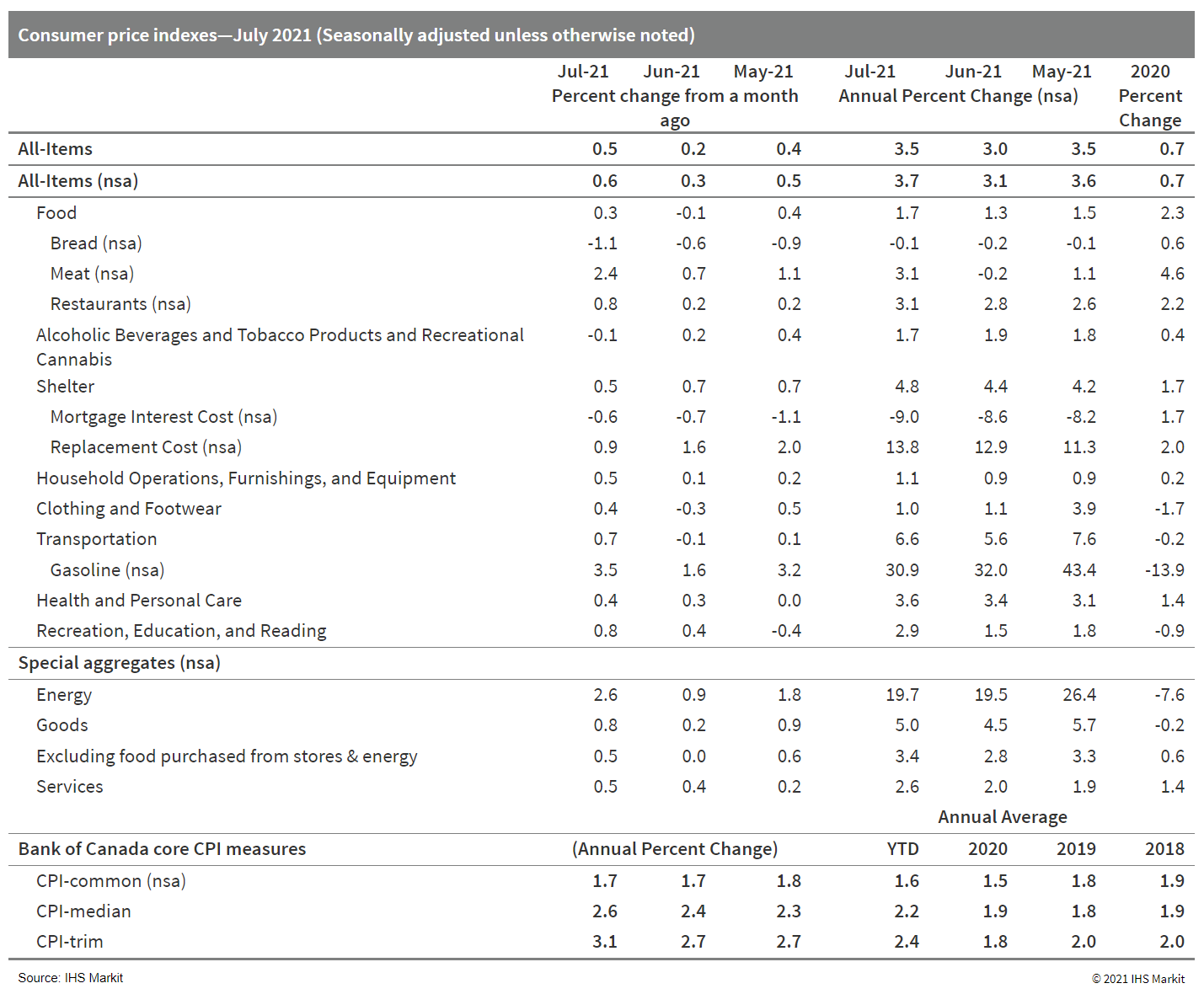

- Canada's consumer prices inflation jumped 0.5% month on month (m/m) on a seasonally adjusted basis (SA) and gained 0.6% m/m on a non-seasonally-adjusted basis (NSA). (IHS Markit Economist Chul-Woo Hong)

- The annual inflation rates elevated to 3.5% year on year (y/y) SA and 3.7% y/y NSA, the strongest pace since March 2003.

- The average core inflation rate was up 0.2 percentage point to 2.5% y/y as the consumer price index (CPI)-trim and CPI-median inflation rates accelerated to 3.1% y/y and 2.6% y/y, respectively.

- Goods and services price inflation quickened to 5.0% y/y and 2.6%, respectively.

- The stronger-than-expected inflation rate in July is still in line with the Bank of Canada's forecast in July's Monetary Policy Report.

Europe/Middle East/Africa

- Major European equity indices closed mixed; Spain +1.2%, Italy +0.5%, Germany +0.3%, UK -0.2%, and France -0.7%.

- 10yr European govt bonds closed higher except for UK flat; Italy -2bps and Germany/France/Spain -1bp.

- iTraxx-Europe closed flat/48bps and iTraxx-Xover -1bp/235bps.

- Brent crude closed -1.2%/$68.23 per barrel.

- The number of payrolled UK employees showed another strong monthly increase, up by 182,000 month on month (m/m) to 28.9 million in July. However, it remains 201,000 below pre-COVID-19 virus pandemic levels. (IHS Markit Economist Raj Badiani)

- Three of the sectors benefiting the most from the end of COVID-19 restrictions reported a rise in payrolled employees between June and July, namely accommodation and food service activities by 32,000 m/m, arts and entertainment by 13,000 m/m, and wholesale and retail by 7,000 m/m.

- The Office for National Statistics (ONS) reported that total UK employment (all aged 16 plus) increased by 95,000 quarter on quarter (q/q), or 0.3% q/q, to 32.3 million in the three months to June, compared with the three months to March.

- In annual terms, the number of employed people in the three months to June was 329,000, or 1.0%, lower compared with a year earlier.

- The number of unemployed people based on the Labour Force Survey (LFS) or the International Labour Organization (ILO) measure decreased by 53,000 q/q in the three months to June, standing at 1.6 million.

- The unemployment rate fell for the second straight quarter when falling to 4.7% in the three months to June. The drop in unemployment was because of rising employment, which offset the impact of a lower economic inactivity rate of 21.1%.

- The pace of job losses continued to slow. The number of redundancies decreased by 52,000 to 99,000 in April-June, compared with the three months to March. This represents a redundancy rate of 3.6 per 1,000, down from 12.9 in October-December 2020

- Furthermore, the number of vacancies continued to climb, averaging a record high of 953,000 over the three months to July, up by 290,000 compared with the three months to April and 168,000 above its pre-pandemic levels.

- The sectors reporting the largest rises in vacancies were accommodation and food service activities and human health and social work activities, up by 73,000 and 57,000, respectively.

- Average annual weekly earnings (total pay including bonuses) growth stood at 8.8% year on year (y/y) in the three months to June. Regular pay (which excludes bonus payments) growth rose for the 11th successive time and at a quicker pace, standing at 7.2% y/y in the three months to June.

- The Office for National Statistics (ONS) has reported that the United Kingdom's 12-month rate of consumer price index (CPI) inflation dropped surprisingly to 2.0% in July from 2.5% in the previous month. (IHS Markit Economist Raj Badiani)

- The rate was equal to the Bank of England's (BoE)'s 2% target for inflation.

- During 2020, inflation averaged 0.9%.

- Energy-related prices rose aggressively on an annual basis, with transport fuel and lubricant prices growing by 17.7 year on year (y/y), the fourth successive double-digit increase. This was in line with global crude oil prices rising by 73.7% y/y to average USD75.1 per barrel (pb) in July, the sixth successive gain since January 2020.

- Clothing and footwear prices decreased by 2.0% month on month (m/m) in July, lowering the annual rate of change to 1.7% from 3.0% in June. This was due to more generous summer sales in July compared with a year ago when clothing and footwear prices fell by 0.7% m/m.

- The ONS reported a notable rise in second-hand car prices due to rising demand because the shortage of semiconductor chips has disrupted production of new vehicles.

- All-services price inflation fell to 1.6% in July from 2.1% in June; for goods, it stood at 2.5%, down from 2.8% in June.

- Core inflation, excluding energy, food, alcoholic beverages, and tobacco prices, retreated to 1.8% in July from 2.3% in June.

- Mini has revealed a new concept to highlight the use of more sustainable materials and manufacturing methods. Working in conjunction with fashion designer Paul Smith, a Mini Electric which has been stripped back and every aspect has been reviewed, to create the Strip concept. Exterior changes include the body being left unpainted with only a transparent paint film applied to prevent corrosion. In addition, the rubbing strips and arches have been 3D printed from recycled plastics, as well as the front and rear apron inserts, while the grille, aerodynamic wheel covers, and panoramic roof have been manufactured from recycled Perspex. The interior has also been taken back to basics, with all the trim omitted with the exception of the dashboard, topper pad and parcel shelf, while the central dashboard display has been removed and would instead be replaced by the driver's smartphone. The only controls are said to be toggle switches for the power windows and the start-stop function. The seats are upholstered in a knitted mono-material that is fully recyclable, and the floor mats are manufactured from recycled rubber. The interior uses cork for certain remaining trim elements, which helps acoustics, and a mesh covering is used to cover the airbag pad on the steering wheel and the door panels. (IHS Markit AutoIntelligence's Ian Fletcher)

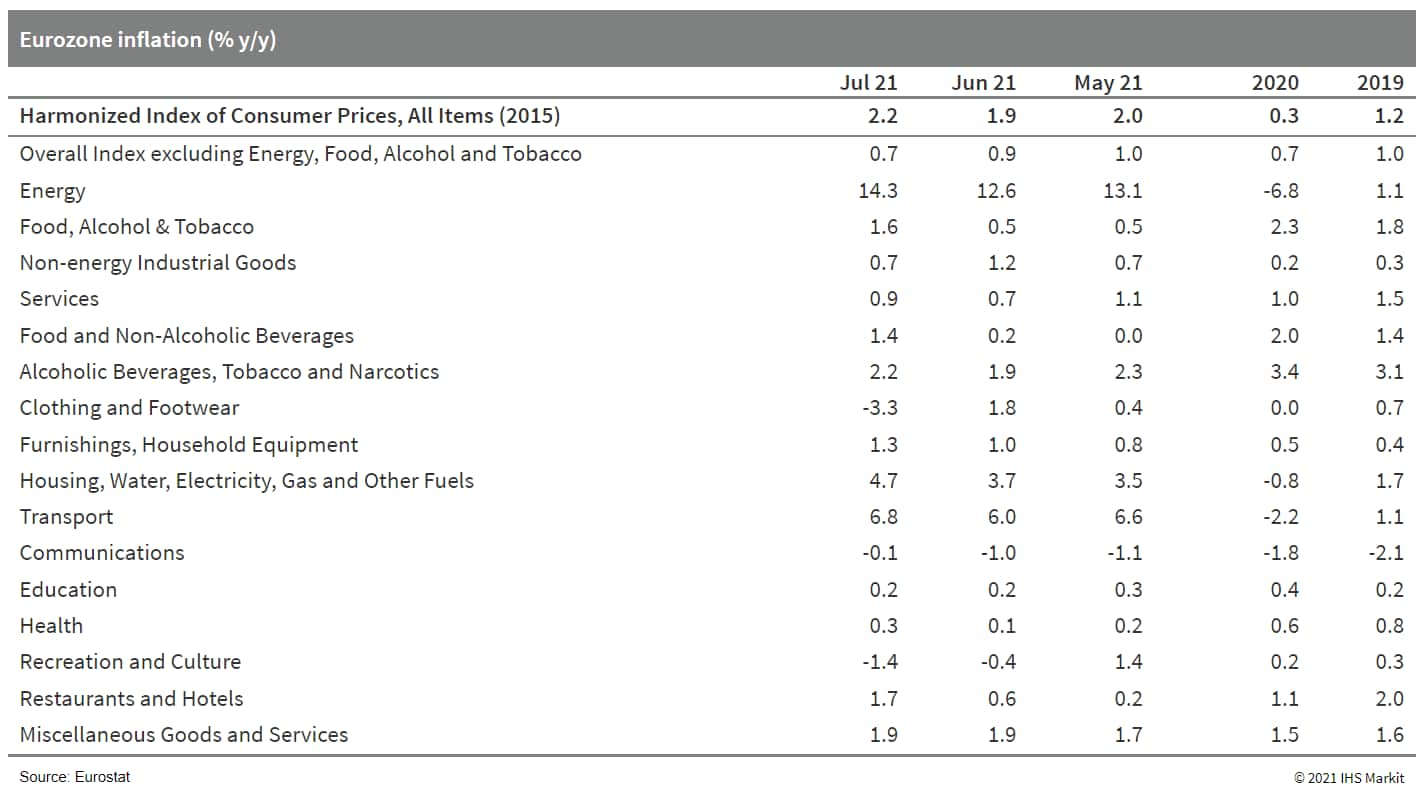

- July's rise in eurozone HICP inflation from 1.9% to 2.2% was confirmed by Eurostat's final estimate, above the initial market consensus expectation (of 2.0%). (IHS Markit Economist Ken Wattret)

- This is the highest rate since October 2018, with energy primarily responsible for the acceleration.

- The year-on-year (y/y) rate of change in energy inflation rose to a new high of 14.3% in July, slightly above the "flash" estimate. In contrast to prior months, however, the acceleration was not due to base effects but rather, a strong month-on-month (m/m) rise (of 2.0%, due to higher crude oil prices).

- The final data also confirmed July's unexpectedly large decline in the core HICP inflation rate excluding food, energy, alcohol and tobacco prices, from 0.9% down to 0.7%.

- Spain's wine inventory fell to 39.4 million hectoliters in June, down by 3.5 million hectoliters from May, according to the latest wine market report from Spain's agriculture ministry. (IHS Markit Food and Agricultural Commodities' Vladimir Pekic)

- The country's total June inventory consisted of 21.4 million hl of red/rose in bulk, 11.4 million hl of white in bulk, 3.2 million hl of bottled red/rose and 3.4 million hl of bottled white wine. The overall wine inventory is still 2 million hl higher than in June 2020.

- Although the June inventory is larger than last year's, the market seems to be balancing out. The new wine grape harvest in the Valencian Community is approaching and according to the estimates of the farmers' association LA UNIÓ de Llauradors it could be between 5-10% lower than last year. The group said it expects the Spanish crop to suffer an even larger decline.

- Asaja, the largest agricultural professional organization in Spain, recently predicted that between 39 -40 million hectoliters of wine will be produced this upcoming season (2021-22), down 15% from 46.49 million hectoliters in the previous season and about 10% less than the average of the last three seasons.

- The expected drop in production will occur in the largest grape-growing areas, such as Castilla-La Mancha, where the drop in wine production is expected to reach 15% y/y, and in Extremadura that is predicted to produce 20% less wine than in the previous season. This decrease in production is being attributed to the damages caused by the Filomena snowstorm in January, which caused significant damage in the main wine-growing areas.

- The Bank of Uganda (BoU) during its monetary policy committee (MPC) meeting on 12 April maintained its benchmark policy rate at 6.5%; the central bank rate (CBR) was lowered from 7.0% to 6.5% in June. (IHS Markit Economist Alisa Strobel)

- In August, the central bank's MPC announced that it will maintain the CBR at 6.5%, raising concerns that a second wave of the coronavirus disease 2019 (COVID-19) virus pandemic is likely to have a severe negative impact on the economy during the third quarter of 2021.

- The MPC has also decided to maintain the band on the CBR at plus or minus 2 percentage points, while the margin on the rediscount rate and bank rate was left unchanged at 3 and 4 percentage points on the CBR, respectively. The rediscount rate and the bank rate were maintained at 9.5% and 10.5, respectively, at the MPC meeting.

- The BoU has highlighted that uncertainty regarding its inflation projections remains. Although risks are balanced, the adverse weather and high global commodity prices of oil, for example, could continue fueling headline inflation upwards through higher food and transportation costs. However, domestic demand could decrease, lowering price pressures in the wake of a second wave of the COVID-19 virus pandemic and its related containment measures.

Asia-Pacific

- Major APAC equity markets closed mixed; Mainland China +1.1%, Japan +0.6%, South Korea +0.5%, Hong Kong +0.5%, Australia -0.1%, and India -0.3%.

- Mainland China's year-on-year (y/y) real industrial value-added growth fell by 1.9 percentage points to 6.4% in July, marking the third consecutive month of decline since May. Meanwhile, on a two-year (2020-21) average basis, the growth rate fell to 5.6% from 5.6% in the previous month. The month-on-month growth rate also fell by 0.3 percentage point to 0.3% expansion after a short-lived pickup in June. (IHS Markit Economist Yating Xu)

- Contraction in upstream sectors due to production curbs implemented to help achieve decarbonization targets, in addition to the persisting chip shortage, led to the moderation in industrial production. Meanwhile, the resurgence of COVID-19 cases and extreme floods this summer added to the disruptions in overseas and domestic demand. By sector, ferrous metals smelting sector growth deteriorated from a 4.1% y/y expansion to a 2.6% y/y contraction, while growth of the non-ferrous metals smelting and non-metal minerals sector moderated. Downstream sectors' performance continued to diverge, with the high-tech manufacturing sector maintaining double-digit growth while the automobile manufacturing sector contracted further. The equipment manufacturing sector's growth fell with the slowdown in infrastructure investment growth.

- The service production index, on a two-year (2020-21) average basis, grew by 5.6% compared with 2019 levels, down 0.4 percentage point from the reading a month ago but higher than the percentage point lower than the May 2019 growth rate.

- Year-on-year FAI growth declined by 2.3 percentage points to 10.3% through July largely as a result of the higher-base effect. On a 2020-21 average basis, FAI growth fell to 4.3% from 4.4% in the previous month. Month-on-month growth slowed from 0.26% in June to 0.18% in July. IHS Markit estimates that decumulative FAI growth deteriorated from 6% y/y expansion to 0.4% y/y contraction.

- By sector, estimated decumulative infrastructure investment fell by 10.1% y/y in July compared with a 0.3% y/y fall in the previous month; estimated decumulative real estate investment growth fell from 6% y/y in June to 1.2% y/y in July owing to the government's deepening de-risking campaign. Decumulative combined real estate and infrastructure investment growth deteriorated from a 2.3% y/y expansion in June to 5.2% y/y contraction in July. Manufacturing investment continued to improve with sustained robust growth in investment in high-tech manufacturing and high-tech services, such as medical instruments, aerospace equipment, and e-commerce.

- The floor space of commercial housing sales dropped by 8.7% in July from a 7.5% y/y expansion in June as housing market controls were tightened in cities with "hot" housing markets. Meanwhile, developers' financing growth continued to slow to 9.2% on a two-year (2020-21) average basis as bank loans declined, while mortgages and purchasers' deposits expanded at slower rates.

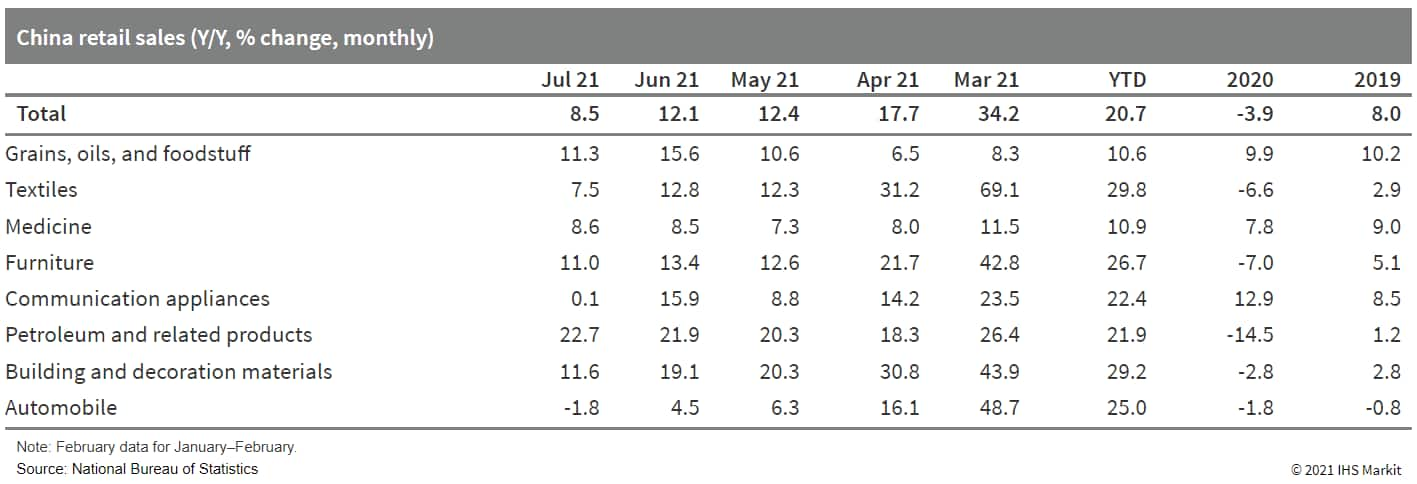

- Year-on-year nominal retail sales fell by 3.6 percentage points from June to 8.5% in July, despite the consumption drive in summer vocation. On a two-year (2020-21) average basis, nominal retail sales growth declined by 0.9 percentage point to 3.6%. Month-on-month growth declined by 0.13%. Real retail sales growth decelerated by 3.4 percentage points to 6.4% y/y.

- Baidu has unveiled its first fully autonomous robocar Apollo during its annual flagship technology conference Baidu World 2021, reports CNBC. The robocar is equipped with Level 5 autonomous system, representing fully autonomous capability, with no steering wheel or pedals. The company also launched the second-generation version of its artificial intelligence (AI) chip, Kunlun II, which has entered mass production. It is designed to support autonomous vehicle (AV) operations by assisting devices in processing huge amounts of data and boosting computing power. It has also announced the rebranding of its driverless taxi app to "Luobo Kuaipao" as it plans to roll out robotaxis on a massive scale. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Japan's private machinery orders (excluding volatiles), a leading indicator for capital expenditure (capex), fell by 1.5% month on month (m/m) in June following three consecutive months of increases. However, orders from manufacturing and non-manufacturing (excluding volatiles) continued to rise by 3.6% m/m and 3.8% m/m, respectively, as the sum of seasonally adjusted individual groupings did not match total private machinery orders (excluding volatiles). (IHS Markit Economist Harumi Taguchi)

- Orders from the public sector fell by 2.8% m/m following a 3.1% m/m increase in the previous month. Orders from overseas also declined by 10.0% m/m following sharp increases in April and May.

- The third consecutive rise in orders from manufacturing largely reflected rebounds in orders from non-ferrous metals, general-purpose and production machinery, and information and communication electronics equipment, offsetting declines in electrical machinery, shipbuilding, and some other groupings. The continued increase in orders from non-manufacturing was thanks largely to rises in orders from wholesale and retail trade and construction.

- Japan's trade balance recorded a surplus of JPY441 billion (USD4 billion) on a non-seasonally adjusted basis in July. The seasonally adjusted balance also recorded a surplus of JPY53 billion following a deficit of JPY63 billion in the previous month. Exports continued to grow, but softened to a 37.0% year-on-year (y/y) increase following a 48.6% y/y rise in the previous month. Imports also softened to 28.5% y/y in July after a 32.7% y/y rise in June. (IHS Markit Economist Harumi Taguchi)

- The softer increase in exports was due largely to easing low base effects because of a plunge a year earlier in line with the global lockdowns. Even so, export growth to all regions remained solid. Major contributors to the increase were exports of autos, auto parts, steel and iron, and semiconductors. However, auto export volume remained below the pre-pandemic level.

- The rise in imports largely reflected higher prices for energy and other commodities, as import volume growth softened to 2.1% y/y from 8.2% y/y in the previous month. While mineral fuels were the major driver of imports, accounting for 11.1 percentage points of total imports, other major contributors to the increase were iron ore and concentrate, non-ferrous metals, semiconductors, and medical products (presumably vaccines from the European Union and the US).

- In the bid to improve its financial health and develop eco-friendly shipbuilding technologies, SHI will raise USD1.1 billion (KRW1.23 trillion) through the sale of new shares. 250 million common shares at KRW4,950 per share will be issued by SHI but offering price to be finalized by end Oct. 20% of the shares will be allocated to the company's employees while the balance to its shareholders. Trading of the new shares in the main stock market will commence on 29 November 2021. SHI has been in the red since the 2015. (IHS Markit Upstream Costs and Technology's Jessica Goh)

- BP said a study into the feasibility of an export-scale green hydrogen and ammonia production plant in Western Australia found that production using renewable energy is technically feasible at scale. Western Australia "is an ideal place to develop large-scale renewable energy assets that can in turn produce green hydrogen and/or green ammonia for domestic and export markets," the company said in early August. Green hydrogen production involves electrolysis using power from renewable resources. Green ammonia uses this green hydrogen and atmospheric nitrogen as feedstocks. Both renewables-sourced gases are seen as key decarbonization tools, especially in hard-to-transition sectors such as transportation and industries including steel production. The study findings support BP's view that Western Australia's potential solar and wind resources, existing infrastructure, and proximity to large, long-term markets make it "particularly promising," according to Frédéric Baudry, APAC senior vice president for fuels and low carbon solutions at BP. BP said it will continue to work with key stakeholders to develop plans for integrated green hydrogen projects in Western Australia, defining technical and infrastructure solutions, customer demand, and the business models. A potential investment figure and project schedule were not disclosed. BP commenced a study in May 2020 of the hydrogen supply chain and domestic and export markets at two differing scales. One was for a demonstration/pilot-scale plant for up to 4,000 metric tons (mt)/year of green hydrogen to produce up to 20,000 mt/year of green ammonia, while the other was for a 200,000-mt/year renewable hydrogen plant producing up to 1 million mt/year of green ammonia. (IHS Markit Net-Zero Business Daily's Keiron Greenhalgh)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.